- Canadian small- and medium-sized enterprises (SMEs), which account for a very large share of businesses, employment and overall economic activity in Canada, bore the brunt of the pandemic-related contraction in 2020.

- The second half of 2021 and 2022 should bring growth opportunities to SMEs, with the strongest economic expansion in decades, continued fiscal support measures and accelerated adoption of new technologies. However, the periodic resurgence of the virus, as well as acute supply chain strains will require continued resilience and adaptability on the part of entrepreneurs.

- In the medium term, ambitious immigration targets should help alleviate labour shortages in some industries that emerged as the number one concern among business leaders.

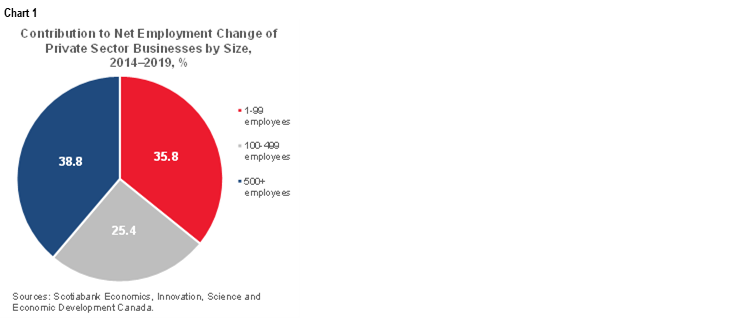

The Canadian economy has its share of business giants, from auto manufacturers (Magna International) to large integrated oil producers (Suncor Energy) to technology companies (Shopify). However, in many ways the story of the Canadian economy is written by small and medium-sized businesses (SMEs), which are ubiquitous across all industries and account for a very large portion of economic activity (see here). As of 2019 they accounted for almost 90% of the private sector employment and more than 99% of Canadian business establishments, contributed over 60% of the overall net increase in employment in the five years through 2019 and accounted for over 50% of the level of Canadian GDP.

While the size of their economic contribution is significant, the role of SMEs in the Canadian economy, society and on the global stage does not end there. For Canada, being an open economy with a large international trade sector, bilateral trade relationships are incredibly important. Given the predominance of SMEs in Canada, it is no surprise that SMEs are the custodians of these trading relationships, as over 97% of exporters have fewer than 500 employees, although this share varies by industry.

Canadian SMEs are able to capitalize on international trading opportunities in part because of the deep pool of highly educated and talented workers. Those born outside of Canada play an additional role, with 1 in 4 SMEs being led by immigrants (as of 2017, see here), a share that is higher than that of immigrants in the overall population. More often than not having an established network of contacts in the country of origin, business owners born outside of Canada are significantly more likely to engage in international commerce than their Canadian-born peers (see here). Thus Canada’s diverse population helps build commercial networks that sustain Canadian trade.

Success in the global economy increasingly depends on the ability to innovate new products, technologies and processes. In Canada, innovation occurs in businesses of all sizes. While larger firms with over 500 employees are more likely to own at least one type of formal intellectual property—73% of these firms do—SMEs have a surprisingly high share of companies with intellectual property ownership: 13% of firms with 1–4 employees own some intellectual property, the share rising to 49% in the case of companies with 100–499 employees. Given the sheer number of SMEs in the Canadian economy, it is clear that SMEs contribute to Canadian innovation in a significant way.

This is reflected in such metrics as the share of high-growth firms among SMEs. By revenue, over 2014–17 more than 10% of the firms in the information and cultural industry were identified as high-growth, with 9% in construction and 8% in manufacturing.

PANDEMIC STRIKES

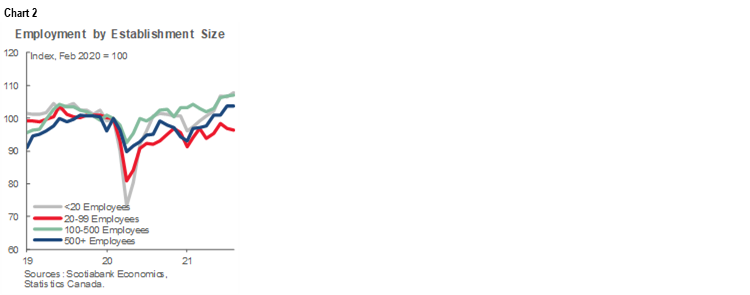

This engine of economic growth was severely disrupted in 2020 by the emergence of the COVID-19 pandemic and the resulting public health measures that shuttered companies for months in Canada and other countries. Restaurants, shops and other high-contact establishments were unable to serve customers in person, while merchandise trade collapsed, pulling the rug from under countless exporter firms. Small and medium-sized businesses bore the brunt of the lockdown measures and the disruption in international trade, accounting for most of the employment losses (chart 2) with hundreds of thousands of firms seeking government relief under support programs such as the Canadian Emergency Wage Subsidy (CEWS). Between May 10th and June 6th, 2020 at the peak of CEWS applications, businesses with fewer than 251 employees accounted for 97% of applicants.

