PROVINCIAL FALL FISCAL UPDATES PREVIEW

- Many provincial fiscal outlooks have deteriorated due to weaker growth, spending increases, and/or oil price declines.

- While Ontario and Quebec showed unchanged deficit projections for 2025–26 (FY26) in their Q1 fiscal updates, the other seven provinces that released Q1 updates showed a worse budget balance projection compared to their budget forecast, with the largest deteriorations in Alberta, British Columbia (B.C.) and Nova Scotia.

- However, the final numbers for FY25 came in better than previously projected in most provinces, leading to a better handoff, especially for net debt burdens. As a result, net debt projections for FY26 were broadly unchanged in the Q1 updates.

- Over the next couple of months, provinces will publish their mid-year fiscal updates, starting with Ontario on November 6th.

- Our latest economic projections are broadly in line with most provinces’ growth assumptions in their Q1 updates. In addition, new spending announcements have broadly been within contingency envelopes.

- As a result, we expect most provinces’ mid-year updates to be broadly in line with their Q1 updates (i.e., unchanged or somewhat worse deficits compared to the Spring budget projections).

- Pressures for new spending are likely to continue, including to support businesses and workers impacted by the ongoing tariffs from the U.S. and China. However, most provinces have built in prudence and/or contingency reserves into their fiscal frameworks to help fund new measures.

- Credit spreads in all provinces have narrowed over the course of the year, though Alberta and Newfoundland & Labrador have enjoyed the largest reductions.

Q1 UPDATES ROUND-UP

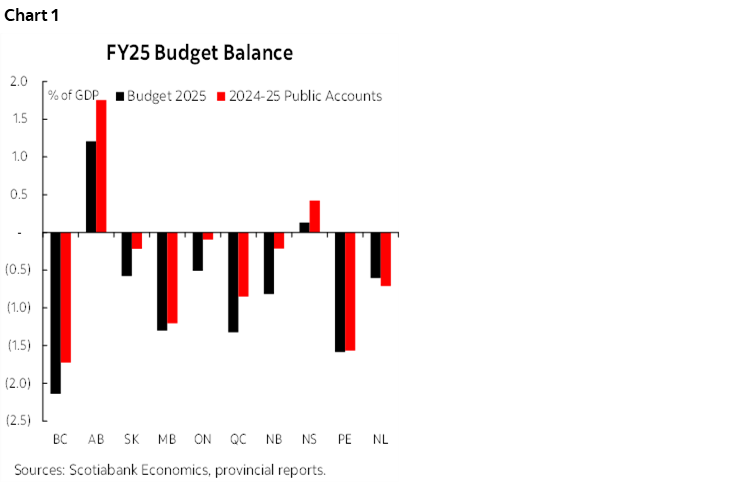

Almost every province overperformed its Budget 2025 estimates for FY25 (chart 1). Each province released its 2024–25 Public Accounts over the past few months, and New Brunswick and Alberta led the pack by beating the budget balance estimate in their Spring budget by more than 0.5% of GDP. Quebec, B.C., and Ontario were not far behind at around 0.4% of GDP. Alberta and Nova Scotia were the only provinces that recorded a surplus last year, but Ontario, Saskatchewan, and New Brunswick were close to balance, registering deficits of 0.2% of GDP or less. B.C. and Prince Edward Island registered the largest deficits, at more than 1.5% of GDP.

