- The economic stakes of the upcoming U.S. presidential elections are high. We examine the potential impacts of high-level tax proposals by President Biden and former President Trump along with the latter’s suggested tariff increases and threats to deport illegal immigrants.

- The scope for tax policy changes hinges largely on the make-up of Congress, but the impact of those policies, whether the hikes proposed by President Biden, or the cuts proposed by former President Trump, pale in relation to the impact of the proposed tariff hikes.

- Given their unilateral nature, former President Trump’s proposed 10% across-the-board increase in tariffs, with a special 60% carve-out for China, would effectively be the launch of a trade war, with damaging impacts on the United States and the rest of the world.

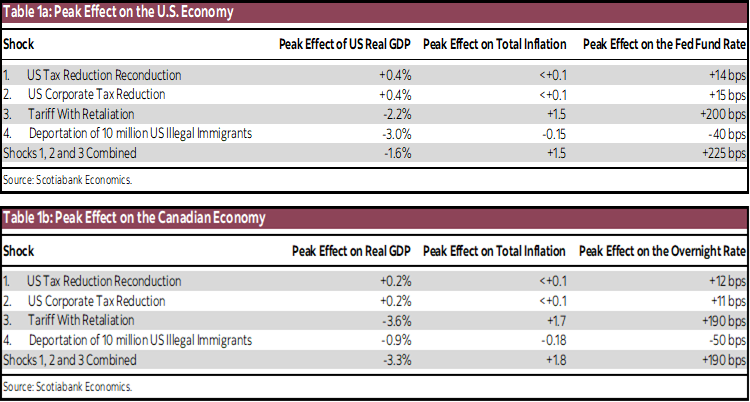

- Assuming other countries respond to higher U.S. tariffs with equivalent tariffs of their own, we would expect substantial negative impacts on U.S. economic activity, including a peak decline of over 2.2% in GDP relative to current forecasts, a peak inflation impact of 1.5% relative to the current view, and a 200 bp rise in policy rates relative to the current expected path for U.S. rates.

- Given Canada’s greater reliance on trade, the imposition of tariffs on all exports to the United States would lead to even greater economic harm north of the border, with a forecast peak decline of over 3.6% in the level of economic activity relative to current forecasts, inflation that is 1.7% higher than currently expected, and policy rates that are 190 bp above the current expected path for the Bank of Canada.

- A scenario in which Canada-United States-Mexico Agreement (CUSMA) countries are excluded from the tariffs dramatically reduces the negative impacts on Canada from higher U.S. tariffs, as would a scenario in which Canada does not retaliate with higher tariffs of its own. This suggests a strong motivation to negotiate a carve-out for Canada and Mexico, even though the United States will hold the much bigger end of the stick in those negotiations, given differential impacts.

- Equally important, the risks posed by a Trump presidency on the trade front represent another clarion call to find solutions to our chronic productivity issues. Greater productivity would provide the Canadian economy with a strengthened ability to withstand shocks, particularly when they originate in the international trade space.

- One can certainly debate the extent to which these simulations results are accurate. They rely on simplified assumptions, but the directional impact seems clear: with the exception of tax hikes, all policies proposed would be inflationary to some degree and would lead to a higher path of interest rates relative to the current view.

- A very important caveat: our analyses do not incorporate any geopolitical impacts or consider the potential for civil disruption (regardless of who wins); they assume the U.S. sovereign risk premium remains unchanged, despite a likely deterioration in federal finances; and they do not consider the impact of heightened policy uncertainty on the outlook. Each of these could have material impacts on the outlook.

The U.S. electoral spectacle is rightly capturing global attention. While much is made of each candidate’s personal qualities, the stark difference between the candidates also applies to economic platforms. This note assesses the potential consequences of both candidates’ platforms as they are currently articulated. We devote more attention to former President Trump’s plans, given that many of them seem more likely to be implemented than those currently laid out by President Biden. While there is of course much uncertainty regarding the eventual winner, with polls suggesting a roughly 50-50 chance of victory for both candidates, there is also much uncertainty regarding the policies each will pursue and implement. One thing appears certain, however: a Trump victory and follow-through on the policy side would likely see higher inflation than what could be expected in a Biden victory. Were Trump to implement the more controversial elements of his platform, namely the imposition of tariffs on all U.S. imports and the effective launch of a trade war, and the mass deportation of illegal immigrants, we would also expect substantial economic impacts in the United States and its trading partners. In that eventuality, large reductions in economic activity could be expected in the countries most dependent on U.S. trade (i.e., Canada and Mexico). Given the uncertainty around potential and eventual outcomes, this note follows the “pick-your-own adventure” format. We estimate the economic impacts of various policies on the United States and Canada individually so that readers may construct economic impacts based on what they believe to be the most likely outcome of the election and the eventual policies undertaken by the winner.

