CANADA HOUSING MARKET: A TIGHT MARKET THROUGHOUT THE SEASONS

SUMMARY

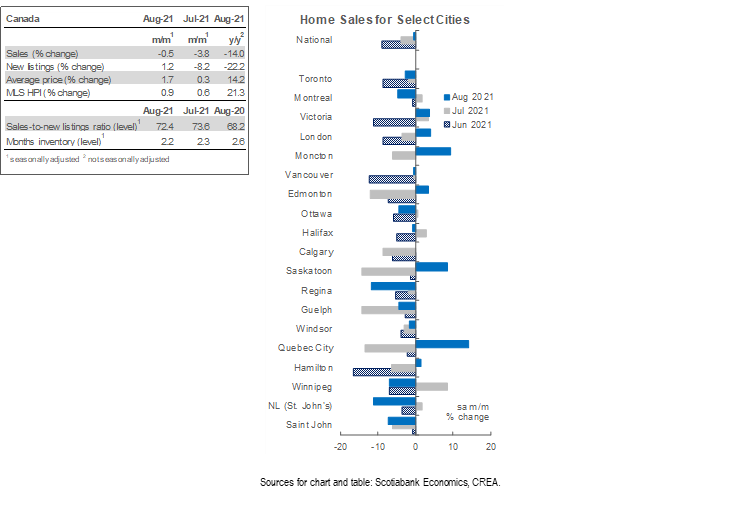

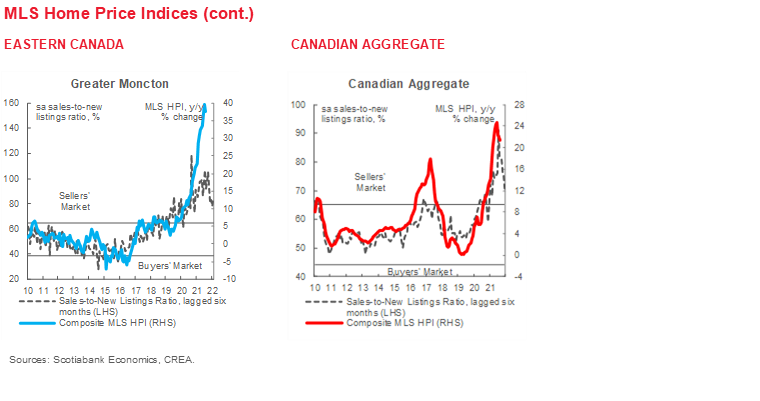

Canadian home sales retreated by 0.5% (sa m/m) in August, the smallest decline in 5 months. Listings edged up by 1.2% (sa m/m) for the first time since March. Despite higher listings, the sales-to-new listings ratio still points to a tight market at 72.4% in August (compared to 73.6% in July, and a long-term average of 54.5%). As a result of this persistent tightness in the housing market, the composite MLS Home Price Index (HPI) rose by 0.9% (sa m/m)—accelerating for the first time since February 2021. Single-family homes were the main driver of the price-gain acceleration in August, with apartments and townhouses holding relatively steady.

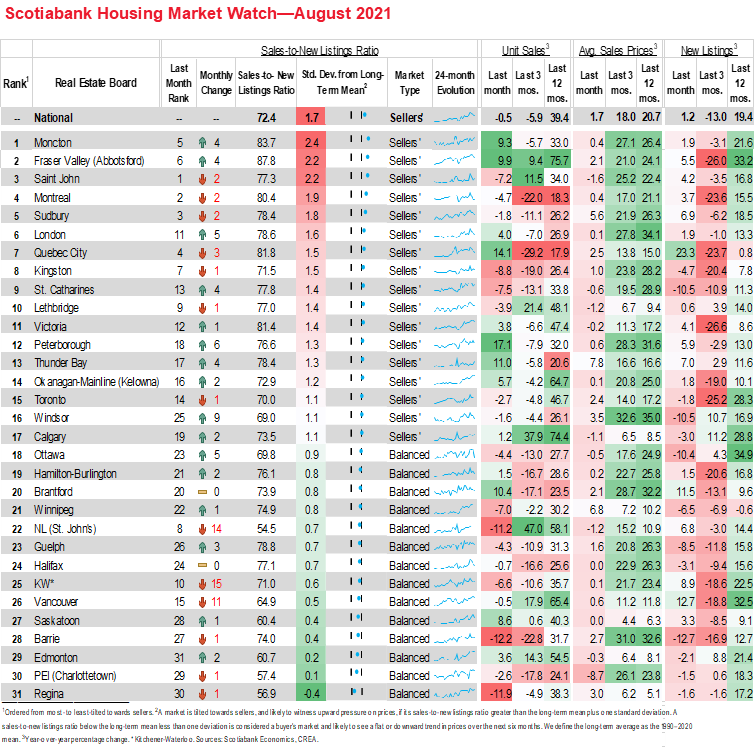

Behind the national decline there was a fairly even split between markets where sales increased and where they decreased. Of the 31 local markets we monitor, sales declined in 18, led by Barrie, Regina, St. John’s, Montreal, and parts of the GTA. These were offset by increases in Quebec City, Fraser Valley, and other parts of the GTA. Despite this net decline, August’s level of sales remains historically strong—the second highest on record for August after August 2020, and 26% (sa) higher than the 2000–2019 August-average.

