FURTHER REOPENING SENDS HOME SALES INTO THE STRATOSPHERE

SUMMARY

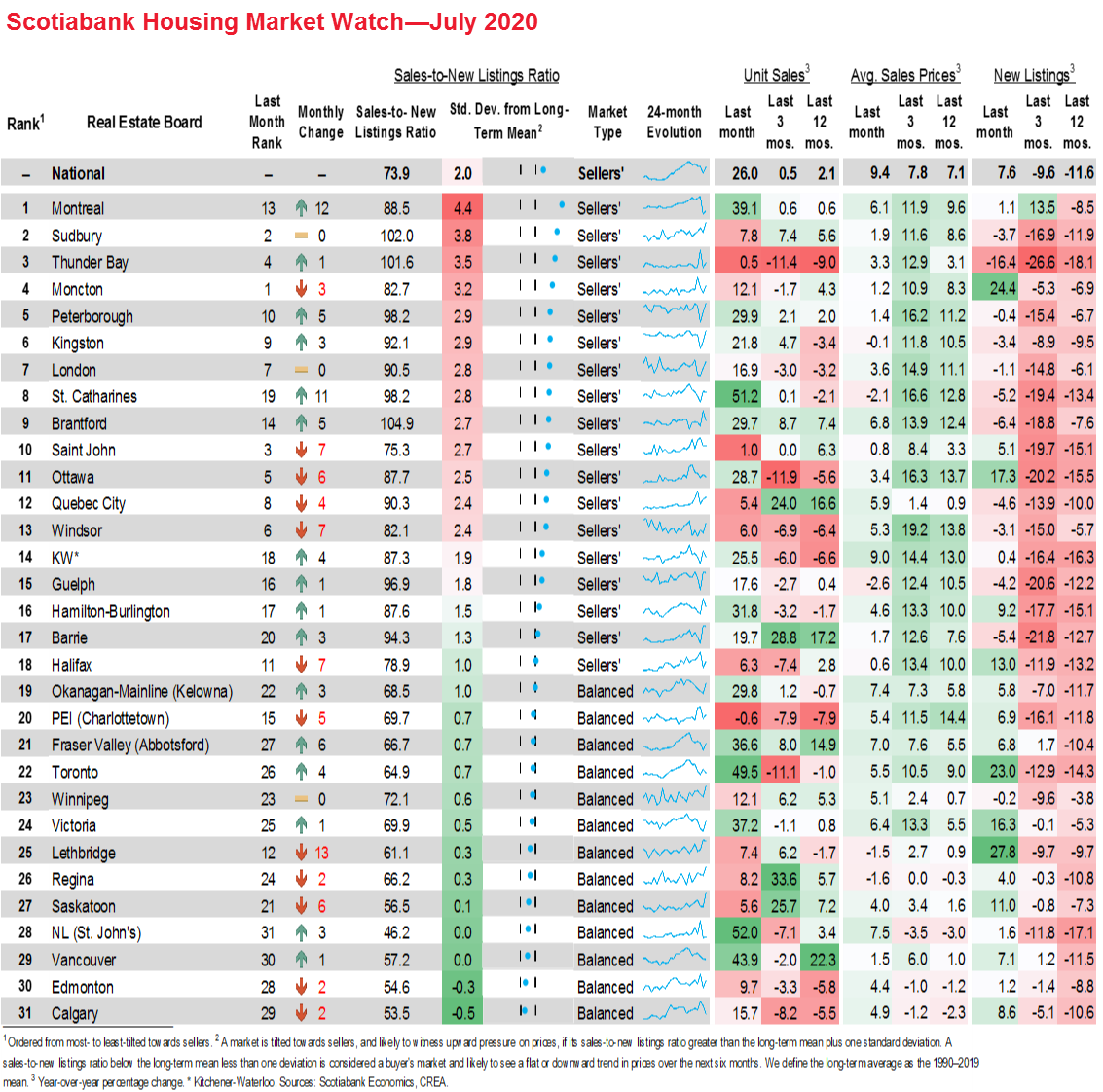

Home sales activity surged again in another sign of Canada’s buoyant ongoing rebound from COVID-19 lockdowns. With re-openings continuing across the country, new listings registered their strongest-ever month of July in 2020, while existing home sales reached their highest level in any month in recorded history. On a m/m seasonally adjusted basis, Canadian home purchases rose by 26%, while new listings climbed by a healthy 7.6%. That pushed the national sales-to-new-listings ratio to 73.9% (sa)—the highest since 2002 and consistent with demand-supply conditions strongly tilted in favour of sellers. Consequently, the composite MLS Home Price Index (HPI) rose by 7.4% (nsa y/y)—the strongest gain since 2017.

