- We estimate that government consumption and pandemic transfers to households account for about 200 basis points of the 475 basis points increase in the Bank of Canada’s policy rate.

- This reflects the large and persistent increase in government consumption by all levels of government in Canada since the end of 2019 and the Federal support programs for households rolled out during the pandemic.

- Given that provincial government consumption of goods and services is more than triple that of the Federal government, provincial spending alone accounts for about a third of the increase in the policy rate.

- Some of the rise in government consumption of goods and services was likely desirable and necessary given population growth and ageing but those expenditures were inconsistent with inflation control and led to higher interest rates.

- Overall, our results suggest fiscal policy at all levels of government has been badly mis-calibrated from an inflation management perspective.

There is no doubt that the Bank of Canada’s interest rate policy is causing hardship for Canadians. This hardship is registering at a political level. There is no better example of this than the extraordinary letters written by some Premiers to the Governor of the Bank of Canada, imploring him to hold off on additional increases in interest rates. Setting aside the concerns we have about these political attempts to influence the BoC, it is unquestionably the case that fiscal policy at all levels of government have contributed to the current level of the policy rate. We attempt to quantify the impact of fiscal policy on interest rates and conclude that roughly 200 basis points of the 475 basis points increase in the policy rate stems from consumption at all levels of government combined with Federal pandemic support programs. In other words, absent actions taken by all levels of government, the policy rate would need to be about 3%, at the high end of the Bank of Canada’s estimate of the neutral policy rate.

Fiscal policy influences the economy in a number of dimensions. We focus on two key channels in our analysis: government final consumption of goods and services (the G in national accounting) and transfers to households. Each of these channels impact the economy in different ways: G impacts economic activity directly whereas transfers impact the saving and spending behaviour of households. A rise in either lifts GDP, the former having a more direct and larger impact than the latter. We exclude government investment in fixed capital from our analysis as there is a closer relationship between that and potential output and the ratio of government capital investment to GDP has remained roughly stable over the last decade.

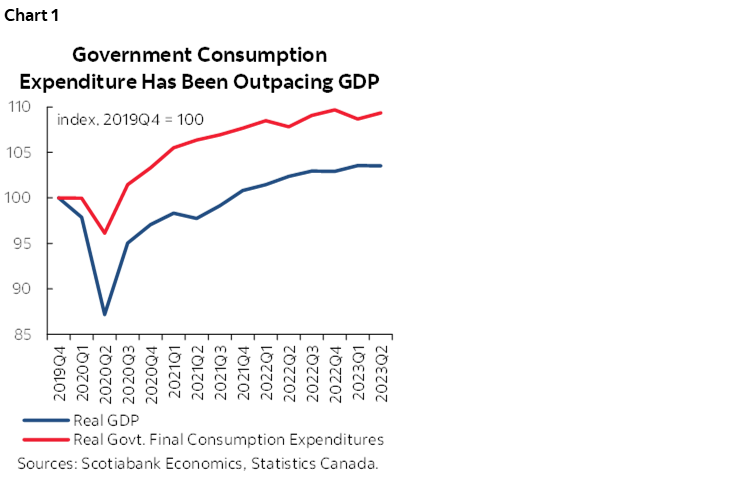

Government final consumption on goods and services has risen sharply since the end of 2019 across all levels of government. Since this rise has been more rapid than GDP growth, the share of government spending in relation to economic output has risen substantially (chart 1). This has had a large impact on the economy. Put in a monetary policy context, the economy would not have been in excess demand were it not for this surge in government spending.

