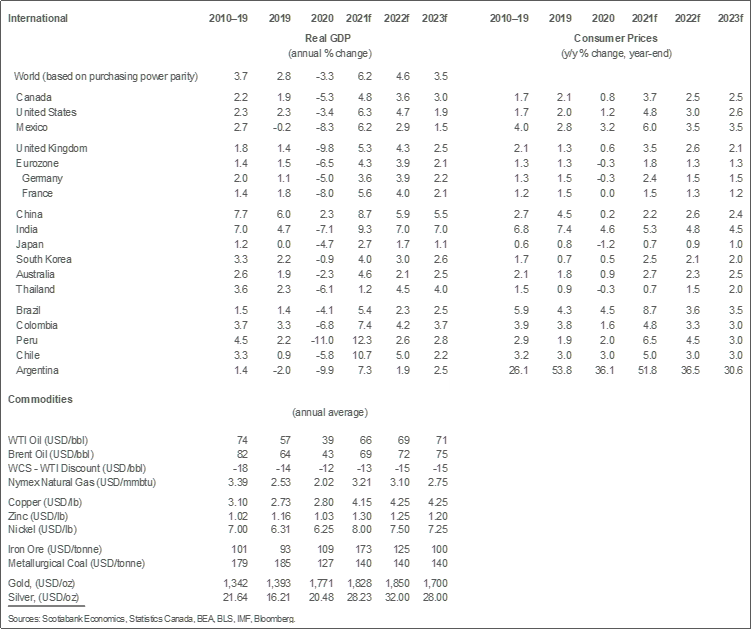

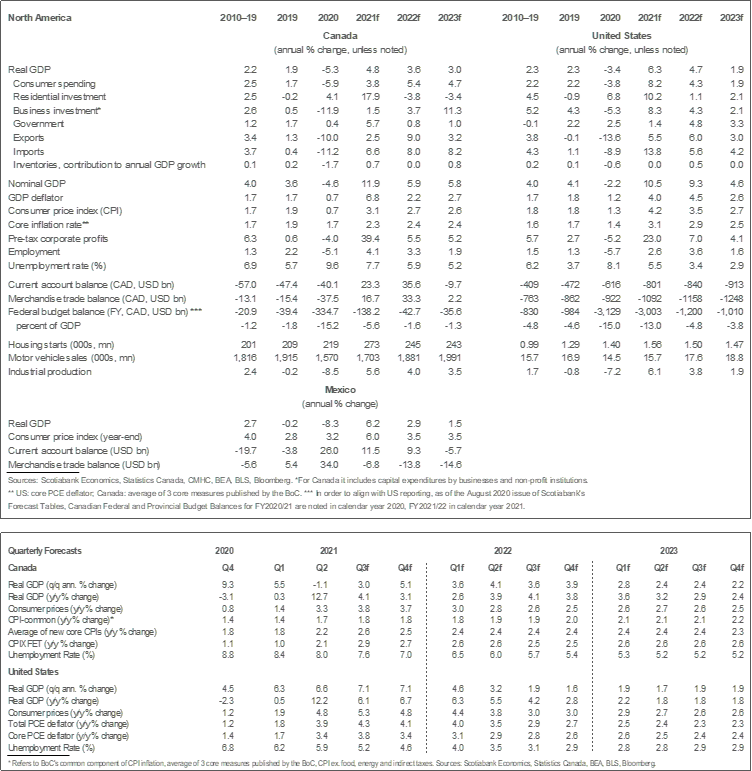

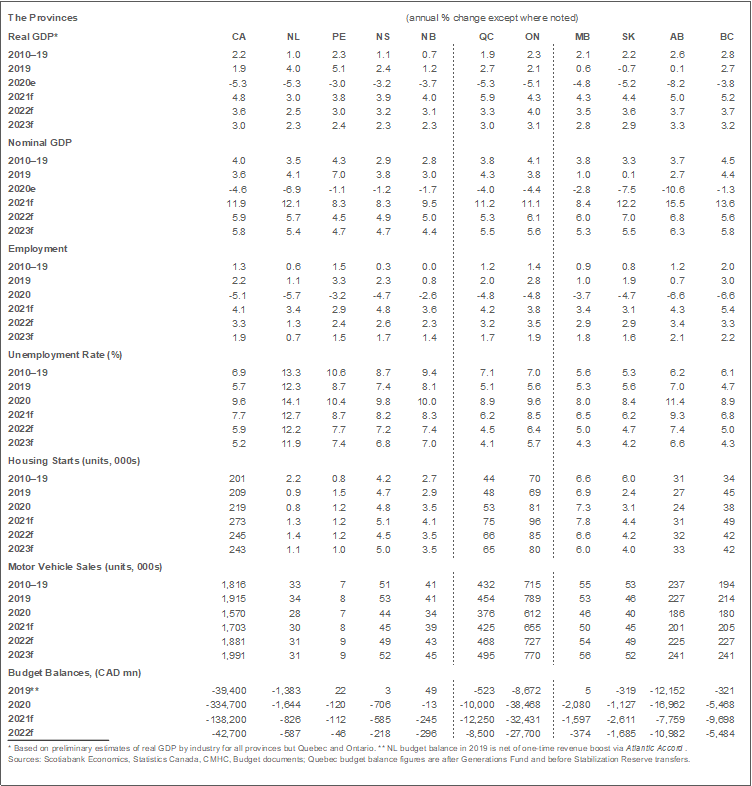

- Growth in Canada revised to a still-strong 4.8% in 2021 from 6.1% in our previous forecast. Growth of 3.6% is now expected in 2022, down from 4.1% in our previous forecast. Our first cut at a 2023 forecast points to growth in the 3% range.

- Challenges along the supply chain account for the majority of these revisions as demand remains extremely well-supported by fundamentals. We have revised our estimate of potential output this year and next to reflect longer-lasting impacts from these supply challenges.

- The Delta variant is contributing to some of these production chain issues, notably in the production of semiconductors in some Asian countries. There