Canada’s largest centres tended to witness the steepest sales increases. Purchase volumes were up by more than 40% in both Toronto and Vancouver, with Montreal registering a 39% advance (all sa m/m). Ottawa, a number of cities in Southern BC, and Ontario’s Greater Golden Horseshoe (GGH) region also enjoyed strong sales gains. Purchases were up across municipalities in Saskatchewan and Alberta as well, albeit at a more moderate pace.

In July, 18 of the 31 centres for which we maintain data posted sales-to-new-listings ratios consistent with sellers’ market territory. While new listings in many centres have recovered to above pre-lockdown levels, 14 of the 18 centres in sellers’ market territory have yet to return to February levels.

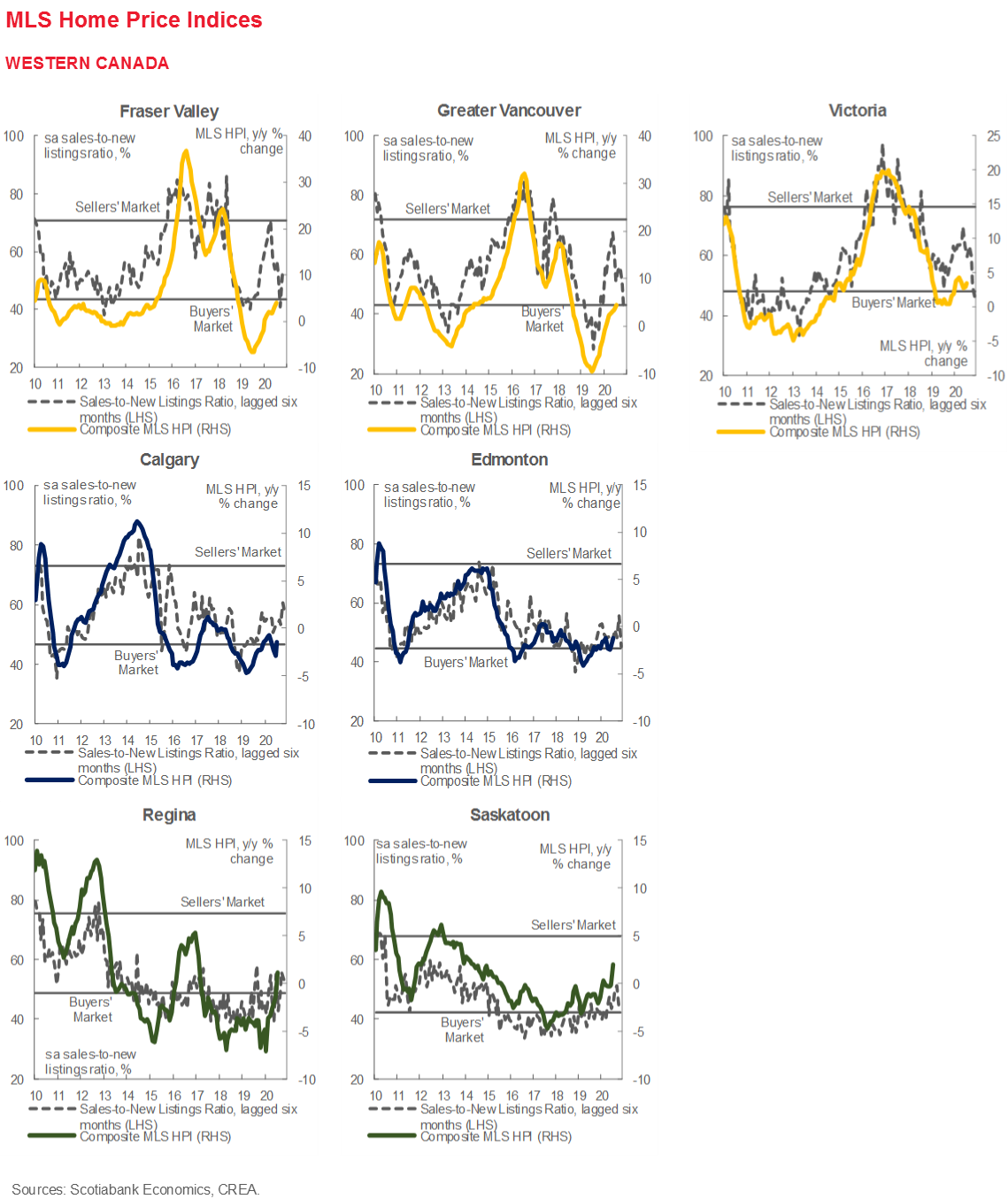

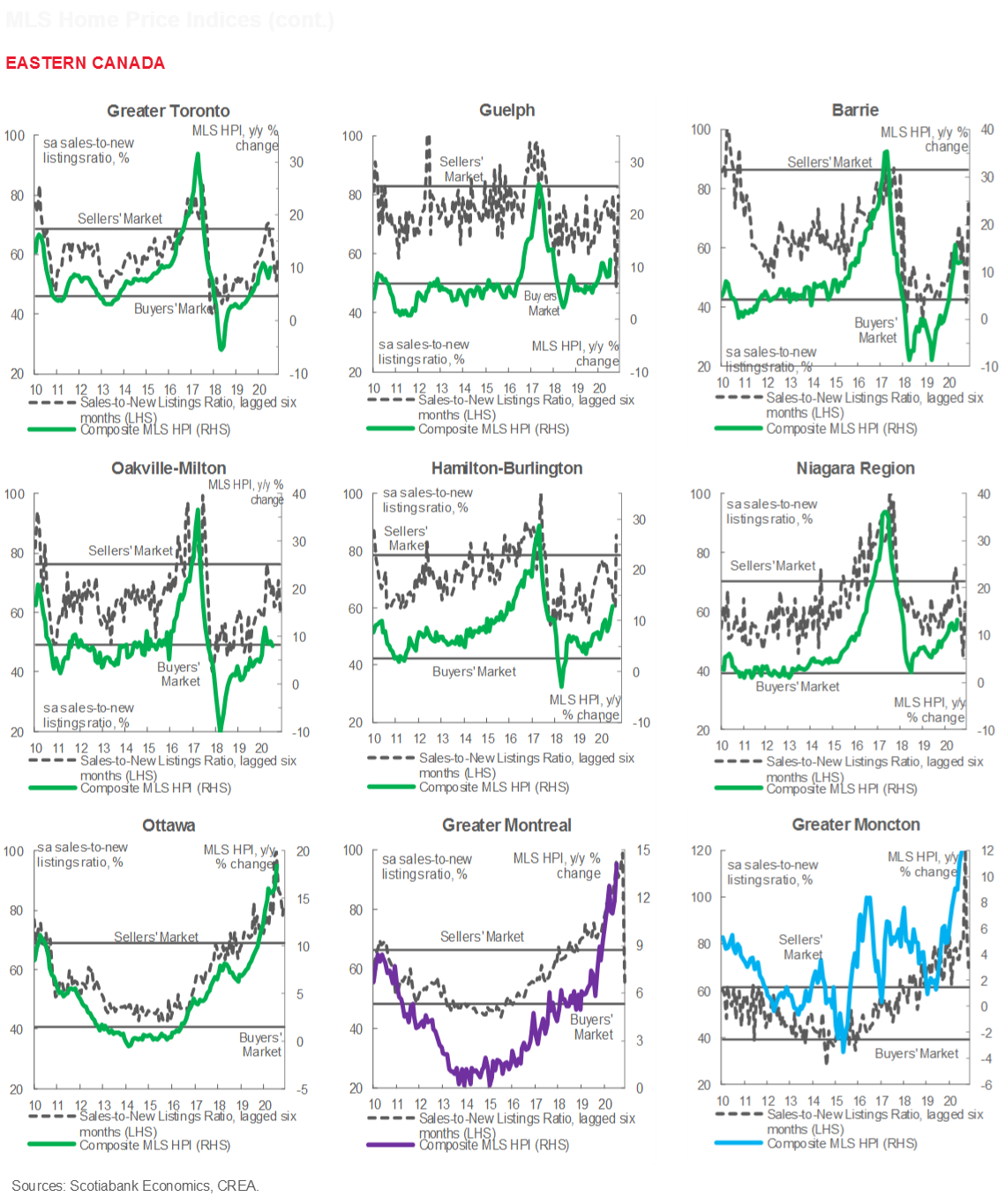

MLS HPI gains were positive in most centres, especially in larger metropolitan areas which had remained in stricter phases of lockdown for longer periods of time. Most cities in the GGH maintained price growth of more than 10% y/y, while Southern BC municipalities witnessed some of the strongest gains in nearly two years. Ottawa (+18% y/y), Montreal (+14% y/y), and Moncton (+12% y/y) posted record growth in home prices despite the recovery of new listings to pre-lockdown levels.

IMPLICATIONS

Solid gains were expected as most regions entered the final stage of reopening in July and following early releases from local real estate boards, but the strength of the rebound continues to surprise. Nationally, both unit sales and new listings have surpassed pre-virus levels, with purchases now a hefty 17% higher than five months ago. That strength, coincident with a labour market yet to return to its pre-pandemic vibrancy, suggests some pent-up demand remains that could continue to be released in the coming months, even as the pace of reopening eases. The effects of more stringent mortgage borrowing conditions introduced by the CMHC on July 1st may eventually dampen mortgage demand, though there is little evidence of that to date.

New listings’ slower pace of recovery versus home sales is a trend worth monitoring in the coming months. Should it persist over future periods, further upward pressure on house prices can reasonably be anticipated.

The strength of the ongoing rebound notwithstanding, potential downsides to the outlook identified earlier remain very much at play. These include a second wave of the virus, persistent weakness in population growth, and risks related to timing the withdrawal of mortgage and tax payment deferrals. All of these factors could undermine continued gains in the housing market as well as the recovery in the broader Canadian economy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.