TAKING STOCK OF CANADA’S PROVINCIAL FINANCES

- Canadian provinces find themselves on strong financial footings as the 2023 budget season kicks off. In this round-up piece, we take stock of where the provinces stand in the ongoing fiscal year (FY23) and what they expect for the next fiscal year (FY24).

- Robust commodity prices and higher-than-anticipated nominal growth inflated government revenues across the country, improving the projected FY23 budget balances by a combined $41.5 bn (1.5% of nominal GDP) as of provinces’ latest updates. Half of the provinces (BC, AB, SK, NB and NL) are on track to record large surpluses this fiscal year.

- Provinces signalled fiscal discipline by keeping new spending initiatives within the bounds of revenue windfalls. Commodity-producing provinces dedicate most FY23 revenue gains to deficit and debt reductions while the others plan to spend larger shares of the windfalls to meet new spending needs. The bulk of new expenses include affordability measures (totalling $9 bn), health care improvements and the recovery from Hurricane Fiona.

- The economic assumptions underpinning the largely improved FY23 budget balances remain reasonable, but slightly more optimistic than forecasted by private-sector economists. The $11 bn set aside in contingencies and allowances should provide a sufficient buffer for the limited downside in FY23 budget balances and leave room for upside as the fiscal year closes.

- Provinces’ combined debt burden is improved owing to better bottom lines in FY23, with expected net debt to run at 28% of GDP (versus earlier-projected 33%)—the lowest level in over a decade.

- Provinces’ borrowing requirements are also expected to come in much lower than previous estimates in 2022 budgets, totalling $65 bn for the three largest provinces (ON, QC and BC), with Alberta eliminating both capital and fiscal borrowing planned for this fiscal year and next thanks to abundant surplus cash.

- Provinces should see revenue windfalls to unwind in FY24 and could expect some deterioration in fiscal balances despite a strong handoff from FY23, with heightened uncertainty around the outlook. The four largest provinces (ON, QC, AB and BC) currently project a combined deficit of -$8.6 bn (-0.3% of GDP) in FY24, including $9.9 bn in contingencies and forecast allowances in anticipation of economic uncertainty and additional spending pressures.

- In an environment of persistently high inflation and slowing growth, it is paramount for the provinces to maintain fiscal discipline against stronger fiscal trajectories and some new-found surpluses to avoid complicating the Bank of Canada’s job to keep inflation under control, and save the fiscal room to support households and businesses in case of a deeper recession.

STRONG NOMINAL GROWTH INFLATED PROVINCIAL COFFERS

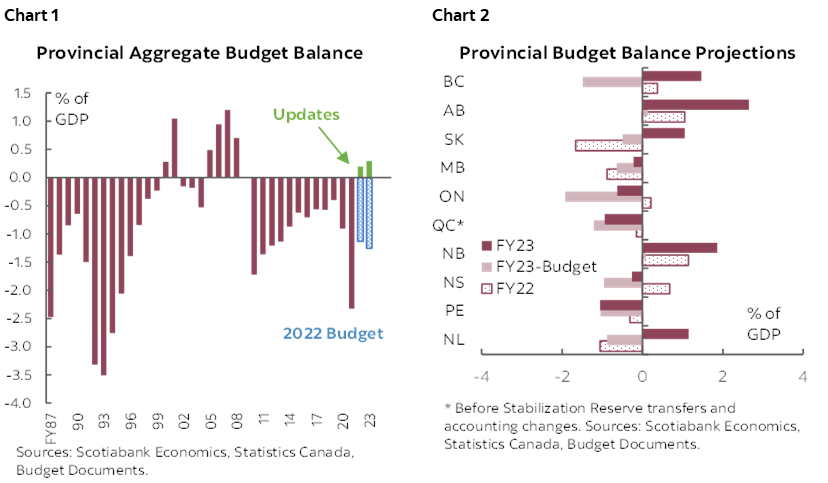

Provinces saw substantial improvements in their finances through 2022 (chart 1). Collectively, the provinces reduced their FY23 deficit estimates by a total of $41.5 bn (1.5% of nominal GDP) in the latest fiscal updates and are projecting an aggregate surplus of $8.3 bn (0.3% of GDP). This marks the second year in the black for the provincial governments, following the $4.8 bn (0.2% of GDP) aggregate surplus recorded in FY22. Half of the provinces (BC, AB, SK, NB and NL) are on track to record large surpluses in FY23, and the others see significant reductions in projected deficits to less than 1% of nominal GDP, with PEI being the only exception (chart 2).

