- The current situation in Canadian housing markets primarily reflects a chronic insufficiency of home supply that is temporarily exacerbated by pandemic-related impacts linked to record-low mortgage rates and a shift in preferences for housing by type and geography. Past and future macroprudential measures are ineffective band-aids that do not address the underlying insufficiency of supply.

- Canada has the lowest number of housing units per 1,000 residents of any G7 country. The number of housing units per 1,000 Canadians has been falling since 2016 owing to the sharp rise in population growth. An extra 100 thousand dwellings would have been required to keep the ratio of housing units to population stable since 2016—leaving us still well below the G7 average.

- Much more policy focus should be devoted to finding ways to increase the responsiveness of supply to demand. Most approaches to achieve this are politically challenging but must be considered. We propose the urgent creation of a national table composed of federal, provincial, and municipal authorities, along with real-estate developers, investors and civil society organizations to comprehensively identify and tackle the obstacles to more responsive supply in all segments of the housing market. There is unfortunately no easy near-term fix, but the more urgency is attached to the problem, the sooner we will see impacts.

The conditions for robust growth in house prices have been in place well before COVID-19. Heading into the pandemic, the supply of housing simply had not kept up with population growth, pointing to a near-record imbalance between the supply of housing and demand (chart 1). The pandemic caused a shift in preferences for housing facilitated by record-low mortgage rates which only served to increase the demand. In some ways, the reduction in immigration growth observed in 2020 withheld the further increase in demand that would have otherwise occurred. So while it is clear that interest rates and a shift in preferences for housing by type and geography (facilitated by remote-work arrangements) contributed to the strength of the housing market, the fact remains that the principal challenge facing the housing market—and the underlying cause for rising prices and diminished affordability—is the substantial insufficiency of supply relative to demand.

Though housing starts are off to a great start this year, and the rise in new listings is bringing better balance to the resale market in some parts of the country, there remains a need for a far more structured solution to the supply/demand imbalance issue in housing. We know, for instance, that population growth will resume its rapid pace of increase if the government delivers on its very welcome immigration plans. Foreign students will return to Canada and need housing. Travel will resume and owners of temporary accommodations will rent those out. If the government is successful in rolling out a new national childcare system, family incomes will rise, almost certainly increasing the demand for housing. We know these things are coming. We should learn from the mistake of the last few years: we know demand will rise strongly from a needs-based perspective, yet we also know that the supply response is likely to be hindered by a range of obstacles.

There is general agreement on the notion that supply challenges are important. Where there is less clarity is the extent of the supply shortfall, and, of course, how to address that. This note focuses on the former and offers some suggestions on the latter by putting the supply/demand dynamics of recent years in historical and international context. Our conclusion is clear: housing construction has not kept up with demand and, when looking at international comparisons, the shortage of supply is even more sharply evident. This suggests that house prices are likely to trend upward for the foreseeable future given the years it would take to close the gap between supply and demand. Much more policy focus should be devoted to finding ways to increase the responsiveness of supply to demand. We propose the urgent creation of a national table composed of federal, provincial, and municipal authorities, along with real-estate developers, investors and civil society organizations to comprehensively identify and tackle the obstacles to more responsive supply in all segments of the housing market.

Taking a longer-term perspective, we can look at the increase in the Canadian housing stock relative to the increase in population to get a sense of how effective we have been in creating new units. The ratio of new home completions relative to the change in population over a three-year period gives a sense of the dynamic response of housing supply to population. At a national level, this suggests that the supply challenges captured by higher-frequency data are rooted to some extent in chronic constraints over the last few years. The ratio has been well-below its historical average since early 2018. That isn’t a surprise. Canada experienced an immigration-fuelled population boom since 2015 that saw population rise much more rapidly than new housing units were built. This population boom came to an abrupt stop in 2020 owing to COVID and saw the ratio of completions-to-population improve a bit, but that is likely to reverse course if the government manages to increase immigration levels in line with its stated ambition. Prior to the interruption in immigration, the ratio was at the lowest level ever seen.

