SPENDING NOW AND CHARTING A COURSE TO LONG-RUN RECOVERY

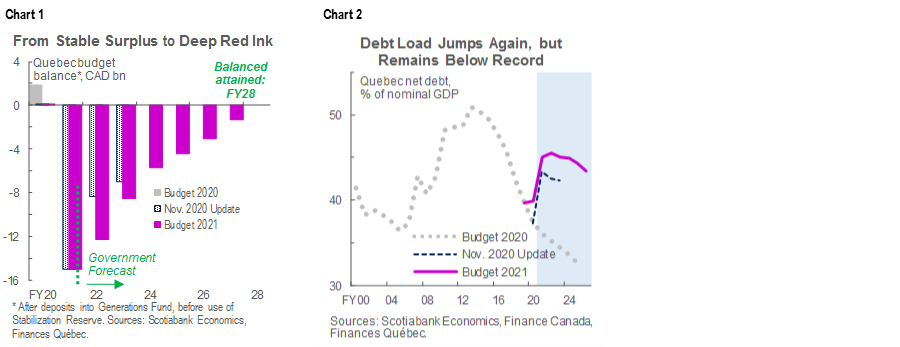

Budget balance forecasts: -$15 bn (-3.4% of nominal GDP) in FY2020–21 (FY21), -$12.3 bn (-2.6%) in FY22, -$8.5 bn (-1.7%) in FY23 before use of the Stabilization Reserve; return to balance targeted for FY28 (chart 1).

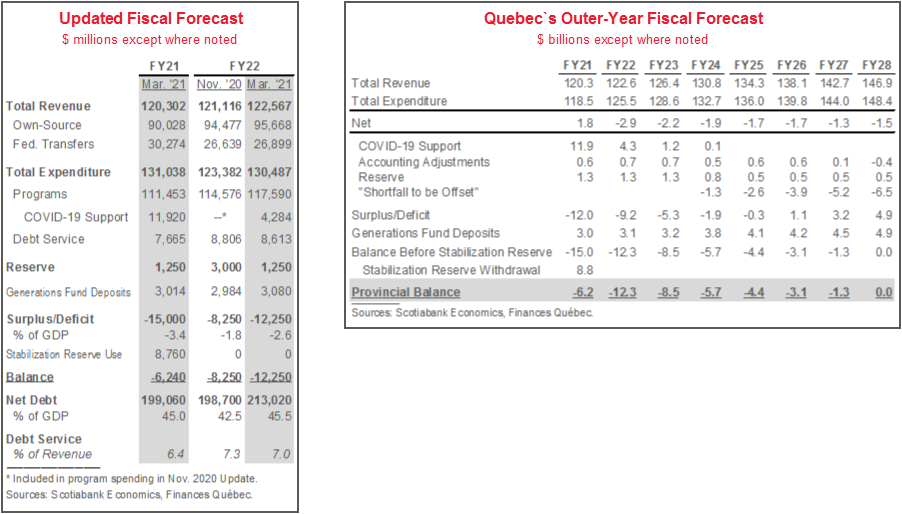

Net debt: expected to peak at 45.5% of nominal GDP in FY22, then ease to 43.4% by FY26—a higher trajectory than forecast in Budget 2020 and the November 2020 Fiscal Update (chart 2).

GDP growth forecast: +4.2% this year, +4% next year, which puts the provincial economy on track to reach to its pre-pandemic, 2019 annual average in 2022.

Financing program: $38.4 bn in FY21, $28.5 bn in FY22, averages $31.3 bn per year from FY23 to FY26.

Budget looks to be a prudent and flexible plan that leaves room for upside and positions Quebec well for a strong recovery from COVID-19.

OUR TAKE

We begin by emphasizing—as we have with all other Canadian jurisdictions we cover—that the COVID-19 pandemic has significantly deteriorated Quebec’s finances. Before the virus reached Canadian shores, the province was in an enviable position with stable surpluses and a steadily declining debt-to-GDP ratio for the foreseeable future, having cut the latter indicator in seven consecutive years. It now anticipates a record FY21 budget deficit—though that was in line with prior guidance—a debt-to-output share 7–8 ppts higher than before the pandemic throughout the planning horizon, and a return to balance in FY28.