All provinces anticipate improved bottom lines in light of higher-than-expected inflation and stronger commodity prices than previously assumed. Provinces across the country saw windfalls through the fiscal year in an environment of rising inflation, despite slowing real growth due to the monetary policy efforts to tamp it down. As of mid-year, commodity exporters saw the largest windfalls owing to much higher commodity prices than those assumed in the previous budgets, which were made before the full impact of the Russia-Ukraine war materialized.

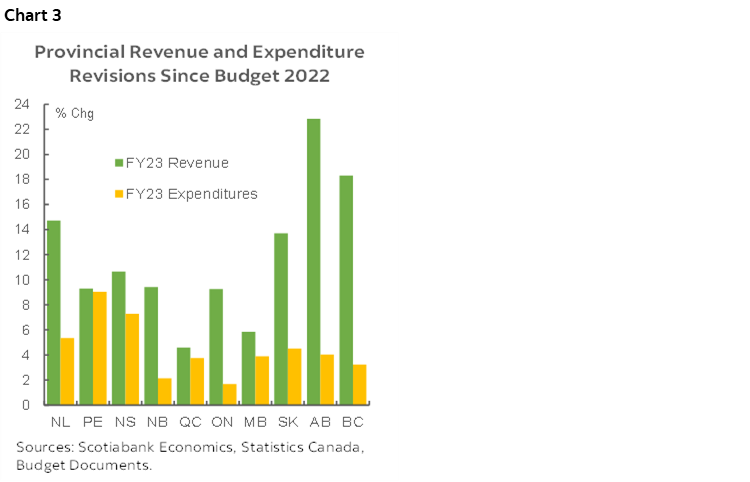

Faced with heightened spending pressures from rising costs of living, health care improvements and the impact of Hurricane Fiona, provinces managed to keep new spending initiatives within the bounds of increased revenues (chart 3). Provinces with larger windfalls—mainly commodity producers—dedicated most revenue gains to deficit and debt reductions. Collectively, provinces plan to spend around 30% of the $57 bn estimated windfalls to meet new spending needs, including a combined $9 bn in affordability measures announced over the course of FY23. Nova Scotia and PEI saw the largest increases in new spending as they pencilled in expenses related to recoveries from the impact of Hurricane Fiona.

