- Economic recovery is underway in India following damaging waves of COVID-19. Real GDP growth is expected to stabilize at around 7% y/y in 2022–2023, following an estimated 9% gain this year.

- Consumer and business sentiment is improving, supporting household spending and investment prospects, yet the evolving COVID-19 situation will remain the main factor impacting domestic demand momentum.

- Persistently high core inflation complicates the Reserve Bank of India’s monetary policymaking at the time of nascent economic recovery. Inflationary pressures and financial stability considerations are expected to prompt the central bank to commence a cautious monetary normalization phase in the first half of 2022.

ECONOMIC GROWTH OUTLOOK

India’s economy is recovering on the back of an improved COVID-19 situation and a resultant easing of movement restrictions. In Q3-2021, the nation’s real GDP expanded by 8.4% y/y (chart 1), supported by solid gains in domestic demand and recovering industrial activity. While output growth will likely weaken in the final quarter of the year as the favourable year-ago base effect fades away, we forecast India’s real GDP gains to average 9.0% in 2021 as a whole. In 2022–2023, economic growth will likely stabilize at around 7% y/y, slightly above the country’s current potential growth estimate of around 6%. Nevertheless, we note that the forecast is subject to significant uncertainties related to COVID-19 developments. The Indian economy’s longer-term outlook is underpinned by favourable demographics and competitive labour costs. Meanwhile, pandemic-related scarring—such as educational disruptions and their impact on human capital as well as muted fixed capital investment—needs to be addressed and requires strong political will for continued reform implementation.

The evolving COVID-19 situation and the speed of India’s vaccination program will be the key factors impacting the outlook for private spending. While consumer confidence has shown early signs of recovery (chart 2), Indian households remain rather cautious, which is reflected in muted spending indicators, such as vehicle sales. Nonetheless, sentiment should strengthen along with advancing vaccination levels, underpinning economic growth momentum into 2022; currently only 32% of the Indian population is fully vaccinated.

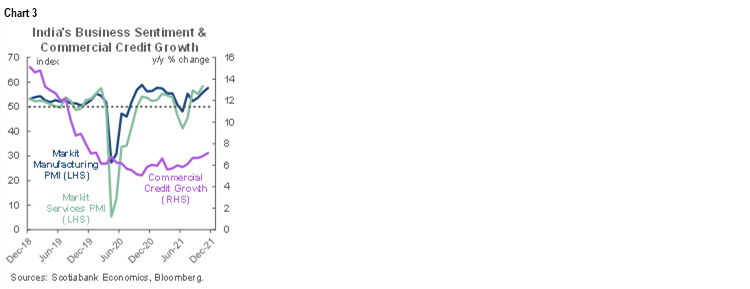

Improving business sentiment across the services and manufacturing sectors (chart 3), an accommodative policy backdrop, as well as the government’s investment incentives and lending schemes will underpin the outlook for private sector business investment. Nevertheless, the pickup is expected to be gradual, in line with a cautious acceleration in commercial sector credit growth (chart 3). Reflecting implemented reforms in recent years, India has continued to attract foreign direct investment throughout the pandemic, and we expect the trend to continue over the foreseeable future.

Government spending remains growth-supportive even though fiscal space has narrowed significantly during the pandemic. Public outlays are targeted at healthcare, infrastructure, and education in order to improve India’s long-term economic growth potential. According to the IMF, India’s general government deficit reached 12.8% of GDP in Fiscal Year 2020–2021 (April–March), doubling from the pre-pandemic level. While the government is prioritizing the economy’s recovery, it is simultaneously trying to show commitment to fiscal prudence over the medium-term in order to support investor confidence, in line with a recommendation by the IMF.

The external sector plays a smaller role in the domestically-driven Indian economy compared with the country’s export-oriented regional peers. Regardless, Indian exporters are benefiting from strong global demand, particularly in the US and the European Union that together purchase over 30% of India’s shipments abroad. At the same time, rebounding domestic demand and elevated oil prices are boosting India’s imports. Accordingly, we assess that the external sector will remain a drag on real GDP growth over the coming quarters.

INFLATION, MONETARY POLICY, AND INDIAN RUPEE OUTLOOK

India’s headline consumer price inflation dynamics have been volatile over recent months, while core inflation—CPI inflation excluding food and fuel—has remained persistently elevated (chart 4). Recently, weaker food price inflation has brought the headline rate down, with prices rising by 4.5% y/y in October, yet we assess that inflation will accelerate somewhat over the coming quarters. The upward pressures will be partially offset by the government’s recent decision to reduce excise duties on petrol and diesel, bringing temporary relief to consumers. Headline inflation will likely reach 5.2% y/y by the end of 2021, pushed up by increased materials prices, high logistics costs, and rebounding domestic demand. In 2022–23, we expect price gains to remain elevated yet slightly below the upper ceiling of the Reserve Bank of India’s (RBI) inflation target of 2%–6%. However, the forecast is subject to notable uncertainties that reflect food and commodity price movements as well as the Indian rupee outlook in the context of a monetary normalization bias in advanced economies.

The volatile and uncertain inflation dynamics are complicating the RBI’s monetary policy conduct. The central bank maintains its “accommodative” policy stance and has pointed out that it would be continued as long as necessary to revive and sustain growth on a durable basis, while keeping inflation within the target. Indeed, the Indian economy needs supportive monetary conditions to underpin the nascent recovery, though persistent inflationary pressures are likely to keep the RBI’s policymakers cautious. Accordingly, we expect the RBI to maintain the benchmark repurchase rate unchanged at 4.0% in the near-term; the policy rate was lowered by 115 basis points at the early stages of the pandemic. As many advanced and emerging market economies continue normalizing monetary policy over the coming months, Indian monetary authorities will likely start paying additional attention to financial market and exchange rate stability. Accordingly, we expect the RBI to commence a cautious monetary normalization phase by mid-2022, taking the benchmark repurchase rate from the current level of 4.0% to 4.75% by the end of 2022.

The Indian rupee (INR) has faced a gradual weakening bias against the US dollar (USD) in recent months (chart 5). We expect the value of the rupee to continue to reflect changes in global risk aversion amidst the evolving COVID-19 situation together with volatile appetite toward emerging market assets, shifting expectations regarding the US monetary policy normalization, as well as the prospects of India’s current account balance swinging back into deficit amidst elevated oil prices and recuperating domestic demand. Simultaneously, high initial public offerings activity in India, a recovering economy, and manageable inflation outlook point to higher domestic real returns, supporting rupee-denominated assets. We expect USDINR to close the year at 74 before appreciating modestly to 72 by the end of 2022.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.