Beyond historical averages for the information above, there is no clear way to determine what the optimal level of housing might be. There is clearly a supply challenge, but how can we assess its scope? One option is to calculate the level of housing completions that would have kept the ratio of completions to population growth at its historical average. Based on 2020-Q4 data, that suggests an extra 90 thousand homes should have been built over the last 36 months, or alternatively that population should have only increased by about half the amount observed given the number of completed housing units.

The most simple and informative metric in assessing the gap between needs and supply is the ratio of the total number of housing units in Canada relative to population.1 Think of the changes in completions and population over the 36-month period above as the flow measure and total housing units relative to population as the stock equivalent. We can compare this stock data internationally to derive insights on the extent to which the supply situation here stands out from other industrialized countries. To calculate this ratio, we use Census data on the number of dwellings and augment that with yearly home completion and demolition data to get a sense for how recent dynamics compare to history.2 An advantage of this approach is that relative homeownership rates do not matter: housing units are required whether citizens predominantly prefer renting or owning, facilitating international comparisons. Differentials in household size can explain some variance, but household size in Canada (2.4) is quite close to the G7 average (2.3).

These data clearly show that the pace of home construction relative to population has declined since 2016. Nationally, there were 427 housing units per 1,000 Canadians in 2016 with that ratio falling to 424 by 2020. For that ratio to have remained stable, roughly 100 thousand more units would have needed to be built in Canada over that time. The ratio alone only provides directional evidence of the evolution of supply and demand. It does not really help us understand how far off (or not) we are from a better matching of needs versus availability of housing.

The international perspective can be helpful here, particularly since observers like to compare the evolution of Canadian home prices against international comparators. Housing choices vary by country and city, so there is clearly not a one-size-fits-all number of housing units per population. The number of housing units in Canada falls quite a bit short relative to most other countries as is clear from chart 2. Across the G7, the average number of housing units per 1,000 residents is 471. To put our number in perspective, it would take an additional 1.8 million homes in Canada to achieve this level of supply of housing relative to population. Simply catching up to the UK, which has 433 units per thousand citizens, would require roughly an additional 250 thousand homes in Canada. Catching up to the US, we would require another 99 thousand units. To put these gaps in perspective, we have averaged 188 thousand home completions in the last 10 years.

The fact that we are so far below our G7 peers provides some indication of the under-build relative to needs but it should of course not be interpreted as a requirement to build many millions of additional units.

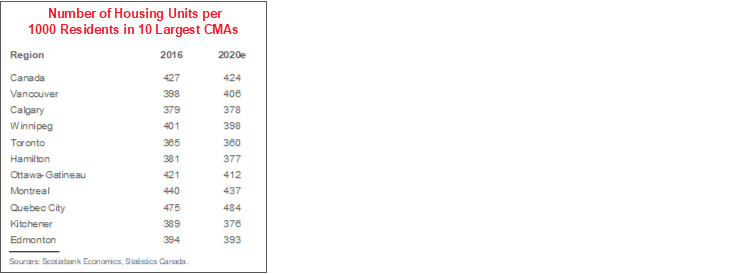

The calculations are more challenging at the provincial or municipal level as there are no data available on the number of units that are torn down to make way for new ones. We approximate demolitions by census metropolitan area (CMA) by scaling national demolition by the number of completions in each CMA. Doing so generally confirms the observations at a national level. Since 2016, the ratio of units to population has declined in almost all of the 10 largest CMAs. Apart from Québec City and Montréal, all CMAs are well-below the national average. Only Québec City and Vancouver have managed to raise the units-to-population ratio since 2016. Recognizing again that there is likely no one-size-fits-all value for the units-to-population ratio owing to a range of factors (local geography, demographics, government policies, size of households, income, share of multi-unit housing, share of owners/renters...) there is nevertheless some indicative value in comparing the data for each CMA to the national average.