Budget increases FY22 spending plans by about $7 bn versus November, largely to address challenges related to COVID-19 and bolster the economic recovery. Measures to strengthen health care delivery include: wage bumps for essential health workers, funds for personal protective equipment and vaccine rollout, planned hiring increases, and another plea for greater Canada Health Transfer payments. It will also offer financial supports for students and temporarily eliminate debt on student loans. Economic initiatives include providing high-speed internet to all of Quebec, tax credits for the adoption of digitization technologies, strategic sectoral supports—including for tourism—and efforts to better integrate skilled immigrants. All appear conducive to boosting growth and productivity.

Federal transfer payments play an important role in early and outer years of the fiscal plan. For one, the end of one-time revenues related to the pandemic supports from Ottawa is expected to contribute to an 11% decline in transfers in FY22. Quebec also expects that a strong economic performance relative to most of the rest of Canada will result in its share of the federal Equalization envelope falling from 64% in FY21 to 53% in FY26. As such, it anticipates that Equalization payments will decline in both FY22 and FY23. Ottawa’s one-time, $7 bn transfer to cover the costs of health care delivery and infrastructure projects—announced today—may help ease the expected pace of decline.

The plan continues to build in prudence, which leaves some near-term upside for budget balances. Budget assumes economic growth below the private-sector mean. Our March 2021 Provincial Outlook assumed that Quebec’s economy will be a top performer in 2021, aided by the arithmetic of its deeper-than-average H1-2020 drop and stronger-than-average rebound since (chart 3). According to Budget, every 1 ppt in nominal GDP growth is associated with $800 mn in own-source revenues; by that figure, our latest 2021 forecast of over 9% growth in Quebec nominal GDP would coincide with more than $2 bn in additional government receipts in FY22. Forecast reserves of $1.3 bn—less than in the November 2020 Update but still meaningful—are included in each year through FY23.

We approve of the planned increase in infrastructure outlays to reinforce the economic recovery. The province had already announced plans to accelerate and step up public capital spending, but we now know the magnitude of those changes. Investment activity is now expected to peak in FY24, but at $16.5 bn rather than the pre-pandemic maximum of $13 bn. Schools, seniors' homes, hospitals, and road and public transit infrastructure will be prioritized, and the province now expects nearly 60% of planned outlays to occur in the next five years. FY22–25 capital outlay forecasts were raised by a cumulative $12.5 bn versus last year’s Budget (chart 4, p.3)

Quebec’s framework for a return to balance appears to contain a good mix of commitment to long-run balance and flexibility on how to get there. The province has identified a $6.5 bn long-term fiscal “shortfall” associated with the spending and economic hit related to COVID-19, which it intends to eliminate over time. It therefore includes an additive $1.3 bn in “shortfall to be offset”—essentially a deficit reduction to be determined at a later date—in each of the five years from FY24 to FY28. This looks appropriate so long as it keeps short-term focus on combatting the pandemic, then targets surplus without limiting the province to any one mode of consolidation. FY28 is the target for balance after deposits in the Generations Fund—Quebec’s sinking fund—and contingencies; before those transfers, surplus is set for FY25.

Other key fiscal indicators have clearly been impacted by the pandemic over the longer-run, but remain on broadly sustainable trajectories. Despite the jump penciled in for FY22–23, Quebec’s net debt-to-GDP ratio is on pace to and decline thereafter and remain below the record levels reached in the early 2010s. Moreover, debt servicing costs are expected to remain at a stable 6–7% share of total revenues—before the “shortfall”—below historical norms.

Quebec’s financing program is estimated at $38.4 bn in FY21, $28.5 bn in FY22, and expected to average $31.3 bn per year from FY23 to FY26. To date in FY21, 32% of borrowing has been conducted on foreign markets; that figure was roughly evenly split between US dollars and Euros. While the 32% share is higher than the mean 21% in the prior decade, but the government noted that it had cushioned against exchange rate effects by keeping no debt exposure to foreign currencies. About three-quarters of borrowings had a maturity of 10 years or more, with an average FY21 maturity of 14 years. The province intends to continue to issue Green Bonds on a regular basis, having already issued five times for a total of $2.8 bn since the inception of its program.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.