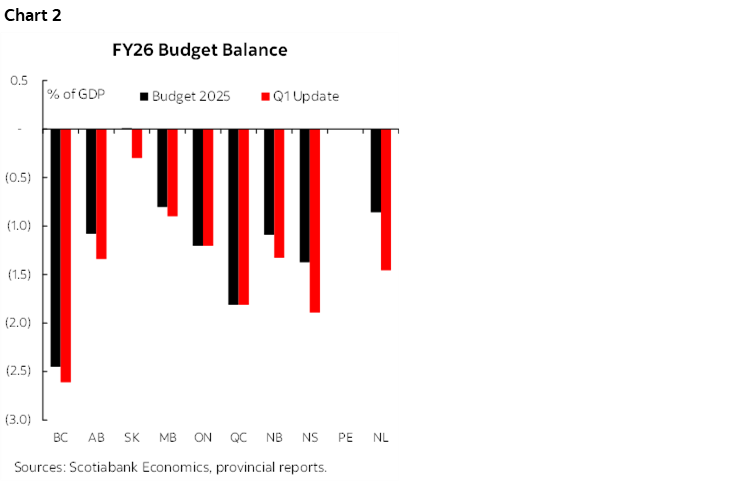

The Q1 fiscal updates showed mostly worsened outlooks for FY26 (chart 2). While Ontario and Quebec did not make changes to the deficit projections for this year (FY26) compared to their Spring budgets, the other seven provinces that released Q1 fiscal updates increased their deficit projections—led by Newfoundland & Labrador and Nova Scotia at over 0.5% of GDP. Six provinces revised down their revenue projection, given the slowdown in the economy and lower oil prices, with Newfoundland & Labrador revising revenues down the most at -2.4%. Alberta’s revenue revision was more modest, as a narrower light-heavy differential helped to offset some of the impact of lower WTI prices. On the spending side, six provinces also revised up their spending projections, with Nova Scotia seeing the highest at 2.8% (reportedly driven by higher health care service utilization). Most provinces are now forecasting deficits of between roughly 1% and 2% for this year, with B.C. the outlier on the high side at 2.6%, and Saskatchewan the outlier on the low side at 0.3%.

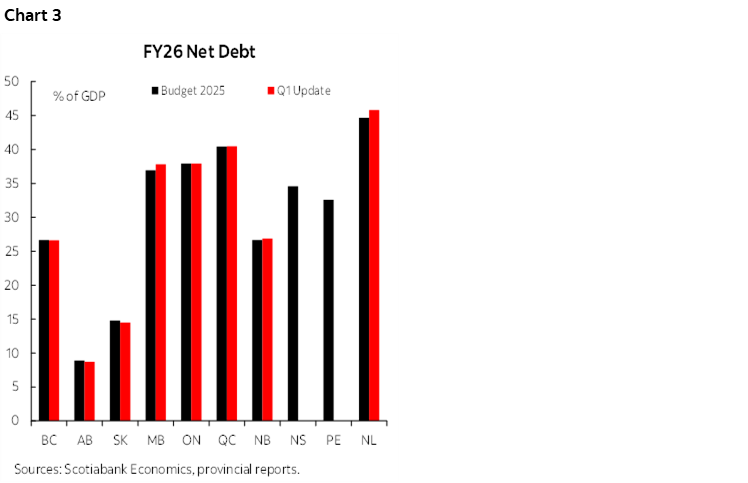

Net debt projections for FY26 were broadly unchanged in the Q1 updates (chart 3). The FY25 overperformance in most provinces has led to a better net debt number to start this year, helping to offset the increased deficit projections for most provinces. Newfoundland & Labrador and Quebec continue to project the highest net debt burdens for this year, and Alberta and Saskatchewan continue to project the lowest.

ECONOMIC CHALLENGES CONTINUE

While some of the downside risks to the macroeconomic backdrop have eased, the outlook remains uncertain and challenging. The U.S. tariffs have been less harmful than some initially feared, thanks to most Canada-U.S. business continuing on a free-trade basis under CUSMA. However, the U.S. continues to announce new tariff measures, and the tariffs and related uncertainty continue to weigh on growth and the labour market. The Bank of Canada made two additional rate cuts this Fall to provide additional support to economic activity.

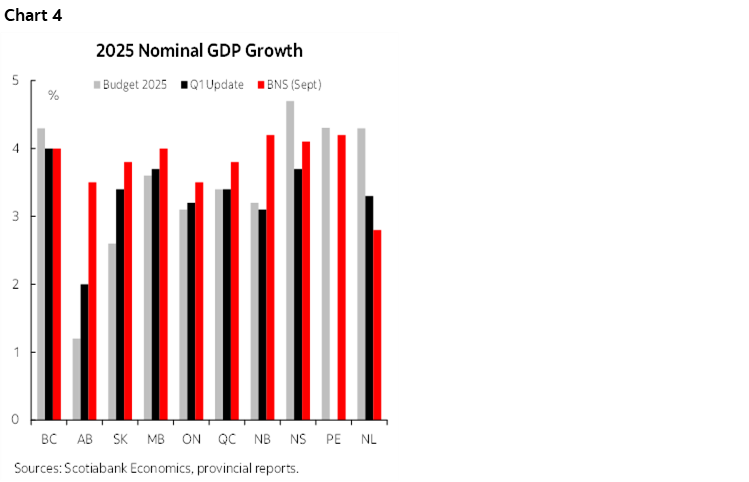

Recent provincial growth assumptions are broadly in line with our views. Most provinces made changes to their assumed economic growth rates for 2025 in their Q1 updates (chart 4), with some revising down and some revising up—in part reflecting the fact that some provinces set the growth assumptions for their Spring budgets before the tariff war started. However, most provinces’ latest growth assumptions (which drives revenues forecasts) are broadly in line with our views—with perhaps the most scope for Alberta to come up, and Newfoundland & Labrador to come down. However, growth in these oil-producing provinces is fairly volatile and difficult to forecast with accuracy. Overall, we continue to expect modest but positive growth in each province.

