- The outlook for growth in most economies remains very favourable with only minor adjustments to forecasts in key economies.

- Supply chain bottlenecks appear more pervasive and persistent, leading to upward revisions to inflation in many countries. While clear evidence of bottlenecks exists, the distinction between supply-related challenges and strong demand is increasingly blurry in some sectors. This is particularly true for housing and labour shortages.

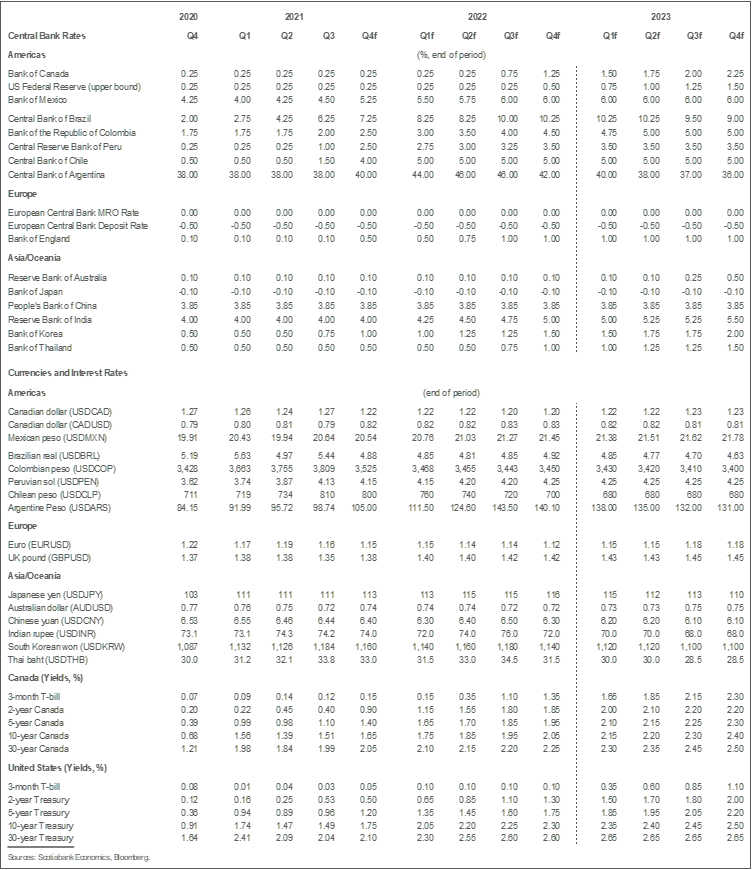

- Given the greater persistence of these supply challenges and our view that these are being compounded by strong demand, central banks will need to respond. The United Kingdom is likely to be the next to move in November, but we are also raising our path for the Bank of Canada, as we now expect 100 basis points of tightening in the second half of 2022 and a further 100 basis points in 2023. The Fed, as long expected, will begin its tapering process shortly, but is likely to hold off on rate increases until late 2022.

