COVID-19 resurgences risk Australia’s nascent economic recovery.

Domestic demand is set to remain soft while the external sector outlook is clouded by diplomatic tensions with China.

Accommodative monetary policy is expected to remain in place for several years due to weak inflationary pressures.

ECONOMIC GROWTH OUTLOOK

Australia is set to join other advanced economies in recording a deep yet brief recession this year, for the first time in almost 30 years. In the first quarter of 2020, real GDP contracted by 0.3% q/q (+1.4% y/y); we estimate that the second quarter drop was significantly larger on the back of declining domestic demand that follows the curtailment of activity due to the COVID-19 pandemic. Australia’s real GDP is forecasted to contract by 3.6% in 2020 as a whole. Growth will likely rebound to 2.7% in 2021 on the back of the lagged impact of monetary and fiscal stimulus measures, pent-up demand, and base effects. We note that there are substantial uncertainties regarding the forecast, with new waves of infections across the country posing notable downside risks to the outlook.

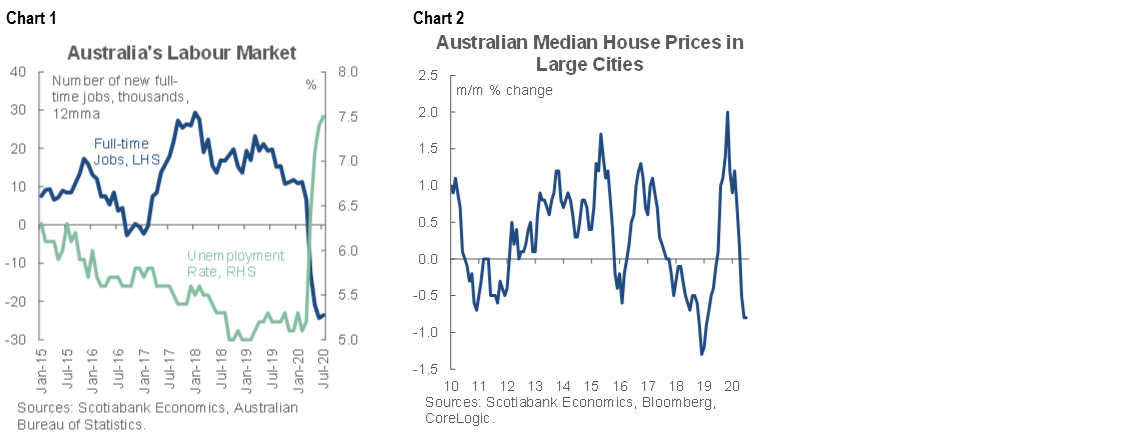

A recovery in household spending and investment will likely be somewhat delayed due to the newly imposed movement restrictions in Victoria. Consumer sentiment remains soft in line with weak labour market conditions (chart 1) and declining residential property prices (chart 2). Business confidence has rebounded, yet the sustainability of the recovery and its impact on real activity are highly dependent on the virus trajectory. Australia entered the COVID-19 crisis with healthy public finances; accordingly, it is in a solid position to support economic activity with higher public outlays until the recovery is well underway. Announced fiscal stimulus measures include direct payments to households, wage subsidies, incentives for private investment, and measures to support affected regions and communities. The Australian government unveiled a “mini-budget” on July 23, which laid out the nation’s fiscal roadmap. The federal budget for the current fiscal year (July–June) was delayed until October due to the virus outbreak. The July update showed that the underlying cash deficit for fiscal year 2020–21 is expected to reach 9.7% of GDP vs. the government’s pre-pandemic goal of reaching a small surplus.