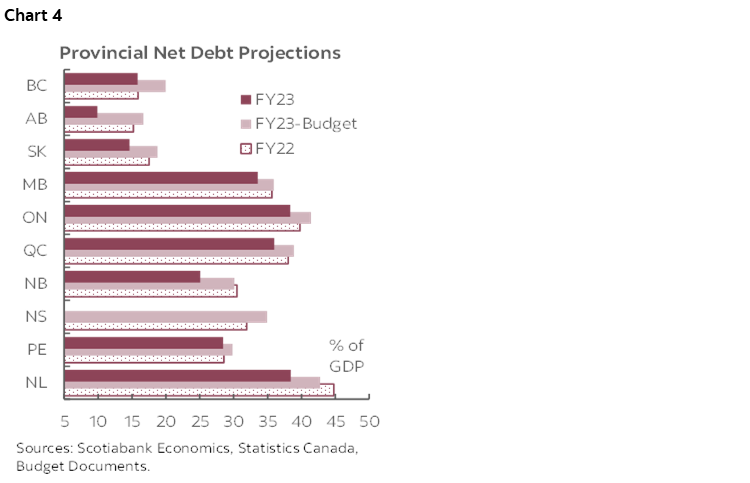

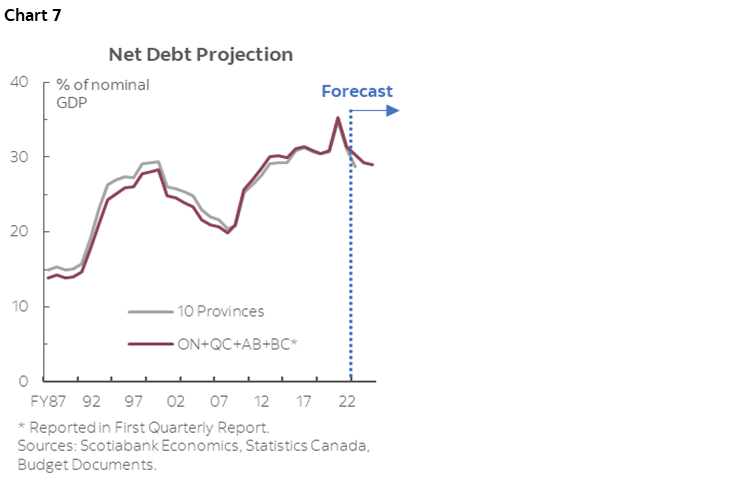

Almost all provinces project smaller and declining debt burdens in FY23 as a share of nominal output (chart 4). The aggregate provincial net debt is expected to run at 28.7% of GDP instead of the 33% projected in 2022 budgets, the lowest level in over a decade. Other than the commodity-producing provinces that project large reductions in debt as a share of output, New Brunswick is showing great efforts by slashing its debt burden rapidly by over 10% of nominal GDP in the past two fiscal years, supported by its sizable budget surpluses. Provinces with high debt burdens such as Quebec and Manitoba are also projecting steady reductions in debt as a share of output. Nova Scotia did not update its net debt projection, but should see some improvements given a smaller deficit forecast and decreased capital spending.

SIZABLE CONTINGENCIES PROVIDE A SUFFICIENT BUFFER FOR UNCERTAINTY IN THE OUTLOOK

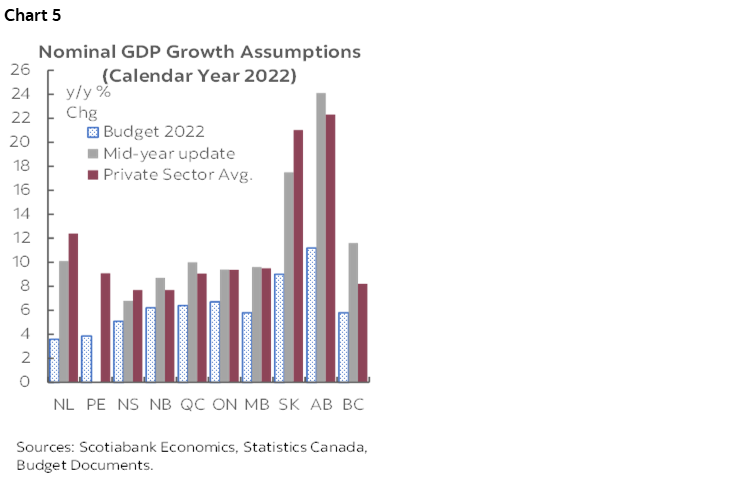

Economic slowdowns that started in the second half of 2022 continued well into 2023, and despite the recent resilience in labour markets, heightened uncertainty brings downside risks to the current projections and clouds the outlook. Provinces revised up nominal growth assumptions for calendar year 2022 in their mid-year updates to incorporate a higher inflation outlook, and brought down forecasts for 2023 as real growth slows and inflation moderates. Overall, the economic assumptions underpinning the current outlook are in line with private-sector forecasts (chart 5), but risks are tilted to the downside with some provinces assuming higher growth than estimated by private-sector economists.

Oil price assumptions used in mid-year updates seemed conservative at the time, but didn’t provide much buffer for near-term volatility. Alberta’s WTI price projections were very close to levels suggested by the pricing of WTI futures, averaging US$91.5/bbl in FY23 before dropping to US$78.5/bbl in FY24. Saskatchewan expects WTI prices to average US$91.0/bbl in FY23. These assumptions are still slightly below the current WTI price average so far in the fiscal year (about US$92/bbl), and even with continued downward pressure in commodity prices, the impact on FY23 deficits should be marginal compared to the substantial windfalls forecasted in the oil-producing provinces.