The goal of this note is not to quantify the exact housing shortage but rather to document these shortages using a range of approaches. The insufficiency of supply is clear at any horizon. It is not simply a reflection of the currently low borrowing costs and exceptional government support. It reflects a long-standing under-production of housing, whether for rent or purchase. The most likely path forward is for home prices to continue to appreciate until there is a better balance between demand and supply. That doesn’t mean prices will continue to rise at what is clearly an unsustainable pace, but we do believe that prices are more likely to go up, rather than down, over the next several years.

A key challenge is finding an approach that can overcome the political obstacles to a better supply response. Very often within city limits, measures to increase density pit current owners versus prospective residents. Municipal councillors are politically responsive to their voters given the nature of the democratic process. What may be great policy from a national perspective, like high immigration, runs into obstacles when it means finding practical solutions at the local level to increase the housing stock.

We need a truly collaborative, multi-stakeholder process to break through these political challenges to concretely identify the factors limiting the supply response of all forms of housing: owned, rental, affordable, singe-family, and multi-family. The current National Housing Strategy isn’t designed to do this. The macroprudential measures of the last years are mere band-aids. We propose that the Federal Government convene a national table bringing together federal, provincial, and municipal authorities along with builders, developers and civil society organizations to document the multiple challenges to raising supply and identify solutions to these obstacles. Given the lags inherent in the development process and the urgency of the supply challenge, this table should be convened expeditiously and report on potential solutions within the next 6 months with commitments by all parties to immediately act upon those.

To overcome political obstacles, and in a fine Canadian tradition, the solution is almost certain to require additional Federal funding to incent provinces and municipalities. As we’ve argued before, the Federal Government could, for instance, tie future transit funding to density and speed-of-approval objectives. An alternative approach would be for the Federal Government to offer density incentives for cities that responsibly raise population density to a certain threshold, or meet certain benchmarks in the planning and approval process.

To get a sense of the main obstacles to a more elastic supply response, we have polled several of our clients in real estate and development across the country to find the cross-cutting factors they see as most limiting supply growth. To no surprise, the key impediments are in the planning and approval process. In many major cities, the entitlement process is very lengthy and unduly political. Many processes can delay or derail development applications and this can be exacerbated by under-resourced planning departments within cities. From a rental perspective, the structure of requirements to build inclusive housing can put a cap on returns, limiting investor interest. Rent control is a perennial concern. Rising development charges applied to new developments, while intuitively appealing, reduces the returns on new investment relative to existing buildings. In some areas, strict requirements to find accommodations for existing tenants in proximity to their current residence while a new building with more units is being redeveloped limits the ability to increase the number of inclusive units. Property tax abatements for rental units with affordable components could be modelled on markets where the property tax system better incents the development of affordable rentals, such as the Affordable New York program. Going beyond the planning challenges, shortages of skilled trades are increasingly likely to affect builders’ ability to meet demand and they would like to see more support for skills development programs by various levels of government.

Solving our country’s housing challenge should be a national priority. The sustainable solution is not rooted in the interest rate or macroprudential space but rather in a determined effort to remove obstacles that limit housing supply. The analysis herein points to the cumulative impact of these challenges as reflected in the gap that exists between measures of housing supply relative to population. A comprehensive national approach should be pursued to identify changes that could increase the responsiveness of supply to demand with those changes then being implemented aggressively. This will not be an immediate fix, we must learn from our experience of the last few years: with a needs-based increase in demand linked to rising immigration in coming years, we know we cannot afford to keep the system as is. Let’s get serious about solutions and find effective and collaborative approaches to meet this challenge.

1 Housing units are defined by Statistics Canada as dwellings with an individual entrance. 2 Demolitions are only available after 2018. We used the average over the 2018 to 2021 period to estimate demolitions for 2017.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.