PRUDENT PLAN KICKS OFF LONG JOURNEY TO RECOVERY

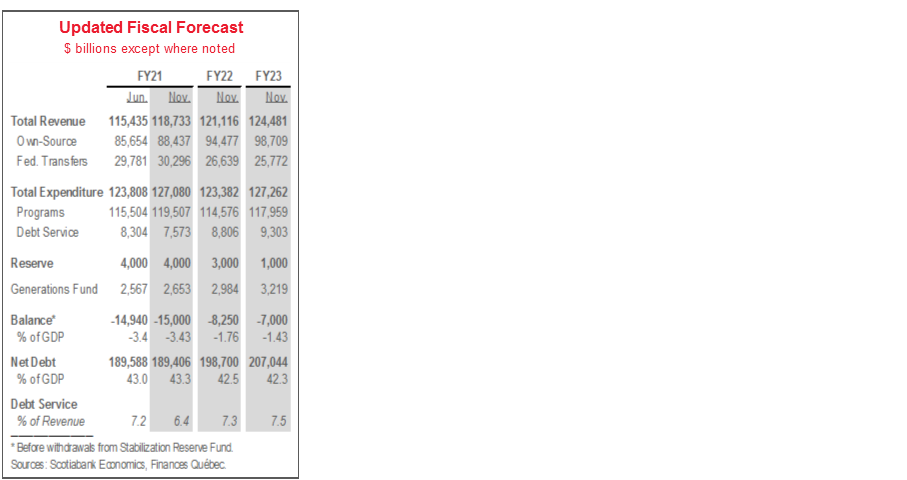

Quebec’s first multi-year fiscal update since COVID-19’s arrival projects deficits of $15 bn (3.5% of nominal GDP) in FY21, $8.3 bn (1.8%) in FY22, and $7 bn (1.4%) in FY23.

A specific date for a return to balance was not provided, but the Province will target a declining net debt-to GDP ratio—now expected to fall from 43.3% in FY21 to 42.3% in FY23.

In line with new deficit spending, total borrowing of $35.3 bn and $31.8 bn are forecast for FY22 and FY23, respectively, a cumulative $15.3 bn more than anticipated for FY22–23 at budget time.

Revenue gains via a stronger-than-expected post-reopening economic rebound this year will be directed to policy measures concentrated in health care and near-term financial support for Quebecers.

Sizeable contingency reserves remain in place throughout the planning horizon to address unexpected cost pressures.

In our view, this is a prudent fiscal plan that, alongside successful virus containment, should position Quebec for a solid recovery from this historic economic event.

OUR TAKE

The government of Quebec has tabled a sensible fiscal blueprint that acknowledges the vital need to tackle the economic and public health consequences of the pandemic, but also remains prudent. Policy supports rightly focus on mitigating the virus’ fiscal costs and strain on the health care system, as well as its immediate and longer-run economic consequences. Sizeable contingency reserves throughout the forecast horizon provide funds to address new pressures in the event that they arise, and also present some upside potential for balances and debt. Finally, the Province’s medium-term plan to keep its net debt-to-GDP ratio on a declining path—enabled by effective pre-pandemic fiscal consolidation efforts—appears appropriately conservative.

Considerable uncertainty to the outlook remains at this time, but implementation of this plan plus successful virus containment should position Quebec for a solid recovery from this historic economic event.

ECONOMIC OUTLOOK

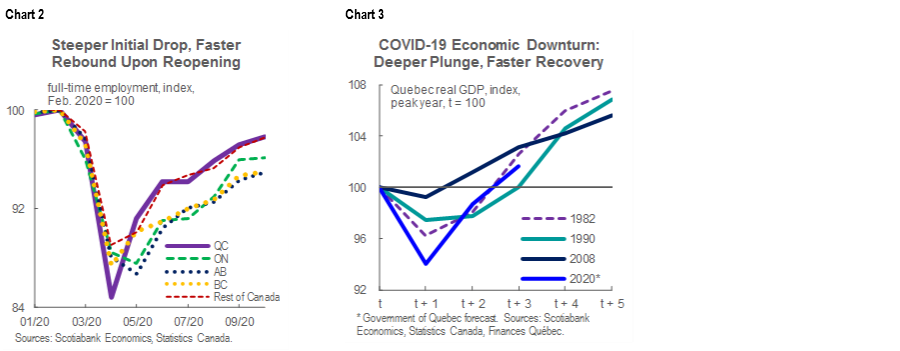

As in the June 2020 update, the Province expects a severe COVID-19-induced economic contraction this year to be followed by a significant rebound in 2021. The drop projected for this year was less pronounced than in June, in respect of Quebec’s particularly strong rebound in output and employment (chart 2, p.2) from first wave restrictions. Gains forecast for 2021 were lowered by 1 ppt to 5%, reflecting a second wave drag and expectations of slower recoveries in sectors like accommodation and food services, disproportionately hit by containment measures. Quebec does not foresee a return to pre-pandemic output levels until 2022, but the abrupt lockdown and bounce-back put Quebec on track to recover its losses more quickly than during some past downturns (chart 3).