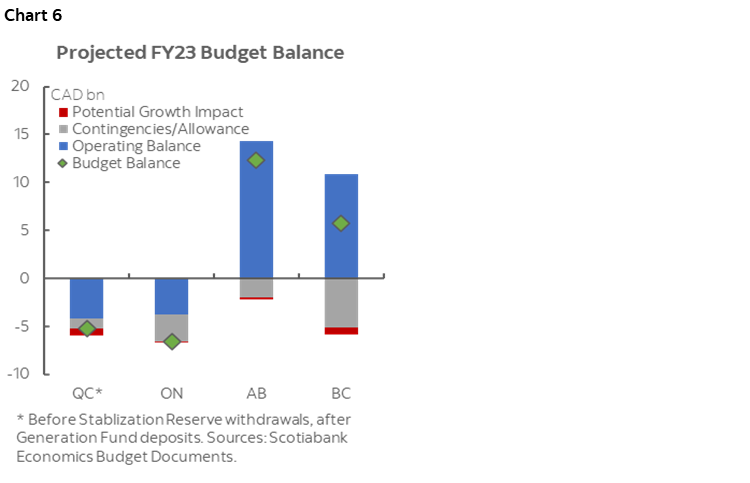

Provinces maintained sufficient buffer to absorb uncertainty in economic forecasts, which leaves plenty of room for upside as the fiscal year closes. Half of the provinces set aside sizable contingencies and forecast allowances in their 2022 budgets, and about $11 bn were left for FY23 as of mid-year. Since the downside of economic uncertainty should be relatively contained, a large fraction of this fiscal buffer could be used to further improve the bottom lines in FY23 (chart 6).

HOWEVER, SURPLUSES ARE (PROBABLY) NOT HERE TO STAY

A strong handoff from FY23 should put provinces on better fiscal trajectories, but as revenue windfalls wind down in FY24, provinces will need to strengthen their effort in consolidation. Ontario is forecasting an -$8.1 bn (-0.8% of nominal GDP) deficit for FY24 in its fall update, which should see some improvement in the upcoming budget since the third-quarter update raised FY23 revenue by $9.6 bn versus the fall update, bringing FY24 to a better starting point. In its mid-year update, Quebec plans to reduce its post-Generation Fund deficit from -$5.3 bn (-0.9% of GDP) in FY23 to -$2.3 bn in FY24 (-0.4%) by keeping expenses flat. Alberta projects another sizable yet much narrower surplus of $5.6 bn (1.2% of GDP) with its non-renewable resource revenue declining by 32% ($9 bn) in FY24. In its first quarterly report released in September 2022, BC expects a return of deficit in FY24 at -$3.8 bn (-0.9% of GDP), driven by the drawdown of its revenue windfalls. Tallying up the current FY24 deficit projections, provinces’ aggregate surplus is unlikely to sustain.

Provincial aggregate net debt should continue to moderate as a share of output in FY24—mostly due to the sizable surplus projected in Alberta while other provinces could face increased debt burdens (chart 7). Ontario and Quebec expect continued growth in net debt and remain elevated as a share of their respective nominal GDP in the next two fiscal years. BC projects a steady upward trend in net debt in FY24 and FY25, albeit from low levels.

PLENTY OF UNCERTAINTY AHEAD

The economic assumptions underpinning the deficit and debt outlook of the four largest provinces seem reasonably conservative for now, but there are still plenty of downside risks to the revenue outlook. Recession is still a material risk in some provinces this year, particularly in Quebec, Ontario and BC where real growth has been slowing sharply, which is not accounted for in their baseline projections. Quebec provided an alternative recession scenario in its mid-year update with its economy contracting by -1% in real terms in 2023, which has a fiscal impact of -$1.8 bn in FY24. Ontario’s slower growth scenario pencils in a -0.9% real contraction in 2023, adding -$5.8 bn more deficits to the province’s FY24 budget balance. The four provinces set aside a combined $9.9 bn in contingencies and forecast allowances in FY24 in anticipation of economic uncertainty and additional spending pressures.