FALL UPDATES COULD INCLUDE NEW MEASURES

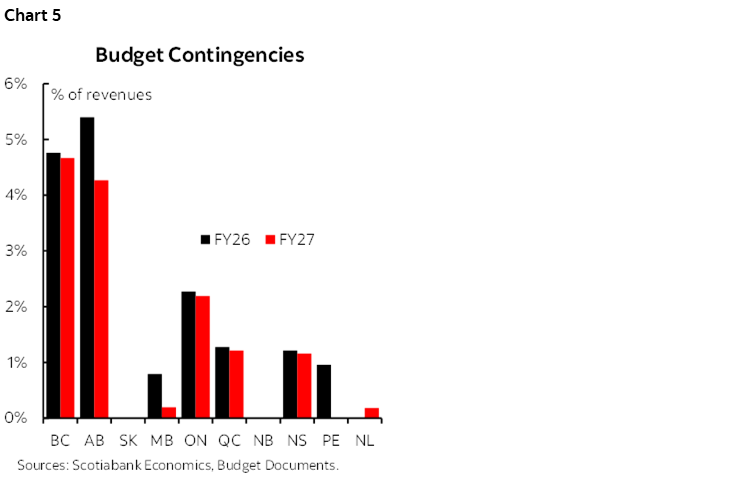

Provinces may start to use some of their contingency budgets to fund new measures. Many provinces set aside considerable contingency funds in their Spring budgets to protect against lower revenues and/or new spending pressures (chart 5). With some of the downside risks abated, some may choose to use some of their contingency reserves to fund new measures. Ontario has already announced that it will include in its mid-year update an expansion of its GST rebate on new homes, to fully refund the 8% provincial portion of the HST for first-time homebuyers. This is a fairly narrowly scoped measure, which should be able to be absorbed with Ontario’s considerable forecast buffers.

The new government in Newfoundland & Labrador is starting to implement its agenda. A new PC government formed earlier this month, running on a platform of broad tax relief, targeted benefits for seniors and students, and increased funding for policing. While we expect most major measures will be saved for the next Spring budget(s), there could be some initial new measures announced as part of the Fall update. However, fiscal space is likely limited. Newfoundland & Labrador’s Q1 update showed a deterioration in the fiscal outlook, and the new government has started a review of, and has committed to holding a public referendum on, the agreement with Hydro Quebec on the expansion of Churchill Falls. This could potentially put at risk some of the potential associated provincial revenues, which were baked into Newfoundland & Labrador’s Spring budget projections.

SPREADS NARROWER DESPITE THE CHALLENGING FISCAL LANDSCAPE

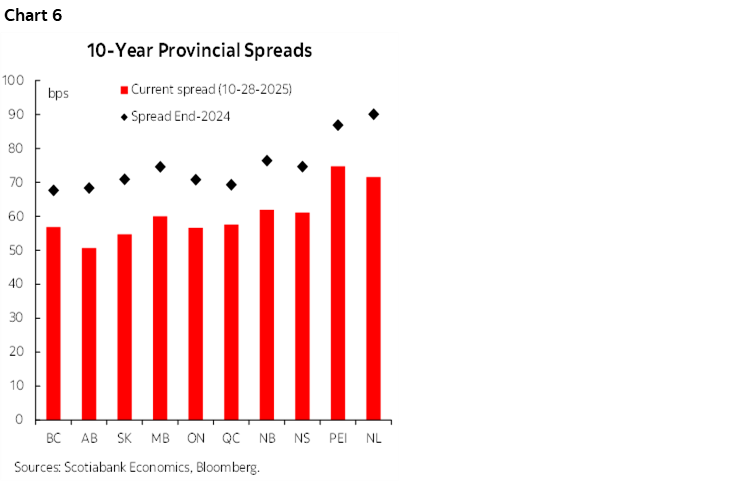

The challenging fiscal environment has led to some credit actions, but spreads have narrowed. S&P downgraded B.C. and Quebec over the summer, with Moody’s also downgrading B.C. The outlook for a number of provinces were also downgraded. Despite the deteriorated outlook, spreads in all provinces have narrowed over the course of the year. 10-year spreads down 10–20 basis points, with Alberta and Newfoundland & Labrador enjoying the largest reductions (chart 6).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.