A critical enabler or obstacle to either winner will be the composition of the House of Representatives and the Senate. It seems likely at this point that neither party will control both chambers following the election. This would effectively mean that presidential ambition may be limited to actions taken outside the legislative process. This could preclude tax changes or large expenditure appropriations. That being said, U.S. politicians seem relatively unconcerned about fiscal dynamics, as witnessed during the last two administrations, and we consider it more likely that proposals to reduce taxes, such as those proposed by Trump, are more likely to be implemented than tax hikes, such as those proposed by Biden.

We focus our analysis on high-level tax, tariff, and immigration policies by using our macroeconometric model of the U.S. and Canadian economies. Our model allows us to consider the impact of aggregate changes in corporate and personal income tax and tariff policies. By aggregate, we simply mean that we can model the impact of changes in corporate taxes to GDP, for instance, but not the incidence of specific changes in corporate tax policies. The same is true for personal income taxes and tariffs. This aggregative impact definitely masks some of the complex ways in which policies impact the economy, but we believe it to be a reasonable approximation of total impacts. We do not, for instance, calculate the impact of tariffs on household budgets, nor do we estimate which industries stand to benefit or gain from these policies (though there are going to be winners and losers from distortionary tariff policy).

The results of the range of scenarios considered are laid out in table 1. It is readily apparent that tax increases in a Biden win, assuming Congress allows that to happen, or tax cuts under Trump would have reasonably minor impacts on economic activity. At the margin, tax increases would reduce growth and inflation, allowing for lower policy rates, while tax cuts would generate the opposite. Tariffs would have a much larger impact, but that impact depends on whether or not countries retaliate. In a world where tariffs of 10% are imposed on all imports into the United States, with the exception of those from China, which face a 60% tariff, U.S. economic activity would fall by 2.2%, while inflation and policy rates would rise by 1.5% and 200 bp. For Canada, the impact of this policy would be substantial given the outsized importance of the United States as a source of imports and destination for exports. Canadian economic activity would be 3.6% lower, with monetary policy rates rising to counter the inflationary impacts of the tariffs. We also simulate an outcome where tariffs are imposed as proposed by Trump but in which the USMCA countries are excluded given the trade agreement governing trade between all three countries. In such a scenario, the economic impacts on Canada are dramatically reduced. Finally, we consider the impact of the mass deportation of illegal immigrants in the United States, as proposed by former President Trump. The deportation of roughly 3% of the U.S. workforce would be highly damaging to the U.S. economy, with U.S. GDP falling by about 3%, leading to lower inflation and policy rates.

In the sections below, we provide more details on each of these scenarios and the key assumptions underlying them.

Higher Personal Income and Corporate Tax Rates Under Biden or Lower Personal Tax and Corporate Rates Under Trump

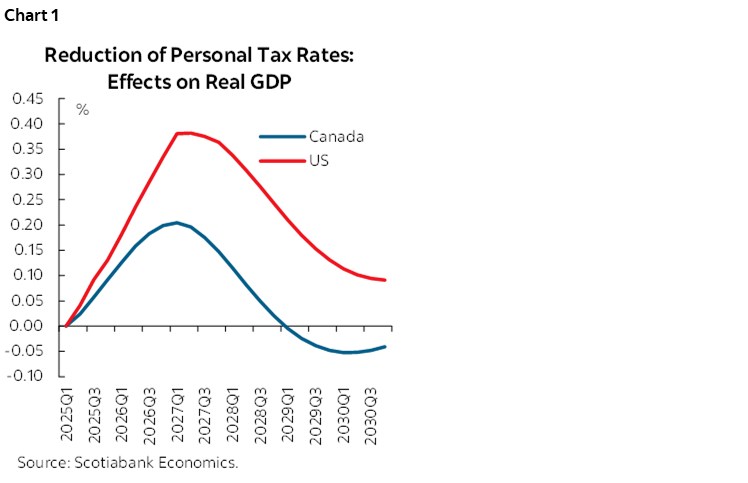

If elected, Trump is likely to reconduct the tax cuts that he temporarily put in place back in his first mandate. We, therefore, simulate the reconduction of income tax reduction equivalent to 1.1% of GDP, which boosts U.S. real GDP by 0.4% in the short term (via an increase of consumption and investment) and by 0.1% in the long run, as the tax reduction slightly increases the incentives to work more. See chart 1.