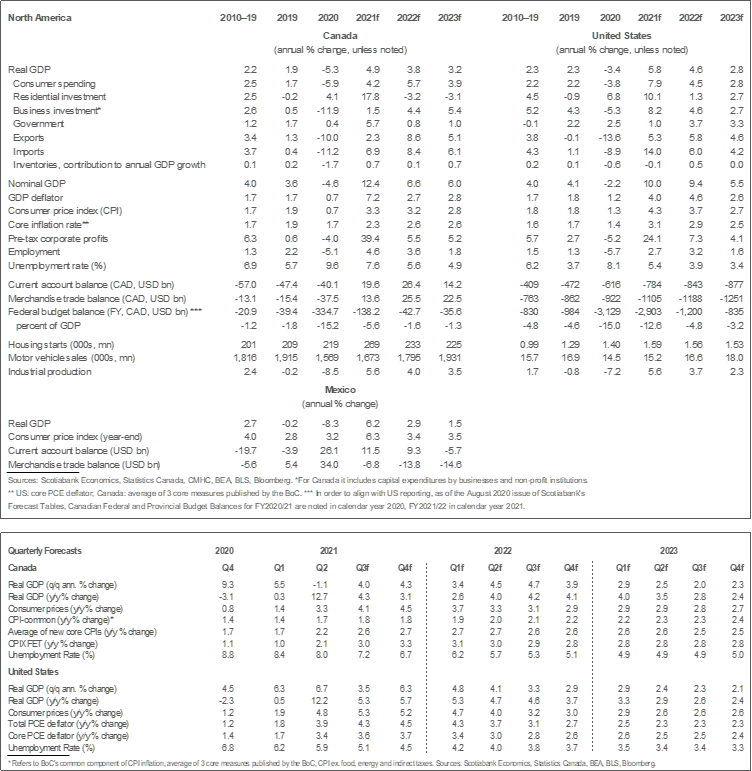

It is now clear that supply bottlenecks are broader and longer lasting than earlier assessed. We had marked-down our forecast for Canadian growth in our September forecasts to reflect this, but it now appears clear that in Canada and elsewhere, the inflationary consequences of these supply bottlenecks have been underestimated. As a consequence, we are revising the inflation outlook in our key markets despite a relatively unchanged growth outlook to account for the greater persistence of the imbalance between global demand and the production apparatus. Central banks in some countries have already responded to the impact on inflation (New Zealand and the Pacific Alliance Countries have increased policy rates, Canada is tapering asset purchases), others have made it clear they will act in the near-term (the United Kingdom), and others have revised their guidance on the withdrawal of stimulus (the United States).

We still view the supply disruptions as temporary, but they are clearly more persistent. A number of important, and less important, components in the global supply chain are in short supply. These range from complex things like semiconductors to raw materials like zinc. In some countries, low inventories of natural gas are leading to much higher energy costs for firms and households. Disruptions such as these are clearly temporary, but they speak to the broader issue of supply challenges catching economies off guard. There is some early evidence that some of the shipping constraints on the US West Coast are easing and, while the cost of shipping commodities remains very high, it is well off the peaks seen earlier this month. Nevertheless, it will take many months of additional improvement in these and other metrics to ease the supply crunch.

Muddying the inflation outlook further is an increasingly blurry distinction between supply-related challenges and those posed by strong demand. Even if ocean shipping costs were to normalize, there is a shortage of transportation and warehouse workers to handle the volume of goods being shipped within and across countries. The truck driver shortage pre-dates the pandemic. In Canada and the US, there are already acute labour shortages. Some of these partly reflect frictions associated with workers leaving one sector to join another, while in the US the labour force participation rate remains well below pre-pandemic levels, suggesting a number of disengaged or discouraged workers. While the participation rate is back to pre-pandemic levels in Canada, labour shortages are acute according to survey and Statistics Canada data. On balance, labour market dynamics appear to reflect strong demand for workers far more than individuals opting not to work or skills mismatches.

The lengthier supply crunch and this ambiguity of supply vs demand impact in some segments of the production chain are leading us to revise upwards our inflation forecast in Canada. On the labour side, we expect compensation per hour to rise by over 4% in each of the next two years. This reflects the unusual dynamics of the current situation: record labour shortages in the early phases of what we still anticipate will be a strong and lasting recovery. Moreover, home prices and rents should continue to rise given the underlying supply-demand imbalance tensions in the real estate market. So even as some of the temporary supply-chain-induced increases in prices mute over the coming months, other sources of fundamentals-driven inflation will amplify. As a consequence, we now expect Canadian core inflation to average 2.6% in 2022 and 2023.

As a result of this revised inflation profile, we now believe the Bank of Canada will raise interest rates by 100 basis points in the second half of 2022, to 1.25%. That’s 50 basis points more than we have carried in our forecast for a few quarters now. We are also marginally adjusting our end 2023 forecast to 2.25% from 2.0%. If inflation rises more rapidly than we expect, we may need to forecast an earlier tightening along with a potentially higher 2023 endpoint.

We are tracking a number of risks that could impact our forecast. There are clearly several risks associated with developments on the supply side of the economy. A more rapid unwind would lessen inflationary pressures and boost growth, while the opposite would occur if the disruptions were to worsen. The potential for significantly stronger wage acceleration than forecast should not be discounted, with obvious impacts on inflation and interest rates if that were to happen. The rise of global energy prices is a clear headwind to energy-importing economies, but is also a tailwind to Canada, though in both cases inflationary consequences could be significant. Further increases in these prices would have a meaningful impact on the global outlook for growth, inflation, and interest rates.

Though we have only incorporated a modest amount of additional fiscal expenditures in the US, a collapse of the infrastructure package talks would lead us to scale our US growth forecast down. On the other hand, an agreement on a broader set of packages could provide a boost to our forecast over the next couple of years. Finally, the impact of deliberate production curtailment in China is leading to lower growth there with modest impacts, so far, on the rest of the world. There is potential for these reductions in production further damage supply chains with clear impacts on growth and inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.