- The “Common Prosperity” -ideology is set to drive Chinese authorities’ policy agenda, likely leading to continued government intervention into private sector affairs.

- China’s real estate sector’s debt crisis clouds the economic outlook; targeted approach to debt restructuring is expected.

- China’s economic growth is slowing on the back of several simultaneous factors; real GDP gains are expected to stabilize at around 5½% y/y in 2022–23.

- China’s monetary policy is a balancing act between supporting growth and addressing financial imbalances.

- Soft domestic demand will keep demand-driven inflationary pressures at bay; the Chinese renminbi is expected to remain relatively stable through 2023.

PUBLIC POLICY CONSIDERATIONS

An ideological shift is taking place in China. The Chinese government is emphasizing “common prosperity” as one of its key policy objectives, pointing out that private sector capital should work for the people instead of being driven by profits. President Xi Jinping is working to mold China into a “modern socialist power”, where the private sector is asked to support the Communist Party’s goals. Given that China is a highly unequal society with large income disparities, we assess that the policy shift reflects the government’s priority of maintaining social stability. The “common prosperity” ideology seems to be behind the government’s increased intervention into private sector affairs, in such areas as technology, education, gaming, entertainment, e-commerce, property and many others. We believe that the government’s interventionist approach will remain in place in the foreseeable future.

China’s real estate sector’s debt burden has raised significant investor concerns in recent weeks, as Evergrande—one of the country’s largest developers—has failed to pay interest due on certain offshore bonds and will face sizable debt repayments over the coming quarters. Real estate is one of the key pillars of the Chinese economy; therefore, developers’ financial issues need to be monitored closely in case the government’s recent clampdown on the real estate sector’s leverage levels creates broader financial stress among the country’s developers.

We assess that the government will likely orchestrate a managed restructuring of Evergrande, which would provide a guideline for any potential future challenges faced by the country’s developers. Given the “common prosperity” goal and social stability considerations, the Chinese government will likely try to support ordinary people over institutional investors. Local governments, for example, could step in to ensure certain development projects are continued in order to protect those who have made down-payments on homes. This would simultaneously underpin the construction sector and its suppliers, as well as overall employment in related industries. Moreover, we assess that there could be intervention to support—e.g., via a separate prioritized debt-repayment plan—the people who have invested in shadow banking instruments issued by the troubled developer, as their risks may not be properly understood by retail investors who now face the possibility of losing their savings. Internationally, we assess that any global spillovers from the real estate debt crisis are set to remain limited and felt mostly through changes in international investors’ risk sentiment. This reflects the fact that the Chinese bond market is not deeply integrated into the global financial market due to China’s capital controls; at end-2020, foreign investors accounted for only around 4% of the onshore bond market’s investor base.

ECONOMIC GROWTH OUTLOOK

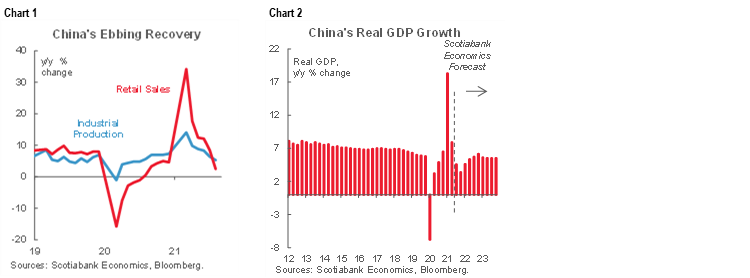

Recent high-frequency data show that the slowdown of the Chinese economy has been more pronounced than what was envisioned earlier this year (chart 1). Indeed, there are several factors putting downward pressure on the economy: 1) occasional surges of COVID-19 cases and resultant movement restrictions; 2) concerns regarding the real estate sector’s debt levels; 3) supply-chain bottlenecks; 4) regulatory tightening and the government’s intervention in the private sector’s affairs; and 5) power shortages that reflect the government’s efforts to reduce emissions as well as high prices and shortages of coal. Following solid year-over-year real GDP growth of 18.3% and 7.9% in the first and second quarters of 2021, respectively, China’s output gains are poised to weaken notably over the second half of the year, taking the country’s average economic expansion to around 8½% this year (chart 2). Nevertheless, the government’s 2021 economic growth target of “above 6%” will be easily surpassed. In 2022–23, we foresee output growth normalizing, with real GDP expanding by around 5½% y/y, in line with China’s estimated potential growth of around 5–6% y/y.

