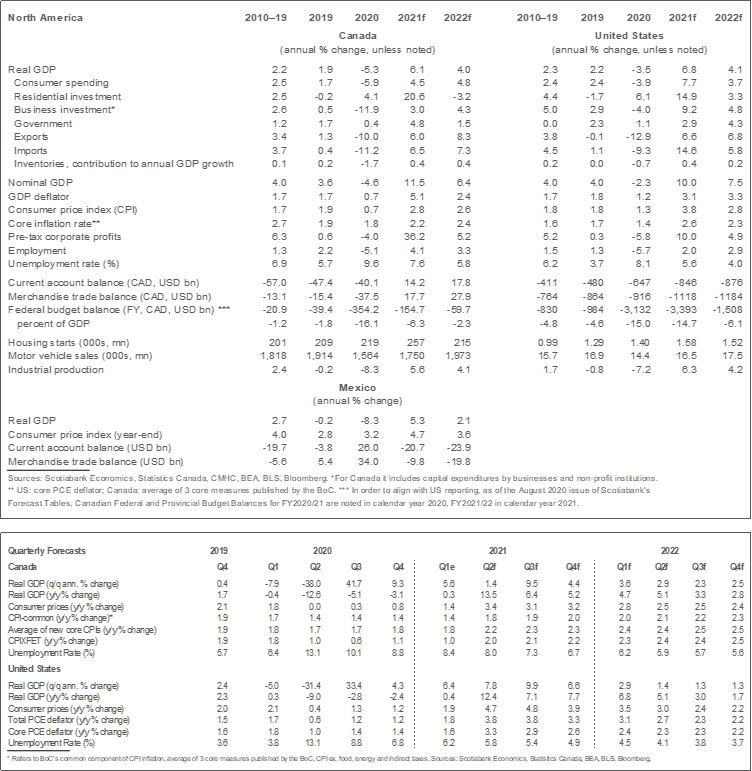

- No major changes to the outlook for Canada and the United States. Exceptionally strong recovery still expected this year and next.

- Supply challenges are temporarily pushing inflation above central bank targets and are increasingly difficult for firms to manage. We think supply will gradually rise to meet demand as the summer progresses, but it may be possible that shortages of goods and materials act as a brake on growth in the interim.

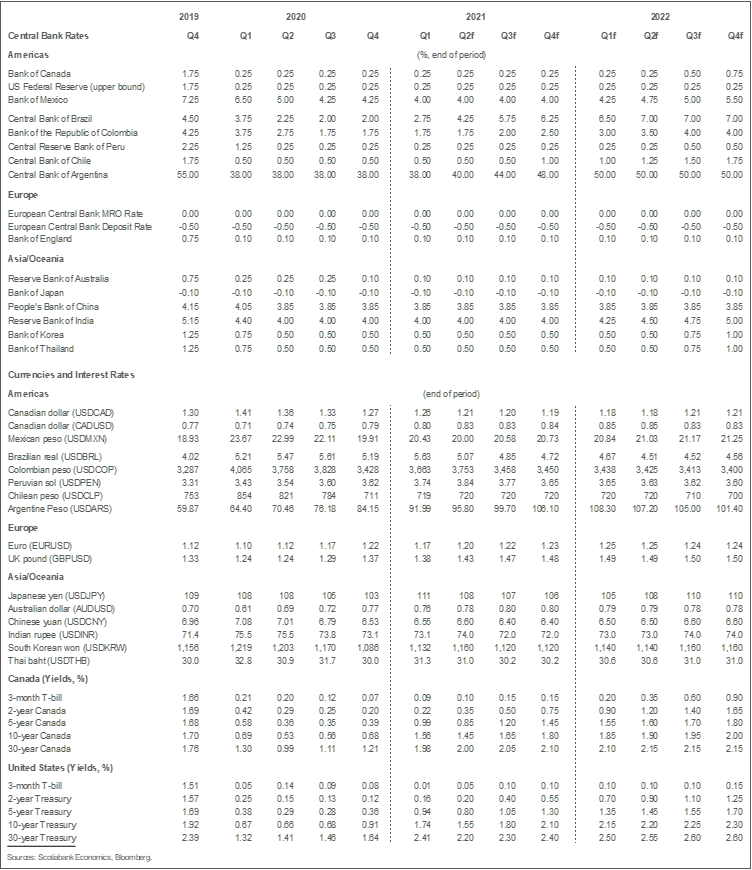

- Our rate calls remain unchanged: The Bank of Canada is forecast to raise its policy rate in 2022-Q3, and the Federal Reserve will likely begin tapering in January 2022 before raising interest rates in 2023-Q2.