The outlook remains subject to considerable uncertainty. Quebec maintains one of the largest per-person COVID-19 caseloads of any jurisdiction in Canada. Case rates appear to have stabilized somewhat since the Province instituted a second round of restrictions (chart 4) and the forecast assumes more targeted, less growth-sapping measures than during the first wave. Still, the fiscal plan acknowledges that a further rise in infections and more all-encompassing restrictions are possible. The blueprint assumes that an effective COVID-19 vaccine will be widely available by the end of next year.

NEW POLICY MEASURES

Policy measures since the June fiscal update fell into three categories: efforts to address public health pressures, financial supports during the pandemic, and measures to facilitate growth as the economy continues to reopen. These build on the $6.3 bn in initiatives announced in June.

The Province anticipates that health system supports announced since the June update will add just over $1.3 bn to its bottom line in FY21. More than $1 bn of these measures consist of enhanced compensation for front-line health care workers. Further funds will be devoted to procuring essential protective equipment.

The Government apportioned $2.7 bn over FY21–23 beyond the June 2020 plan towards actions to support Quebecers. About $2.4 bn of the fiscal impact is expected in FY21, the largest single line item of which consists of $1.9 bn in financial assistance for municipalities. Other measures in this category include financial assistance for students, efforts to promote within-province tourism, and funding to offset revenues lost in the cultural industries as a result of public health restrictions.

New economic restart initiatives are expected to cost nearly $1.5 bn over the next three fiscal years, with more than half of those costs slated for FY22. The Province allocated almost $250 mn to various workforce training measures this fiscal year, with the express aim of supporting firms as they hire workers to relaunch their operations. It will also direct $300 mn through FY23 more to its 2030 Plan for a Green Economy—set to be released later this year—and provide a host of supports for regional economic development, firm-level digitization, and buy local initiatives. As well, previously announced plans to accelerate infrastructure spending are on track and expected to add $2.9 bn to Quebec’s economy, a 14% increase versus FY20.

FISCAL PLAN DETAILS

As a result of the stronger-than-anticipated rebound, Quebec’s FY21 revenue trajectory has improved since June. Own-source revenue projections were revised $2.5 bn higher than expected four months ago, with further assistance for the bottom line via a $515 mn increase in forecast transfers from the federal government. Expenditure plans announced in June were revised modestly lower. The surplus previously projected for FY20 was revised downward to just $32 mn as a result of a pandemic-induced revenue hit and a greater loss provision for the Province’s CSeries investment.

Beyond this year, government receipts are expected to recover gradually, in line with economic growth. The Province anticipates that personal income taxes will hold steady in FY22 after increasing this fiscal year. Despite steep contractions in labour income at the height of the lockdowns, generous (and taxable) government transfers are expected to dominate declines this year.

The Province has penciled in a 4% decline in program expenditures next year as extraordinary pandemic supports—particularly those related to health and economic development—ease. A more normal 3% rise is expected in FY23, with debt servicing costs climbing significantly throughout the forecast horizon, largely as a result of higher debt loads.

The FY21 fiscal room created by stronger-than-expected revenues and modest expenditure savings will be directed towards new policy measures, leaving the previously projected $15 bn accounting deficit intact. However, the smaller FY20 surplus contributed to a nearly $3 bn drop in the value of the Province’s Stabilization Reserve Fund versus June projections. The Fund will still be drained to negate the Province’s FY21 accounting balance, but leave a post-withdrawal shortfall of nearly $3 bn. A hefty $4bn contingency reserve remains in place this fiscal year.

With expenditure gains easing and a gradual recovery in revenues expected over the next several years, the Province expects accounting deficits of $8.3 bn and $7 bn in FY22 and FY23, respectively. The Province will maintain a contingency reserve of $3 bn next fiscal year, and $1 bn in FY23. In light of considerable uncertainty with respect to the outlook, the document did not commit to a timeline for a return to black ink, but reiterated its commitment to boosting economic potential and keeping tax burdens manageable.

DEBT AND BORROWING

As signaled in June, the COVID-19 crisis is expected to end Quebec’s impressive run of seven consecutive annual decreases in its net debt as a share of provincial output. The Province noted that pandemic-related fiscal pressures will make the previously announced target of a 45% gross debt-to-GDP ratio by FY26 very difficult to achieve. However, the government plans to keep both its gross and net debt-to-GDP ratios on downward trajectories—from FY21 to F23, the former is expected to ease from 50.5% to 49.9%, as the latter falls from 43.3% in FY21 to 42.3% in FY23. The figures forecast for both variables are well below the highs reached in FY13–14 (chart 5). Deposits into the Generations Fund are projected to rise from $2.7 bn to $3.2 bn over FY21–23.

In line with increased pandemic-induced deficit spending, Quebec significantly increased the size of its borrowing program. For FY21, forecast borrowing was revised incrementally higher to a total of $32.5 bn, roughly 90% of which had been completed by the end of October and 70% had a maturity of 10 years or more. Total borrowing of $35.3 bn and $31.8 bn are forecast for FY22 and FY23, respectively, a cumulative $15.3 bn more than anticipated at budget time for FY22–23 (chart 6).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.