A small increase in listings was not sufficient to ease the tight-market conditions in August. Similar to sales, movements in national listings were evenly split among markets. Of the 31 local markets, listings declined in 13. Of the remaining 18 markets that added listings, sales went up in 11—pointing to persistent pent-up demand that may be absorbing increased supply as it hits the market. This is best seen in Quebec City, which added the most listings in August (21% sa m/m), and sales surged by over 16% (sa m/m). At the opposite end, Barrie recorded the largest reduction in sales and listings, both falling by more than 12% (sa m/m). The negligible increase in national listings barely made a dent in the sales-to-new listings ratio, leaving 17 of our local centres in sellers’ market territory. Months of inventory fell in August to 2.2 months—better than their lowest level on record in March 2021 of 1.7 months, but still much lower than their long-term average of 5 months.

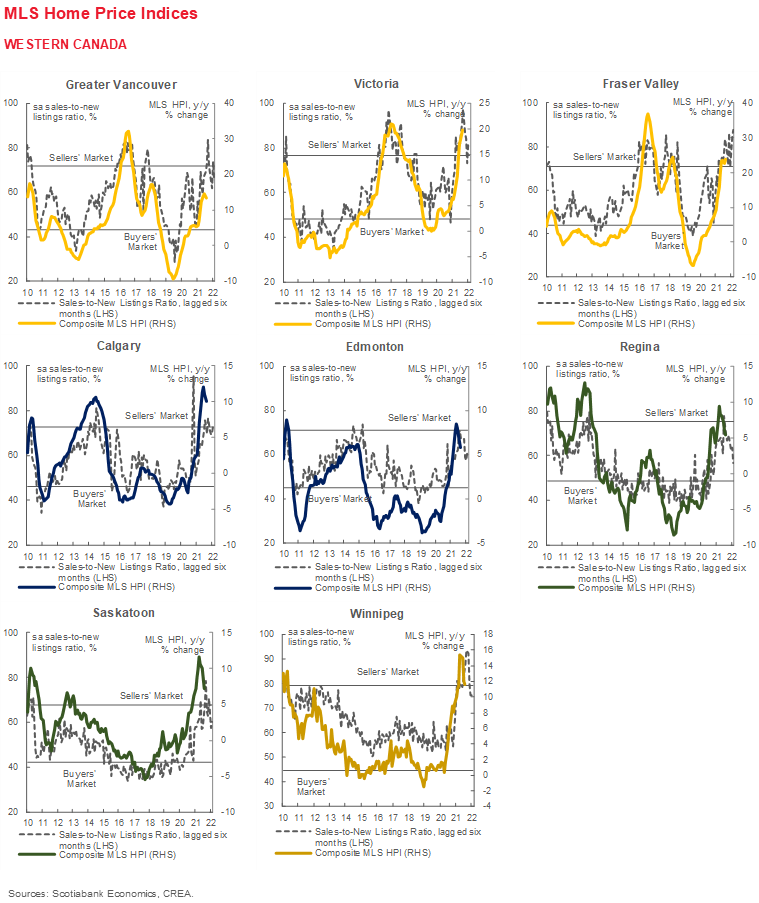

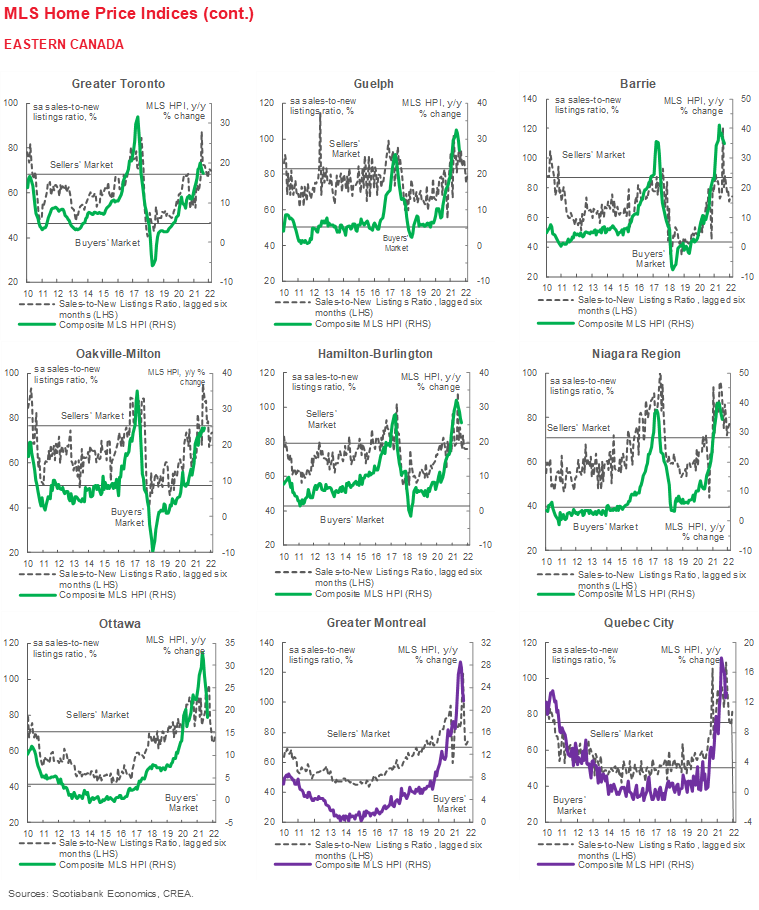

Single-family homes led the acceleration in price gains, while apartments and townhouses held a steady pace. The up-tick for single-family homes comes after 5 months of deceleration, where their price gains cumulatively slowed 5 times as much as the price gains for apartments. Thus, the acceleration in single-family homes may be more indicative of a catch-up than a re-shifting of preferences back to bigger units. On the whole, the growth in composite MLS HPI for all homes in Canada eased to 21.3% (nsa y/y) in August 2021—down from the largest year-over-year increase on record in June.

IMPLICATIONS

As expected, Canadian home sales continued to decline in August, albeit at a much slower pace than in previous months, pointing to a gradual stabilization in transactions, which are slowly getting closer to their pre-pandemic level. The level of transactions in August is nevertheless significantly higher than historical norms, as it is the second highest level of sales ever witnessed for the month of August, after August 2020. Despite the small reduction in sales, the market is no less tight, as the sales-to-new-listing ratio remains significantly above long-term averages and prices continue to increase.

The market has likely been responding to multiple factors underpinning the slowdown. Erosion in affordability, OSFI’s stress test, bidding wars fatigue, lack of supply, and a reversal of pandemic-spurred preferences for more space as mobility restrictions unwind and travel surges are among the possible explanations. Further, some buyers may be adjusting plans to account for higher expected borrowing costs as the Bank of Canada begins to hike rates in response to a recovering economy with strong inflation readings. We still