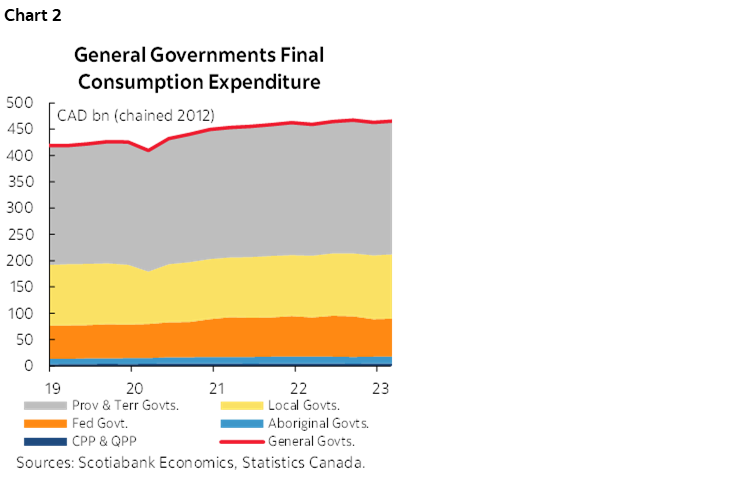

Statistics Canada breaks down government consumption by level of government allowing us to determine which levels of government grew more than others, but more importantly, which level of government’s consumption spending had the most impact on the economy. From chart 2, we see that Federal consumption spending has risen a bit more rapidly than other levels of governments since end-2019. However, spending by other levels of government represents a multiple of Federal spending. Provincial spending is more than triple Federal spending. Spending by municipalities and other governments is 50 per cent larger that of the Federal government. Looking at the contributions of these levels of government to economic growth since 2019Q4, it is clear that provincial spending had a much larger impact on GDP than other levels of government.

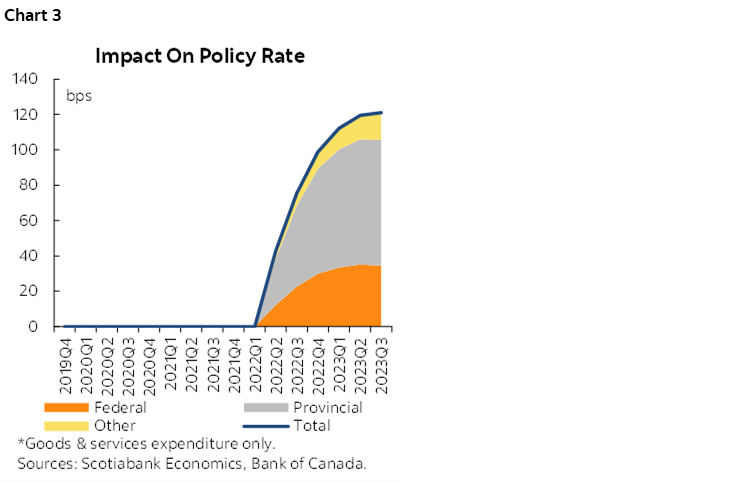

The implications for monetary policy from this are clear. All levels of government have contributed to the recovery in post-pandemic output. Of these, the provinces had the most impact. We can estimate the impact of these policy decisions on monetary policy using our model of the Canadian economy. We do this by simulating the path of real government spending from 2019Q4 onwards using actual data and estimating how that would have impacted output, inflation and ultimately the policy rate. Importantly, we assume that the lower-bound remained a constraint on the policy rate—that is that the Bank of Canada would have kept its policy rate at 0.25% until it ultimately chose to raise policy rates in the first quarter of 2022.1 This exercise points to a very significant impact on policy rates from government consumption at all levels of government. At the aggregate level, government consumption necessitated roughly 120 basis points of tightening by the Bank of Canada (chart 3). This is about a quarter of the total rate increases implemented by Governor Macklem. Of that 120 basis points, more than half results from provincial spending decisions (70 basis points). The remainder is split between the Federal government (30bps) and municipal and other levels of governments (20bps).

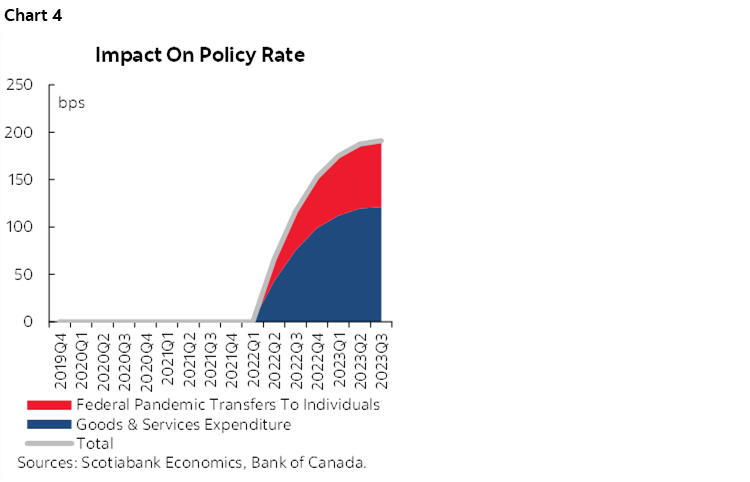

We also examine the impact of Federal pandemic transfers to households on the interest rate path to get a sense of the full fiscal impact of COVID and post-COVID fiscal policy. There too the impacts on monetary are substantial given the sums involved (chart 4). We estimate the impact on policy rates to be about 80 basis points. This is exclusively attributed to the Federal government.