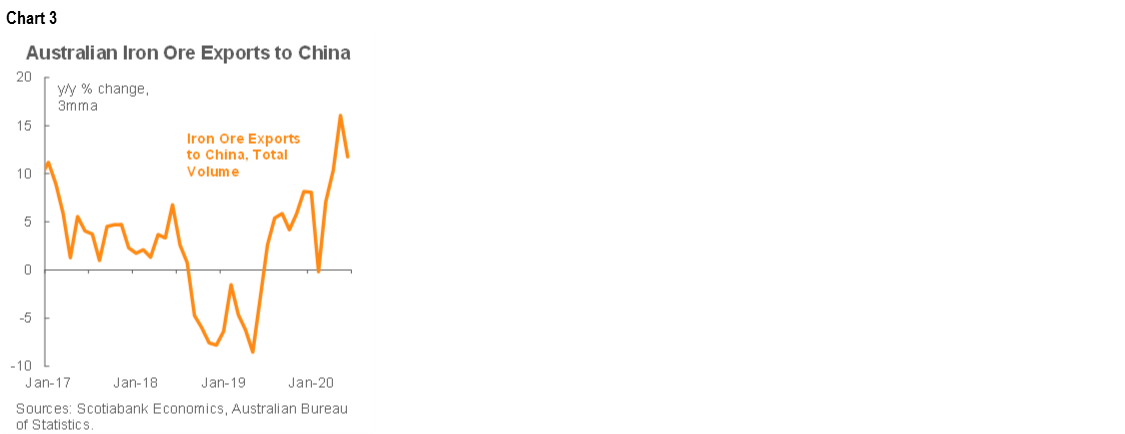

Escalating tensions between Australia and China cloud Australia’s external sector outlook; China is Australia’s most important market, purchasing 42% of its total exports and 80% of its commodity exports. The bilateral relationship has been somewhat strained for some years already, yet it tensed up significantly in April following Australia’s call for an international inquiry into the origins of the COVID-19 outbreak. Since then, China has slapped an 80% import tariff on Australian barley, banned beef imports from certain producers, and warned its citizens against travelling to Australia. Meanwhile, Australian authorities have advised that Australians may be at risk of arbitrary detention in China and have suspended the country’s extradition treaty with Hong Kong after China imposed the National Security Law on the territory. As the latest move, China launched anti-dumping investigations into Australian wine shipments to China. At this point, we assess that the direct economic harm for Australia caused by China’s retaliatory measures remains manageable (barley and beef account for only slightly over 2% of Australian shipments to China, while international travel is limited due to the pandemic). However, if the dispute intensifies, other agricultural products, such as wine, dairy, or fruit, could be adversely impacted. The biggest risk related to the conflict is that China’s retaliation spreads to mineral products/iron ore. Around 83% of Australia’s iron ore shipments—the country’s most important export—are destined to China. Nonetheless, we see such an escalation as a distant scenario given that Australia is a critical iron ore supplier to China; for now, the diplomatic dispute has not had a visible impact on the countries’ iron ore trade (chart 3).

INFLATION, MONETARY POLICY AND AUSTRALIAN DOLLAR OUTLOOK

Inflationary pressures will remain muted in Australia over the coming quarters due to significant spare capacity in the economy, high unemployment and low wage gains. Headline prices declined by 0.3% y/y in the second quarter (chart 4). While some of the underlying factors, such as dropping child care costs, are expected to reverse in the near future, we forecast headline inflation to climb only moderately, closing 2020 at 0.4% y/y. Inflation will likely accelerate gradually over the course of 2021 as the economy normalizes, yet we anticipate it to remain below the Reserve Bank of Australia’s (RBA) target range of 2–3% y/y through 2021. Weak demand-driven price pressures will allow the RBA to maintain accommodative monetary conditions in the foreseeable future.

In March, the RBA responded to the COVID-19 shock with notable conventional and unconventional monetary policy measures. The benchmark cash rate has been lowered by a total of 50 basis points this year to 0.25%, following cuts of 75 bps in 2019 (chart 4). The RBA has also adopted yield targeting, aiming to keep the 3-year Australian government bond yield at around 0.25% by buying government bonds in the secondary market as needed. The RBA’s government bond purchases total around AUD55 billion so far, with most of them conducted in April and May. Policymakers remain prepared to scale up the purchases when needed. In addition to the benchmark interest rate cuts and yield targeting, the RBA has also established a term funding facility for the banking system in order to lower funding costs and incentivize banks to provide credit to businesses.

According to the RBA, the yield target is set to remain in place until progress is being made towards the central bank’s goals of full employment and annual inflation of 2–3%. Meanwhile, the monetary policymakers have pointed out that the yield target will be removed before the cash rate is raised. According to Governor Philip Lowe, the cash rate will likely remain at the current level for at least three years. As the economy is responding to the stimulus measures and starting to gather momentum, we do not expect any further monetary easing to be unveiled in the near future.

The Australian dollar (AUD) has strengthened against the US dollar (USD) since its low point in mid-March (chart 5), assisted by climbing iron ore prices and China’s economic recovery. The reintroduced movement restrictions in Victoria seem to have had little impact on the AUD. Nevertheless, we assess that potentially escalating tensions between the US and China ahead of the US presidential election in November will limit the AUD’s upside in the near future. We expect AUDUSD to close 2020 at 0.71.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.