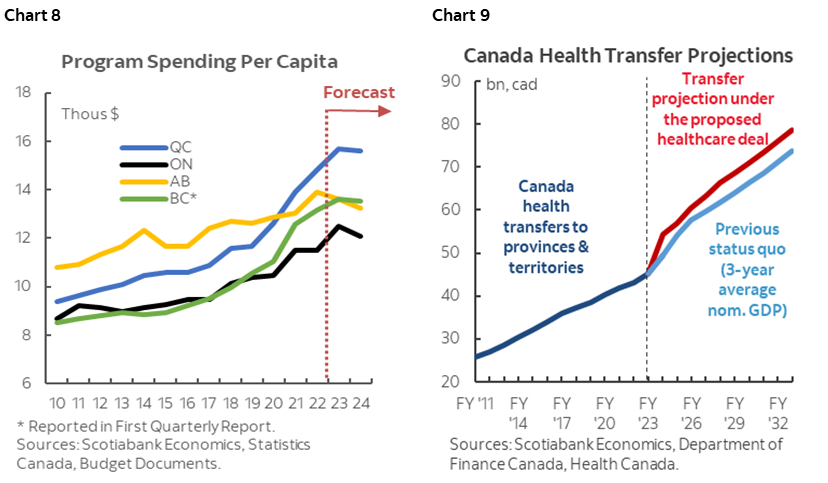

With significant downside risks in the revenue outlook, provinces need to show more consolidation effort in the upcoming budgets and hold the line on spending. Despite subsiding spending pressures from pandemic control and cost-of-living support, provinces still plan to keep program expenses elevated and well above pre-pandemic levels in per capita terms (chart 8). BC and Quebec have been raising program spending aggressively since 2020 and plan to keep it at peak levels in FY24. Alberta brought down program spending per capita to levels in line with BC and the national average but slightly eased expenditure restraint with some of its newfound windfalls. Ontario has the lowest program spending per capita and will likely face more pressure to increase expenditures to serve its growing population. All provinces will see increasing costs next fiscal year in an environment of high price and wage inflation, making it increasingly challenging to hold the line on spending. The $46.2 bn new health funding over 10 years recently announced by the federal government should alleviate some spending pressure in health care, including an immediate $2 bn top-up and a guaranteed 5% growth top-up payment to the Canada Health Transfer (chart 9).

BORROWING AND DEBT MANAGEMENT

Provincial borrowing requirements in FY23 were revised significantly lower than anticipated in previous budgets. The four largest provinces are projected to borrow a total of $65 bn in FY23—$25 bn lower than anticipated in 2022 budgets. Alberta eliminated both capital and fiscal borrowing planned for this fiscal year thanks to abundant surplus cash, and instead dedicated $13.4 bn to pay down debt, while planning to pause borrowing again in FY24. Ontario and Quebec both expect higher funding requirements in FY24 with increased refinancing needs, currently forecasting $38.4 bn and $32 bn in long-term borrowings, respectively. The actual borrowings could eventually be lower considering the size of contingencies and provisions built into the fiscal plans.

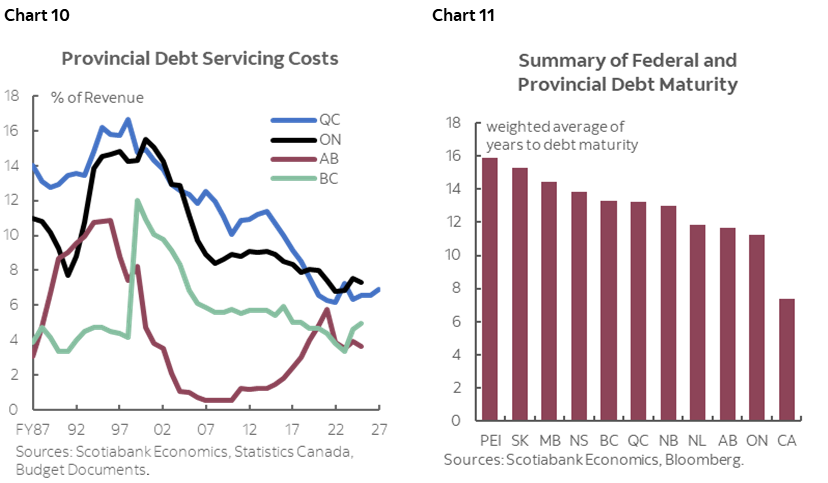

Provinces will spend more to service debt amid elevated interest rates, but only marginally higher as a share of total revenue. Debt servicing costs were revised down in FY23 in most provinces as lower-than-anticipated debt burden offset rising interest rates on outstanding borrowings. Debt servicing costs are set to increase in FY24 (except for Quebec due to the one-time loss of the Sinking Fund recorded in FY23), but only incrementally as a share of revenue and still stand at very low levels historically (chart 10). The provinces proactively manage interest rate risks by maintaining relatively long average maturities (chart 11). Ontario also set a new target aiming to keep debt maturity to net debt ratio below 10% (which stood at less than 8% as of mid-year).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.