Recent weakness in Chinese household spending reflects muted consumer confidence (chart 3) and movement restrictions imposed because of a surge in Delta variant cases. While we expect the softness to be temporary—indeed, the services sector has started to show signs of revival—it highlights the fact that China’s economic recovery remains uneven and fragile. The real estate sector’s debt crisis casts a shadow on the consumer as around 70% of household wealth is linked to real estate; fire sales and declining house prices would erode consumer confidence and household balance sheets, limiting spending prospects.

Fixed investment remains a key growth driver in China, but tighter lending standards have resulted in a weaker growth in capital investment (chart 4). The troubled real estate sector and related activities account for about a quarter of Chinese GDP; accordingly, weaker housing demand and less funding available for real estate development is expected to adversely impact fixed asset investment activity. Some of the softness will be offset by higher public infrastructure investment—in such areas as technology, urban transportation, utilities facilities, and rural development—as Chinese authorities are speeding up local governments’ issuance of special-purpose bonds. In the first nine months of the year, only 65% of the 2021 issuance quota of CNY 3.65 trillion had been used, compared with 90% of the 2020 quota of CNY 3.75 trillion used by September last year.

China’s external sector has benefitted from rebounding global demand with the nation’s exports during the first nine months of the year being 23% higher (in CNY terms) than over the same period in 2020 (chart 5). While we expect continued solid export gains, some moderation is likely in the near term, as global demand dynamics will normalize from goods to services along with the reopening of economies. Moreover, high freight costs and material prices are hurting exporters while electricity rationing is adversely impacting manufacturing production. As the US remains China’s most important export market—shipments to the US accounted for over 17% of total Chinese exports last year—the US-China trade relationship will play a key role in China’s external sector outlook. Following an intense trade conflict between the two countries over recent years, the US has recently resumed diplomatic dialogue with China. While we do not expect the Biden administration to announce any tariff reductions on Chinese imports in the near future, we consider the return to the negotiation table a positive development. Nonetheless, the bilateral relationship will remain challenging over the foreseeable future on the back of fundamental differences in ideology as well as in political and economic structures.

MONETARY POLICY, INFLATION AND CHINESE YUAN OUTLOOK

The People’s Bank of China (PBoC) will likely continue to monitor the banking system’s liquidity situation closely, alleviating any stress resulting from the real estate sector’s debt crisis. Should weaker lenders face any financial difficulties in the face of potentially rising non-performing real estate loans, we would expect China’s monetary authorities to intervene effectively to limit any banking sector instability. We also note that the Chinese banking system is dominated by state-owned banks, which will underpin confidence in the financial system during times of stress.

Conducting monetary policy in China is a balancing act between supporting the economy and addressing rising financial imbalances, such as weaker quality of debt. Accordingly, we do not expect any significant policy moves over the near term; any central bank action is likely to be targeted and fine-tuned. The PBoC will use its relending programs for underpinning economic growth; in early-September, the central bank announced CNY 300 billion of low-interest rate funding to banks that will be lent to specific areas of the economy, such as micro, small, and medium-sized enterprises that are important employers in the country. Considering the government’s deleveraging efforts, we do not foresee any interest rate cuts in the foreseeable future, with the PBoC’s 1-year and 5-year Loan Prime Rate fixings set to remain at 3.85% and 4.65%, respectively. Nevertheless, as Chinese domestic demand has room to strengthen, we forecast that the PBoC will opt to reduce banks’ reserve requirement ratio (RRR) before the end of the year to provide additional support. The most recent RRR cut of 50 bps took place in July 2021 (chart 6).

We forecast China’s headline inflation to accelerate in the near future from the current low level of 0.7% y/y (chart 7). While inflation is set to remain well below the government’s 3% target for 2021, we expect consumer prices gains to approach 2% y/y by the end of the year on the back of base effects as well as higher electricity and commodity prices. Price pressures further up the distribution chain continue to build, with producer prices climbing by over 10% y/y. Nevertheless, firms’ limited pricing power—due to weak domestic demand—is likely to prevent a significant spillover from the producer side to consumer prices. We forecast headline consumer price inflation to hover at slightly above 2% y/y in 2022–23.

The Chinese yuan (CNY) has remained stable against the US dollar (USD) over the past few months (chart 8) following a solid gain of around 10% between mid-2020 and early 2021 as China was leading the global economic recovery. We expect further stability ahead with USDCNY closing 2021 at 6.40. While the CNY may benefit from improved sentiment related to resumed diplomatic dialogue between the US and China, we expect the currency to avoid notable appreciation in the short term; with the export sector playing a key role in China’s economic recovery, it is not in Chinese regulators’ interest to allow significant CNY gains. USDCNY is expected to close 2022 and 2023 at 6.30 and 6.10, respectively.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.