Taken together, rising government consumption and the pandemic transfers account for roughly 200 basis points of the 475 basis points increase in the Bank of Canada’s policy rate. There is thus no question that fiscal policy at all levels of government in Canada have played a significant role in the stance of monetary policy. That being noted, it is also clear that the Canadian dollar would have been significantly weaker had interest rates not followed those in the US as closely as they have. That would have pushed inflation higher and so it is likely that some of the rate increases observed in Canada that are attributable to fiscal policy might have occurred to minimize exchange rate passthrough.

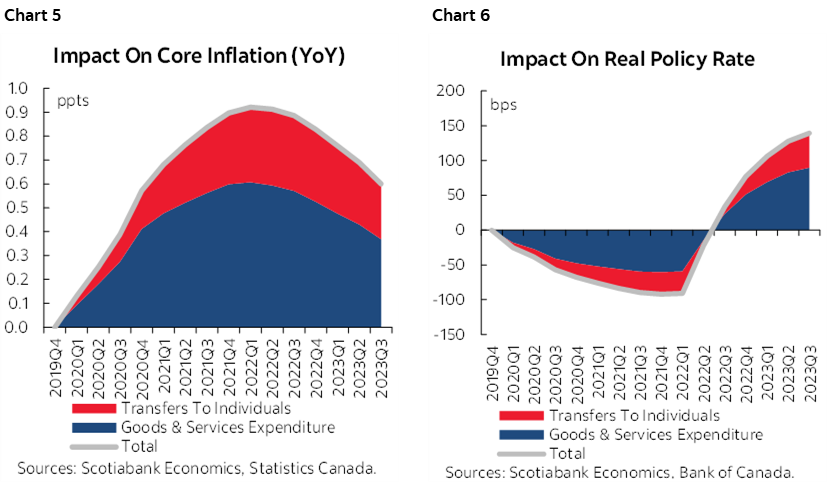

While it may be tempting to conclude that required rise in interest rates crowded out private spending, this may not have actually been the case so far. In fact, we estimate that until recently consumption and business investment have been higher as a result of the rise in government support. This counter-intuitive result is linked to the fact the interest rates in Canada were at the lower bound of 0.25% in the quarters following the pandemic. The surge in transfers and government consumption spending led to higher inflation, which then lowered the real policy rate (which is equal to the nominal policy rate minus expected inflation). This is clearly seen in charts 5 and 6: higher government spending and pandemic transfers raised inflation and pushed down the real policy rate by around 100 basis points, effectively increasing the amount of monetary stimulus in the economy. The resulting reduction in real interest rates temporarily boosted consumption and investment above and beyond what would have occurred given the rise in transfers alone. Business investment remains higher today than would have been the case absent the rise in spending and transfers but consumption and residential investment are now below where they would have been absent the rise in government consumption. Moreover, as much of the rise in government consumption relates to an increase in public sector employment, it may also be the case that our pitiful productivity performance reflects in some part the shift of labour resources away from the private to the public sector.

The exaggerated impact of fiscal policy at the lower-bound of interest rates is a well-known effect. It makes fiscal policy a much more powerful tool in combatting negative economic shocks in those circumstances. This can be very helpful when lots of firepower is needed to support a weak economy or low inflation. It can also cause problems when too much support is provided, whether that relates to the magnitude of the fiscal support or its duration. This was definitely the case in Canada. Real government spending rose much more rapidly than real GDP since late 2019 (chart 1, again). There was nothing temporary about the surge in government consumption. Pandemic transfers, on the other hand, were temporary but extremely large and kept in place too long.

There is no question in our minds that fiscal policy has complicated the task of monetary policy in Canada. Interest rates are substantially higher than they would be had government consumption spending at all levels of government remained fixed in relation to GDP. That being said, the size of the Canadian population has exploded in recent years. Combined with an ageing population, the needs for government services have risen dramatically. Some rise in spending was inevitable and desired. How much of that increase is justifiable is debatable, but there can be no doubt that a consequence of that increase is higher interest rates.

Overall, our results suggest that fiscal policy was badly mis-calibrated since the pandemic from an inflation management perspective. All levels of government are responsible for this. This is not meant to absolve the Bank of Canada of responsibility for the current rate environment. We remain of the view that a number of mistakes were made on the monetary front, but the larger errors seem to have been committed by fiscal authorities. We quite literally cannot afford to repeat these errors in upcoming budgets.

1 This assumption impacts the timing of the change in stance of monetary policy but not its overall rise.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.