expect the Bank of Canada to increase rates no sooner than 2022H2 and in a gradual and well-communicated manner. However, at today’s higher prices and elevated debt levels, gradual increases over the term of the mortgage will translate to larger monthly payments, making households more vulnerable to rate hikes at renewal. On the other hand, some sellers may be slow in adjusting their expectations to a less-unstable market, turning down generous offers that do not match what their neighbours have received earlier in the peak months of February or March, further dampening transactions.

Aside from erosion in affordability, buyer fatigue has been among the most cited causes for the slowdown in resale activity—after months of unsustainable price increases and stories of vicious bidding wars, it is no surprise that some buyers opted to exit and watch from the sidelines as ownership became less feasible, despite the record-high savings accumulated during the pandemic. Some of the buyers who took a break to enjoy a double-vaccinated summer may have been further increasing savings toward a higher down payment (for some, this meant saving on rent by taking advantage of working from home and moving back in with the parents). After the summer moderation and as life gradually resumes normalcy, it is possible that some of these buyers will feel well-rested and ready to restart their search and put these savings to use. With few signs of direct impacts from the Delta variant on Canada’s economic activity, this pick-up in demand is likely to occur alongside a recovering economy, improved labour conditions and a resumption in immigration.

This means the stabilizing trend over the past few months might reverse. With demand well-supported by fundamentals, activity is expected to pick up again—of course, tempered to an extent by the erosion of affordability for certain households—while the critical supply shortages underlying the market imbalances have not yet been addressed. These persistent demand-supply imbalances continued to push the MLS Home Price Index (HPI) upward. The plethora of election promises geared at solving the housing market problem may fall short of doing so, as most are focused on issues of affordability rather than increasing supply. All major parties have indeed promised to build more houses, but once you net out what is already being built on average every year, the additional promised units will alleviate some of the pressure but are far from sufficient to close the widening supply gap. Much of the solution lies in a collaborative, multi-stakeholder process to comprehensively identify and tackle the obstacles to more responsive supply in all segments of the housing market and at all levels of government (see here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.