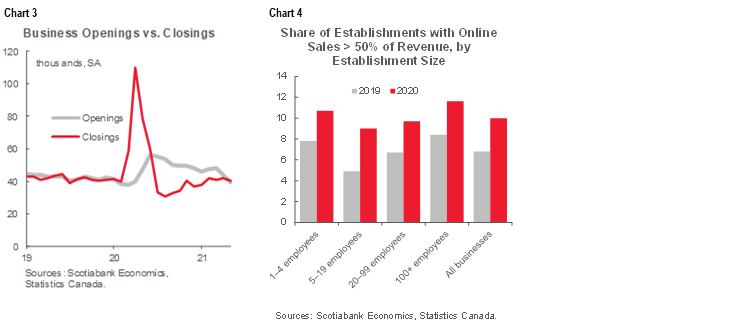

The numbers of business closures spiked, but once the restrictions started to be lifted new businesses sprang to life (chart 3). In part this speaks to the adaptability of the Canadian entrepreneurs and business owners, who pivoted to new technologies when restrictions disrupted existing ways of doing business. One example is an embrace of e-commerce, with the share of firms who obtain more than 50% of revenue from online sales rising for all business sizes between 2019 and 2020, although this also reflects the restrictions on in-person business during the pandemic (chart 4). The shift was more pronounced for firms with 5–99 employees, and is a particularly welcome development given that these strata were previously underutilizing this technology compared to the Canadian average. Given the rapid evolution of the way businesses operate in Canada, a new spurt of innovation may be coming and SMEs should stand to benefit the most.

In contrast to the overall impact, some sectors dominated by SMEs were less affected by the pandemic, with construction and real estate being the most notable, fully recovering to the pre-pandemic level in terms of GDP (chart 5).

ACTIVITY RISING, DESPITE DELTA, SUPPLY CHAIN DISRUPTIONS

While SMEs have not yet recovered from the pandemic, with employment continuing to languish below the pre-pandemic levels particularly in the 20–99 employees category (chart 2 again), SMEs make up most of the employment gains since April 2020, with 75% of net job gains occurring at firms with fewer than 100 employees.

Consequently, the business community has been remarkably optimistic. Before easing somewhat in September on the implications of new pandemic restrictions and vaccine mandates, the CFIB’s business barometer of the 12-month outlook had hovered at levels not seen in years (see chart 6 and here). In fact, business owners now rank shortages of skilled labour as the number one factor limiting sales growth, overtaking weak demand, which was the number one concern through the pandemic.

No wonder, since demand in a number of industries has been skyrocketing, in part buoyed by the significant fiscal support, in part as consumers switched spending from temporarily restricted categories—international travel, restaurant meals, even clothing—to others, such as home renovations, electronics, cars and housing.

As vaccinations in Canada proceed apace, demand is likely to rotate to previously-closed high-contact sectors. This should allow the red-hot parts of the economy to cool, alleviating some of the supply chain strains—allowing production to catch up to demand and cooling the rising input costs (here). However, the rise in demand at high-contact businesses is running up against a pervasive shortage of workers, as well as supply chain disruptions causing everyday items to be in short supply.

Overall we expect supply chain disruptions to gradually improve over 2021–2022. While there were tentative signs of stabilization in some areas, with Statistics Canada reporting that in July of 2021 automakers managed to secure increased supplies of microchips, raising production and wholesale exports of autos, the escalating infections in Southeast Asia prodded other auto makers to curtail production globally. The consequences of the global dislocation in international trade and shipping may also take a while to work through. Shipping delays and skyrocketing costs due to reduced processing capacity at ports and lack of shipping vessels and containers at key shipping terminals will likely linger into 2022.