Inflation and the policy rate rise by less than 0.1% and by 14 bp, respectively. In Canada, the shock is essentially a positive trade and wealth-related demand shock. Canadian real GDP increases by 0.2% and inflation and the policy rate temporarily rise by less than 0.1% and by 12 bp, respectively. The shock is moderately positive for U.S. and Canadian stock markets and bond rates increase a little bit.

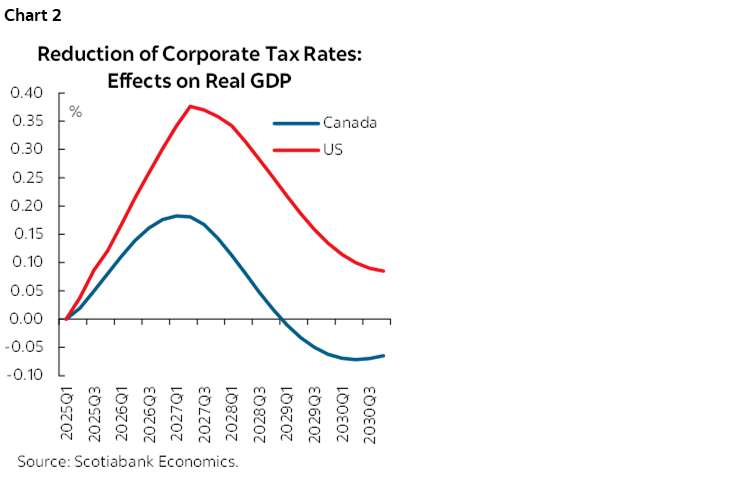

Biden promises to raise the corporate tax, while Trump would like to reduce it. Thus, we also simulate a reduction of the corporate tax under a Trump presidency (or an increase under a Biden presidency) that would create a wedge equivalent to 0.6% of GDP between the two presidencies. This tax reduction increases U.S. GDP by 0.4% in the short term, mostly by stimulating investment. In the long run, GDP increases by 0.1% because the corporate tax reduction gives more incentive to invest. Similar to the tax cuts reconduction case, in Canada, the shock is essentially a trade and wealth-related positive demand shock and GDP increases by 0.2%. See chart 2.

