- The Australian economy has hit a speed bump due to a surge in COVID-19 Delta infections; we expect softness in economic activity to prove temporary, with the economy’s solid growth momentum returning before the end of 2021.

- Lockdown-related weakness in the labour market makes consumers cautious spenders in the near-term. Once restrictions are eased, the labour market and consumer spending are expected to rebound.

- Inflationary pressures have intensified; while some of the pickup is expected to be transitory, Australia’s inflation is forecasted to remain within the central bank’s 2–3% target through 2023.

- Monetary policy will remain accommodative for an extended period, assisting the economic recovery. We expect gradual adjustments to the central bank’s quantitative easing program over the coming months to pave the way for cautious interest rate hikes from Q3 2023 onwards.

ECONOMIC GROWTH OUTLOOK

A surge in COVID-19 Delta infections (chart 1) has clouded Australia’s near-term economic outlook following solid performance in the first half of 2021. Due to a still-low vaccination coverage—only around 40% of the Australian population is fully vaccinated against COVID-19—rising infections have triggered widespread lockdowns. Accordingly, real GDP is expected to contract in quarter-over-quarter terms in the third quarter of 2021. Nevertheless, we do not expect two consecutive quarters of declining output, which would mark a double-dip recession. The Australian economy will likely bounce back as soon as the situation starts normalizing, with the rebound underpinned by a recently accelerated inoculation program that aims to reach 80% vaccination coverage by December. Meanwhile, Australia’s fiscal measures should offset some of the adverse impact on the economy, complemented by highly accommodative monetary policy. Australia’s real GDP is expected to increase by 4½% in 2021, followed by an average gain of 2⅓ y/y in 2022–23.

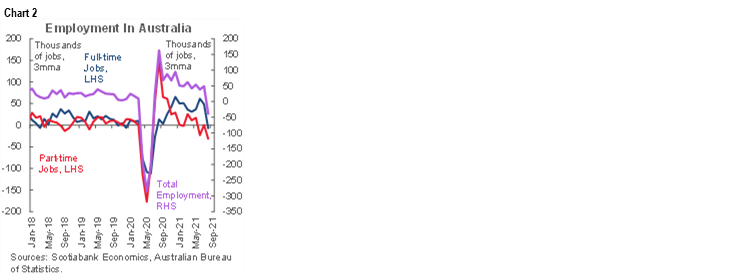

The Delta outbreak and resultant lockdowns are negatively impacting Australian consumer confidence and household spending, particularly on services. In the first half of 2021, a robust labour market and rising house prices had created a supportive backdrop for the consumer. Now, the Delta surge has led to a decrease in employment—both part-time and full-time (chart 2)—making households more cautious spenders in the near-term. Nevertheless, we expect the labour market to recover relatively quickly once movement restrictions are eased, helped by the government’s employment support programs as well as labour shortages in certain sectors that reflect closed international borders. Prior to the Delta wave, the labour market was tightening with many companies facing difficulties in filling vacancies; therefore, we assess that during the current wave firms are more likely to adjust offered hours than overall employment levels, which should help the labour market get back on its feet. Meanwhile, households’ savings are elevated, and their net wealth has continued to increase on the back of rising house and equity prices. Accordingly, we assess that the Australian consumer will confidently spend again once movement restrictions are eased and vaccinations advance.

The near-term outlook for business investment remains somewhat uncertain on the back of softer confidence, yet we expect Australia’s supportive policy environment to underpin a gradual recovery in business outlays over the coming quarters. Meanwhile, Australia’s external sector prospects remain sound, assisted by favourable terms of trade (chart 3) and the global economic recovery. Iron ore shipments to China—Australia’s main export destination—maintain strong growth momentum, but many other (less economically significant) exports face obstacles stemming from the ongoing conflict between Australia and China. We expect further headwinds for the bilateral relationship, particularly as Australia very recently established a security pact with the US and the UK.

INFLATION, MONETARY POLICY AND AUSTRALIAN DOLLAR OUTLOOK

Australia’s headline inflation accelerated to 3.8% y/y in the second quarter (chart 4) on the back of year-ago base effects. While the significant pickup is forecast to be temporary, inflation will likely remain consistent with the Reserve Bank of Australia’s (RBA) 2–3% target through the foreseeable future as the economy’s spare capacity diminishes. We expect headline inflation to close 2021, 2022 and 2023 at 2.7% y/y, 2.3% and 2.5%, respectively.

The trajectory of wages will be an important contributor to the RBA’s monetary policy decisions over the coming quarters. The RBA has said that wage inflation at around 3% y/y would keep inflation consistently within the target over the longer term. Wages increased by 1.7% y/y in mid-2021; we forecast wage inflation to approach the 3% mark in mid-2022, yet Australia’s border restrictions and associated labour shortages create significant uncertainties around the forecast.

Australian monetary conditions will remain supportive of economic growth for an extended period. In September, the RBA tapered its current quantitative easing program for the first time, reducing the purchases of Australian government securities from AUD5 billion a week to AUD4 billion. The central bank also announced that the current level of purchases will be maintained until mid-February on the back of uncertainties related to the Delta wave of COVID-19 infections. We assess that the economy’s expected bounce-back in the fourth quarter will allow the RBA to announce another tapering step in December, with reduced purchases implemented from February 2022 onwards.

The RBA expects that conditions for monetary tightening will not be met before 2024. While we do not foresee runaway inflation in Australia, we believe that the RBA is overly dovish in its expectation of the benchmark interest rate remaining on hold at 0.10% until 2024, well past most other major central banks’ monetary normalization timelines. We expect the Australian economy to prove more resilient than the RBA assumes; therefore, we highlight the risk of a shift in the RBA’s tone over the course of 2022. We expect the first rate hike—of 15 basis points—to be implemented in the third quarter of 2023, with the policy rate closing the year at 0.50%.

The Australian dollar (AUD) has depreciated against the US dollar (USD) in recent months (chart 5), reflecting market participants’ expectation that the US Federal Reserve is set to announce a plan to start tapering its bond purchases soon. Moreover, the AUD has weakened on the back of the COVID-19 surge in Australia and the RBA’s relative dovishness. Nevertheless, as the resilient Australian economy is expected to rebound in the near term, the AUD will likely regain some strength against the USD. We expect AUDUSD to close 2021 at 0.78 and 2022 at 0.75.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.