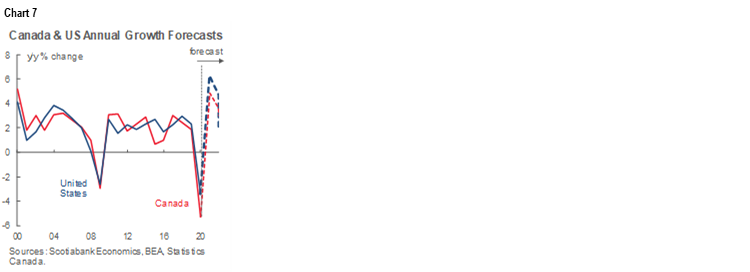

Despite the supply challenges, 2021 is expected to see an incredibly strong expansion in Canada and its main trading partners, including the US.

- In the US, a rapid, albeit now slowing, vaccination campaign allowed for a gradual lifting of pandemic restrictions and unleashed pent-up demand for goods and services. In addition, several rounds of fiscal stimulus, including the most recent infrastructure spending plan, should help supercharge the recovery and further speed up employment growth. In this environment, the US GDP is expected to grow 6.3% in 2021, the highest rate in decades (see chart 7).

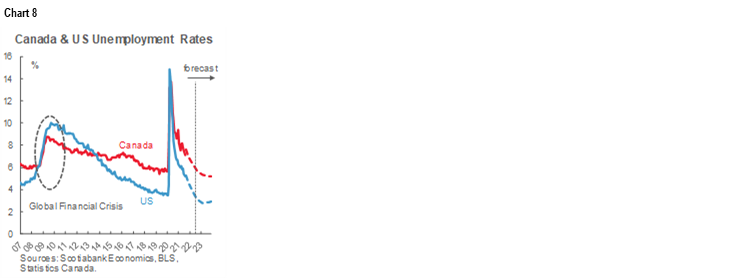

- Strong growth south of the border is expected to boost Canadian exports, adding to internal pent-up demand, leading to an acceleration in the second half of 2021 with the overall Canadian growth at 4.8% for the year, before a gradual slowing to 3.6% in 2022. Such strong growth is expected to leave the Canadian unemployment rate at a record-low level of 5.2% by the end of 2023 (chart 8).

Given such rapid growth, albeit tempered by supply challenges and the likely periodic re-emergence of virus waves, the next few years present a once-in-a-lifetime opportunity for SMEs to rebuild and grow their business, expand into new markets, develop new products and in general position their firms for long-term success. In particular, the industries where output has not materially recovered from pandemic lows, such as arts and recreation, accommodation and food services and others (see chart 5 again) should benefit from the economic expansion. However, taking advantage of these opportunities will require entrepreneurs to remain nimble and take risks in an environment where delay may mean more difficulties sourcing inputs and hiring skilled labour, or loss of market share to competitors. It will also require resilience, as the road ahead is likely to be bumpy, even as the trend is clearly up.

POLICIES, CHALLENGES, OPPORTUNITIES

There is no doubt that the Canadian economy, once it emerges on the other side of the pandemic, will look quite different. The cataclysmic event that is the COVID-19 pandemic has already led to deep changes in its structure, sharply accelerating its digitalization among other shifts. SMEs are well-positioned to take advantage of this trend, given the speed with which they adapted to doing business in the past year. In this task the business owners will continue to enjoy government support. Federally, the 2021 budget included a series of measures intended to assist SMEs with transition to the digital age, incentives for business investment, as well as the extension of CEWS and other support programs. In addition, the announcement of very aggressive immigration targets (here), if they are reached, should help address skilled labour shortages reported by business owners, in addition to increasing the pool of would-be entrepreneurs in Canada.

In the medium term, an important trend that is expected to accelerate is the implementation of measures to address the issue of climate change. The Canadian government, and increasingly governments around the world, continue to align policies to reduce greenhouse gas (GHG) emissions, with Canada committing to net-zero emissions by 2050. While this will raise costs for businesses that emit GHG, in particular in the oil and gas and transportation industries (see chart 9), it will likely help spur innovation in clean technology and Canadian SMEs are well-placed to participate in this. The Canadian Venture Capital and Private Equity Association report showed that funds raised by clean technology companies in Q1-2021 already far surpassed the total for all of 2020.

On the clean technology adoption side, in a 2021 survey, about 12% of companies with 20–99 employees stated that they planned to make investments in renewable energy or implement energy efficiency measures. While this might seem small, the number of companies in this size range is very large and so the impact may be substantial.

CONCLUSION

Stars are aligning for better days beyond COVID-19. With strong growth in Canada and the US anticipated in the short term, and—in the medium term—accelerated adoption of new technologies, rising immigration and continued fiscal support, SMEs should enjoy plenty of opportunities not only to recover to pre-pandemic levels, but to thrive and continue to succeed in the competitive global environment.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.