Unilateral Tariff Increases

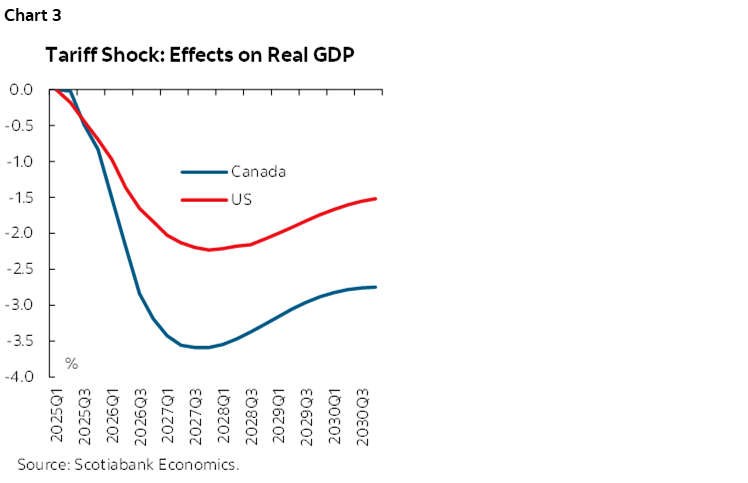

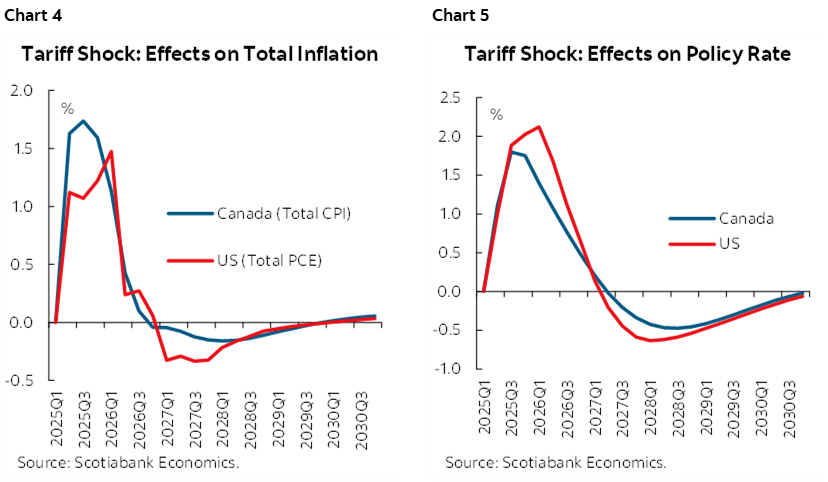

We also assume that Trump will put in place a 10% tariff on U.S. imports from everywhere in the world except from China where he imposes a larger tariff of 60%. We assume that all the countries, including Canada, retaliate and impose an equivalent tariff on imports coming from the United States. This shock is negative for growth for all countries. The negative effect on growth on all countries is explained by trade and supply chains disruptions, misallocation of resources and production, trade uncertainty, increases of the price of intermediate inputs of production, and a negative wealth effect (fall in equity markets). Since we assume that the tariff shock is permanent, the shock generates a permanent fall of GDP worldwide. In the United States, the level of real GDP falls by 2.2% in the short term and by 1.5% in the long run. Because Canada is a more open economy and is very exposed to U.S. trade, real GDP drops even more (-3.6% in the short term and -2.8% in the long run). See chart 3.

The increase of the price of imports worldwide, combined with disruptions of supply chains, push inflation up for around two years. In both the United States and Canada, the policy rates rise to fight the increase of inflation. See charts 4 and 5.

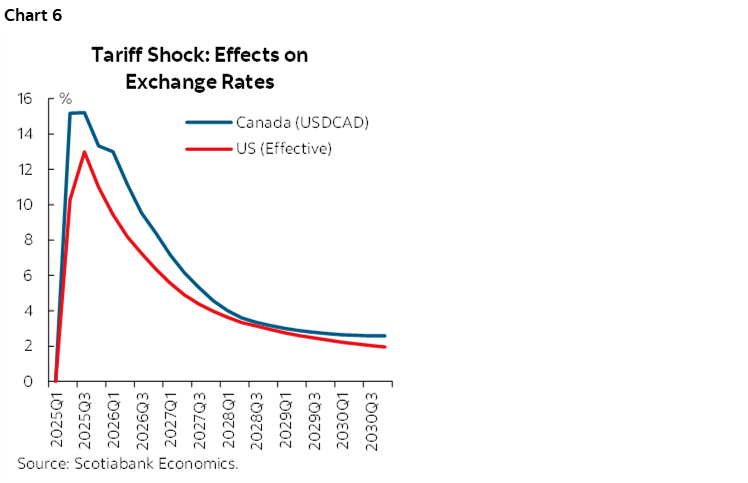

The U.S. dollar appreciates because of the flight-to-quality/safe-haven effect, helping dampen the impact on inflation, as does the reduction in economic activity. The Canadian dollar depreciates because of the drop of the price of oil (less demand) and the flight to quality to the U.S. dollar. The shock is negative for global stock markets and bond rates increase. See chart 6.

Simulations show that Canada (and presumably Mexico) can substantially reduce the effect on their economies by negotiating an exclusion of the CUSMA from the U.S. tariff increase. In that case, Canadian real GDP would only fall by -1.4% in the short term and -0.3% in the long run compared to -3.6% and -2.8%, respectively, if tariffs are also imposed between USMCA members and the United States. It is also in the interest of the United States not to impose tariff against Canada and Mexico because U.S. GDP would only fall by -1.7% in the short term and -1.2% in the long run compared to -2.2% and -1.5% if tariffs are also imposed among USMCA members. It is clear Canada and Mexico have an interest to jointly negotiate a USMCA exclusion with the United States, but it is clear that the United States would carry the much bigger end of the stick in those negotiations.