is relatively little evidence to date that Delta is impacting consumer activity beyond the inability to purchase some goods owing to low inventories.

- With mobility restrictions unwound through the summer in Canada, activity in the COVID-affected sectors is rebounding, helping to offset some of the weakness associated with low inventories of goods.

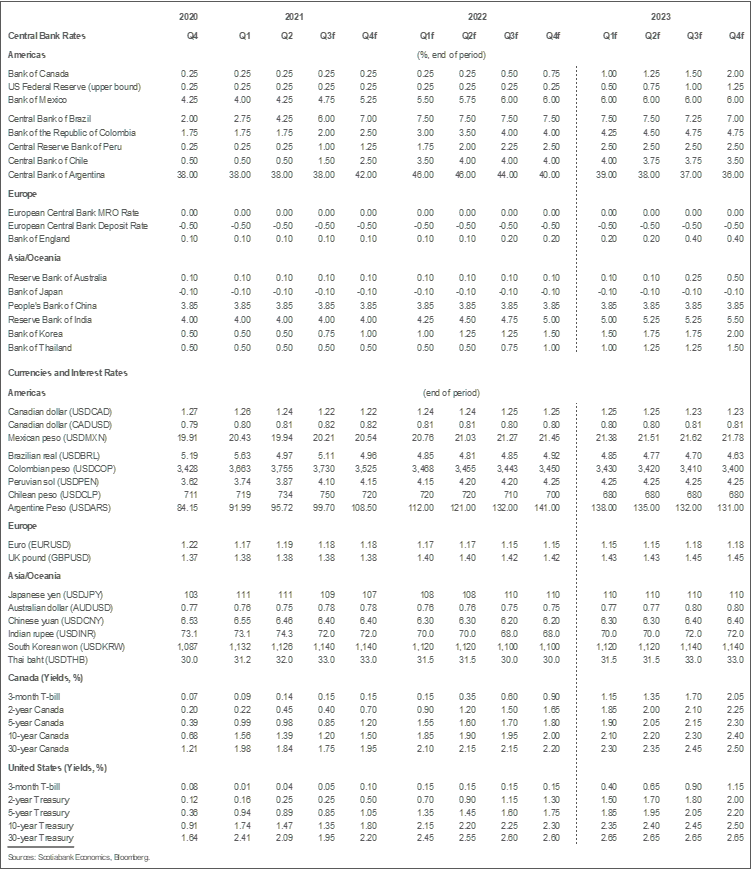

- Inflation pressures remain strong, with a number of central banks already moving aggressively to contain inflationary pressures. We continue to expect that the Bank of Canada will raise its policy rate next summer and that the Federal Reserve will raise rates in early 2023.

- We do not think the electoral outcome in Canada will have a noticeable impact on economic activity next year.