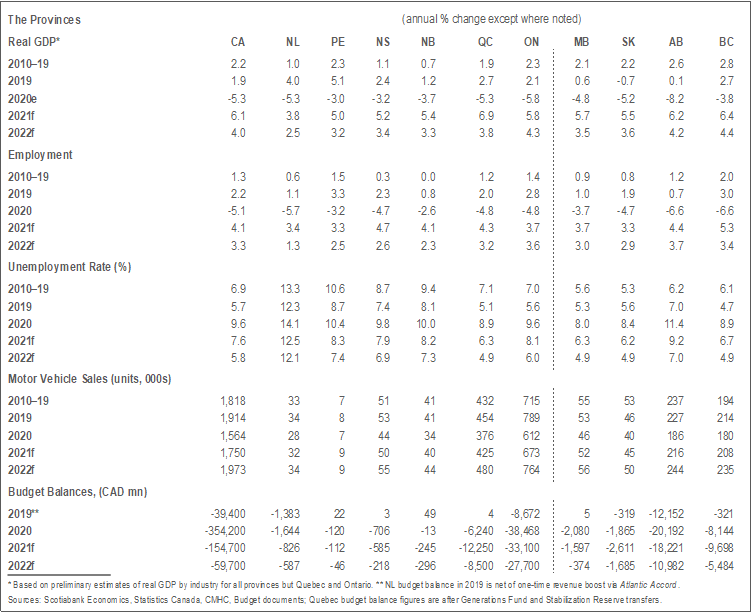

There are no material changes to our US and Canada outlook this month. Economic indicators continue to suggest a strong rebound is underway, though Canadian data are muddied by the impact of COVID restrictions in April and May. In the Canadian context, solid progress on the vaccination front and sharp reductions in new infections have led many provinces to announce gradual re-opening plans which suggest that much of the economy will be re-opened by the end of the summer. This should allow a forceful rebound in the sectors that continue to be deeply affected by COVID. This is all contingent, of course, on continued progress in the fight against the virus.

There are three big uncertainties facing the forecast for Canada and the US. How temporary will the current overshoot of inflation be? Associated with that question, will supply rebound fast enough to facilitate the growth in demand we anticipate? Finally, how quickly will labour markets improve?

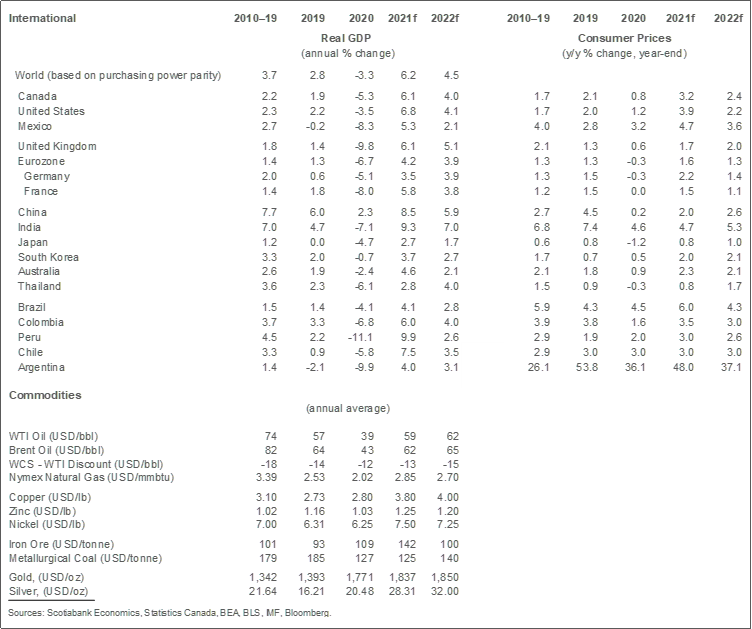

On inflation, the most recent inflation readings in Canada and the US clearly point to an acceleration in inflation that exceeds inflation targets. We view these exceptional pricing pressures as temporary, as do the Bank of Canada and the Federal Reserve, but believe inflation will slow yet remain sustainably above targets once these impacts pass and output gaps move into excess demand (expected at the end of this year in Canada). In the meantime, shortages of inputs and the consequent increase in their prices are leading to a rapid adjustment in consumer prices. In the US, these price pressures are exacerbated by a high number of job vacancies that are putting upward pressure on wages.

There is not yet compelling evidence that supply challenges are abating. In Canada, for example, the economy-wide inventory-to-sales ratio is at the lowest level since 2014. In relation to sales, retail inventories are at their lowest level ever. In the US, a record share of firms are indicating that backlogs of orders are rising and that customer inventories are too low. And of course, commodity prices continue to suggest that demand exceeds supply in some sectors. We remain comfortable with our view that supply will increase enough to attenuate the temporary and substantial overshoot of inflation targets, but this appears to be a riskier call the more data we get.

In Canada, labour markets remain deeply affected by the pandemic and associated mobility restrictions. In May, employment was 3% below pre-pandemic levels, as the third wave resulted in a deterioration from the March result, which had pointed to employment being only 1.5% below pre-pandemic levels. The weakness in employment is concentrated in certain industries and types of workers, but we anticipate that employment will rebound strongly in months to come as mobility restrictions are lifted. That is certainly the pattern observed in the previous waves. In the US, nonfarm employment remains stuck at about 5% below pre-pandemic levels despite a record rate of job openings.

There remains a sharp divergence between employment and inflation outcomes in Canada and the US, complicating the task of the Bank of Canada and the Fed. This is particularly so in the US considering the relative underperformance of employment. In view of our growth outlook, we anticipate that labour market outcomes will improve substantially as the year progresses, even as wage growth picks up. Given that, and our forecast that core measures of Canadian inflation will be sustainably at 2% by the third quarter of this year, we still expect the Bank of Canada will raise interest rates in 2022-Q3. The Federal Reserve is forecast to raise interest rates in 2023-Q2 given the lagged employment recovery relative to Canada, but we expect it will begin tapering asset purchases next January. At this point, the upside surprise to inflation suggests that risks to the rate calls appear skewed to the upside, both in terms of timing of the initial move but also the speed at which rates will rise when they do move.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.