Deportation of Illegal Immigrants

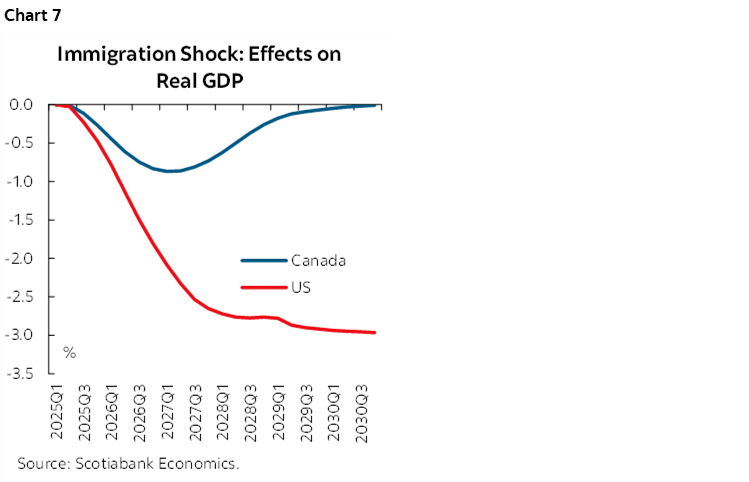

The deportation of roughly 10 million illegal immigrant implies a gradual fall of around 3% of the U.S. labour supply. U.S. employment and real GDP would gradually fall by 3% permanently. See chart 7.

There is a small negative effect on U.S. inflation and policy rate as the U.S. aggregate demand adjusts at a similar pace to the gradual fall of potential GDP; therefore, the U.S. output gap would barely move. The shock is negative for U.S. stock markets but roughly neutral on the bond rates. For Canada, it is essentially a temporary negative demand shock (GDP, inflation, and policy rate fall) through the trade and stock market wealth channels. Canadian real GDP temporarily falls by around 0.9%.