A big revision to the Canadian outlook is in order owing to supply chain constraints that appear longer-lasting and more binding than previously assessed. We now anticipate growth of 4.8% in 2021 (6.1% previously) and 3.6% in 2022 (4.1% previously). The majority of these changes reflect negative revisions to second quarter growth, which largely reflected challenges in obtaining key production inputs either because of component shortages, such as semiconductor chips, or transportation bottlenecks. Despite these frictions, there is plenty of evidence that demand remains robust, that pent-up demand is rising, and the recovery remains on a solid track barring any additional supply disruptions. We currently see few direct signs of economic impacts from the Delta variant on Canadian economic activity and expect that to largely remain the case through the remainder of the year, but it is clear that the virus is impacting key countries involved in the production of critical inputs and that will delay the speed at which the economy can recover.

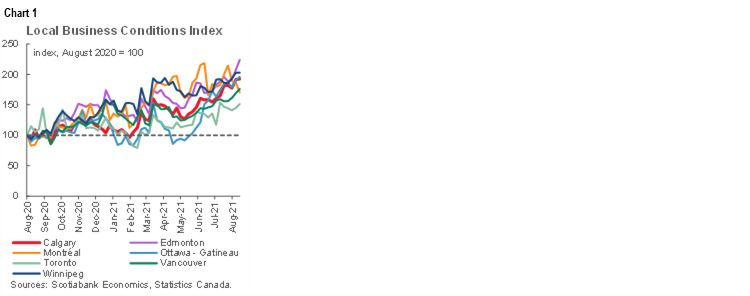

The supply constraints bite precisely because demand is so strong. Employment growth remains exceptionally strong in Canada, household wealth is still at record levels, commodity prices remain high, US growth remains very strong, savings continue to accumulate, and business confidence remains particularly strong even as COVID-19 cases have been on the rise again. Taken together, these fundamental drivers of growth continue to point to remarkably strong growth in coming quarters even if the economy’s ability to import or produce goods is temporarily impaired. Helping offset some of the challenges on the goods side of the economy, the service industry is picking up steam, as mobility restrictions have been unwound. Travel is surging, as is activity in the food and accommodation sector. Bank transaction data appear to confirm this, suggesting consumer spending remained strong in August. Moreover, Statistics Canada now publishes an experimental real-time measure of business activity in major cities (chart 1) which suggests that economic activity in the largest urban centres generally accelerated through the summer.

This tension between demand and supply is evident in a number of metrics, none illustrate this more clearly than survey information from the Canadian Federation of Independent Business’s monthly Business Barometer (chart 2). With job vacancies now above pre-pandemic levels, SMEs report that the impact of labour shortages is the most damaging to sales and production since the survey began. Shortage of inputs and challenges in distributing products are also at their highest recorded level.

These obstacles along the supply chain are observed elsewhere, including the US. It is having particularly strong impacts in industries with large and complex supply chains such as the auto sector. Many global automakers have announced production reductions or shutdowns in coming weeks owing to an inability to secure key semiconductors. Given the sector’s importance to the North American economy, this had a noticeable impact on Mexico, the US and Canada in August and likely September. More generally, the mounting evidence of supply chain challenges has led us to reduce our estimate of potential growth in Canada this year and next.

It is important to put these supply challenges in context. They exist to a large extent because of the strength of demand. For a broad range of goods, low inventories are leading to pent-up demand. Given the strong financial position of many households and still extremely accommodative financing rates, robust consumer spending will follow as more goods become available. This underlies our view that Canadian growth will remain quite strong, at 3%, in 2023.

In the meantime, the imbalance between demand and supply is leading to wide-spread increases in inflation as firms pass along some of the input price pressures they are subject to, including higher wages. Headline inflation is accelerating more rapidly than anticipated in most countries we monitor. We remain of the view that the inflation spike will be transitory, but it is now clear that it will take a few quarters for inflation to be purged of these temporary, but persistent, input price pressures. In Canada, we have maintained our inflation outlook roughly unchanged as the significant negative revisions to our growth forecasts incorporate an adjustment to the rate of potential output growth. In both Canada and the US, we continue to anticipate that core inflation measures will remain above central bank targets through 2023.

Central banks are reacting to these inflation pressures. In the Pacific Alliance countries, input price pressures combined with exchange rate depreciations have led to inflation surges that are already met by aggressive increases in policy rates. In Canada, the Bank of Canada has begun the tapering process and seems unfazed by the surprising weakness in second quarter output. The Federal Reserve appears to be setting the stage for a reduction to their quantitative easing program before year-end. As a result, we remain confident that the Bank of Canada will raise its policy rate next summer despite the mark-down to our growth forecasts. The Fed should follow in early 2023.

The Federal election in Canada is largely a non-event from a macroeconomic perspective. The two leading parties’ economic platforms suggest a largely stay-the-course approach for the next year or two in relation to the magnitude of spending, though platforms differ on what things might be done.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.