The Most Probable Scenario: Increased Tariffs Combined with Tax Reductions

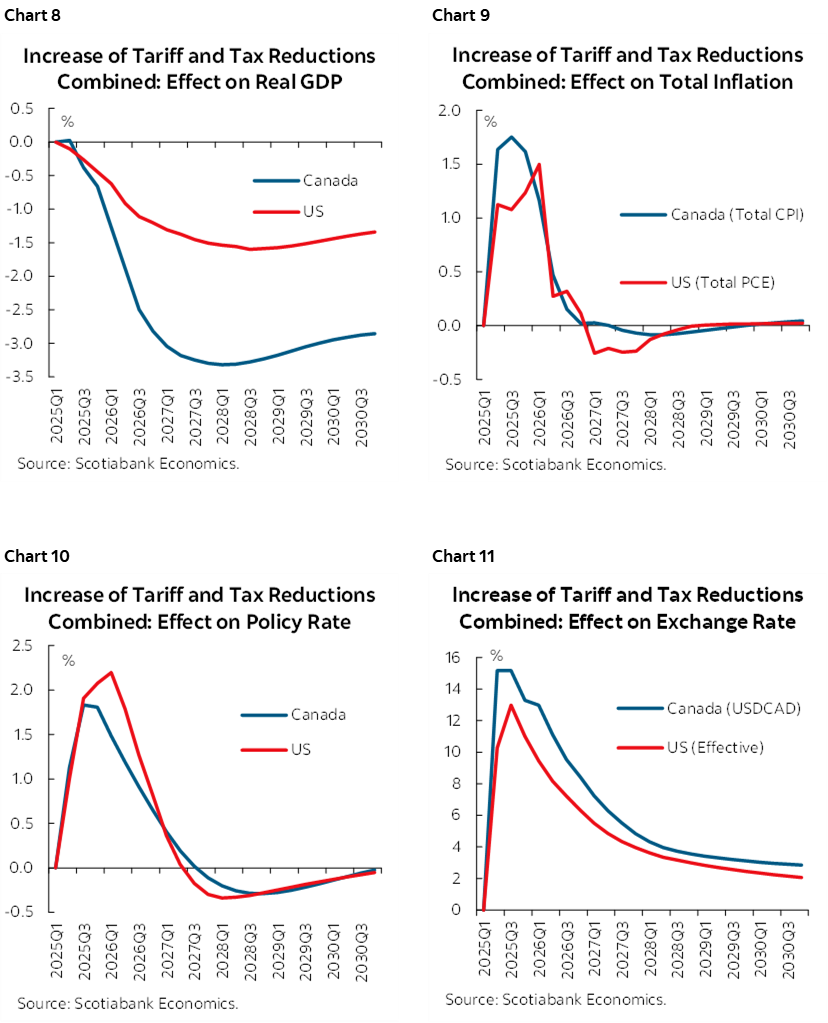

We think that the deportation of 10 million illegal immigrants is politically and logistically infeasible. Therefore, our most likely scenario excludes this immigration policy shock but includes all the other policies previously mentioned, namely the tariffs increase and the reductions in taxes combined. Charts 8 to 11 show the effect of this base case scenario on real GDP, total inflation, policy rates, and exchange rates, respectively. The scenario is dominated by the effects of the tariffs increase, though the effect on real GDP is attenuated somewhat by the tax reductions. U.S. and Canadian GDP falls, inflation increases, and monetary policy reacts to the rise of inflation by increasing the policy rates. Bond rates increase and stock markets falls. According to the macroeconomic fundamentals included in the model, the U.S. stock market should fall by around 10% in 2025 before quickly partially reversing in 2026 (+7%); in the long run, they should be 3% lower than they would have been without Trump’s policies. The U.S. effective exchange rate appreciates because of the safe-haven effect and the price of oil falls because of the decrease of the global economic activity caused by the tariff increase.

All these scenarios make a number of highly simplifying assumptions. Importantly, the scenarios make no assumptions regarding the following:

- An increase in trade-related uncertainty that flows from the threat of tariffs as opposed to the actual implementation of tariffs. We know from Trump’s first term that his threats and actions created a dramatic increase in measured trade policy uncertainty. The uncertainty reduced economic activity in the United States and elsewhere, despite the beneficial intention of those threats for the United States. Please see this report from 2019 for an estimate of the impact of trade uncertainty on the U.S. economy.

- Non-tariff retaliation by China to U.S. trade actions. It is a near certainty that China would retaliate to such an escalation of trade tensions. One possibility would be to reduce its holding of U.S. Treasuries. This would be complicated, given what would be the likely downward pressure on the RMB, which would require an increase in intervention and holding of U.S. Treasuries to contain depreciation pressures. But it nevertheless remains a possibility, as would an increase in tensions or threats in Asia.

- U.S. fiscal irresponsibility in the form of a further deterioration in the budgetary position could potentially lead to a rise in the sovereign risk premium demanded by purchasers of U.S. government debt. While this has not happened in a material way in recent years, despite the sharp deterioration of the U.S. fiscal position, there may well be a tipping point in the future. A large deterioration in U.S. fiscal dynamics, as seen in the first Trump administration, could lead to higher borrowing costs. We assume no such dynamics in our scenarios.

- We assume U.S. equity markets respond in line with the shift in fundamentals. A cut in tax rates supports equities, while a reduction in growth or rise in interest rates put downward pressure on equities. We know, however, that equity markets rose sharply during Trump’s first presidency. While the scope of actions he is currently contemplating are on net more damaging to growth than what was implemented or floated in his first term, and so should be more harmful to equity markets, there is a chance that equity markets respond more favourably than reflected in fundamentals-based approach. This would raise household wealth and lower the cost of capital. Both could support growth and at the margin add to inflationary pressures.

- No attempt is made to consider post-electoral tensions, regardless of the winner.

- No attempt is made to reflect the potential for heightened geopolitical tensions given former President Trump’s views on Russia and China. The risk being that appeasement or disengagement could embolden these countries to pursue extranational ambitions, with negative consequences to global supply chains and the economic and financial outlook.

Conclusion and Implications for Canada

It may well be that whoever is President next year may opt to forego electoral promises upon assuming office. It certainly would not be the first time a politician walks away from a commitment. Based on the assessment above, that may actually be the most desired outcome in this current electoral cycle. That being said, the risks to the outlook remain important at this point given polling and stated policy intentions.

While we note that Canada could reduce the economic consequences from U.S. trade actions by negotiating a CUSMA carve-out, it would likely have to offer some concessions to U.S. trade negotiators. Those concessions could well be costly to certain industries if that is the route chosen by the Canada side.

Perhaps more importantly, the risks posed by the upcoming election highlight once again the key vulnerability that is weak productivity in Canada. While productivity levels are a key determinant of our standard of living, it is also a critical driver of resilience to economic shocks. This is particularly true for international trade shocks in which national competitiveness is key. While the events described above may not materialize, the risk that they might serve as yet another clarion call to urgently address the vulnerabilities that flow from our weak productivity.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.