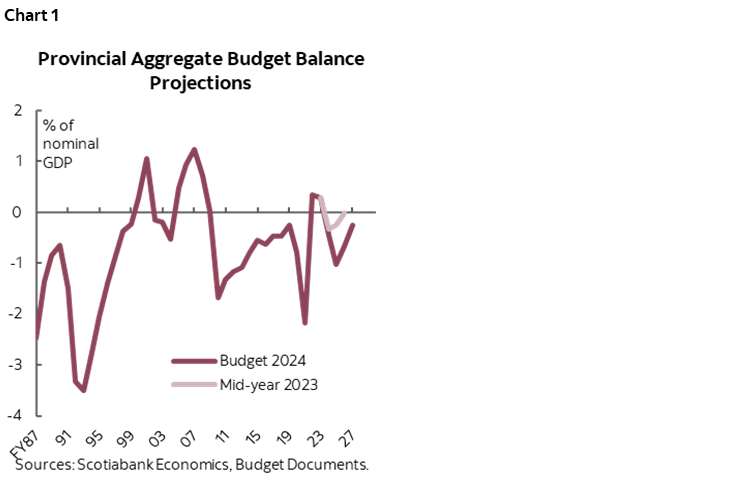

- 2024 budgets revealed further downside from a slowing growth outlook and a multitude of public finance challenges. The provinces experienced varying degrees of deterioration in their bottom-lines, projecting a deeper aggregate deficit of -$12.7 bn (-0.4% of nominal GDP) in FY24—a -$2.9 bn deterioration since the mid-year updates, followed by a substantial shortfall of -$30.1 bn (-1.0% of GDP) in FY25 (chart 1).

- Revenue outlook is a mixed bag as moderate windfalls from robust economic momentum encounter stronger headwinds. Broad-based spending boost is the driver of deterioration.

- The provinces have generally taken a reasonable approach in their economic forecasting and budget planning. Most provinces foresee moderate slowdowns this year, but some appeared complacent regarding potential downside risks of a more severe downturn.

- The largest four provinces demonstrated prudence by setting aside about $9.9 bn as contingencies and provisions in FY25, followed by another $8.0 bn in FY26 and $9.2 bn in FY27, providing a sizeable buffer for unforeseen losses in revenues and additional spending needs.

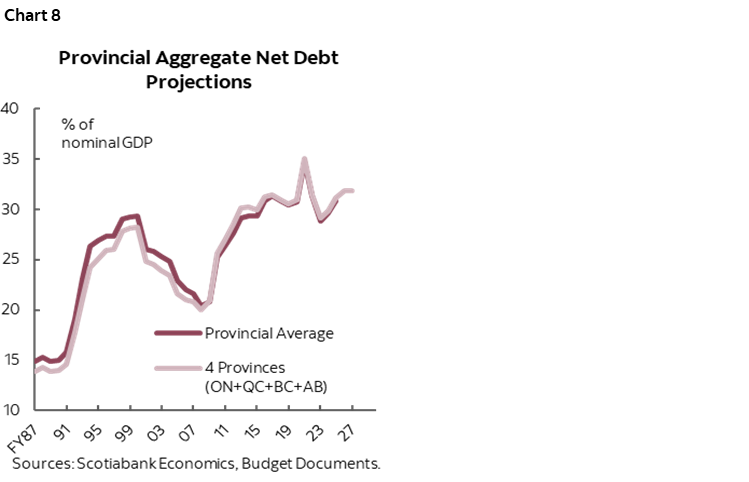

- Provinces still face rising debt burdens, with many expecting higher net debt-to-GDP ratios in the medium term. The aggregate ratio is anticipated to climb to 30.9% in FY25 and continue on an upward trajectory, nearing 32% in FY26 and FY27.

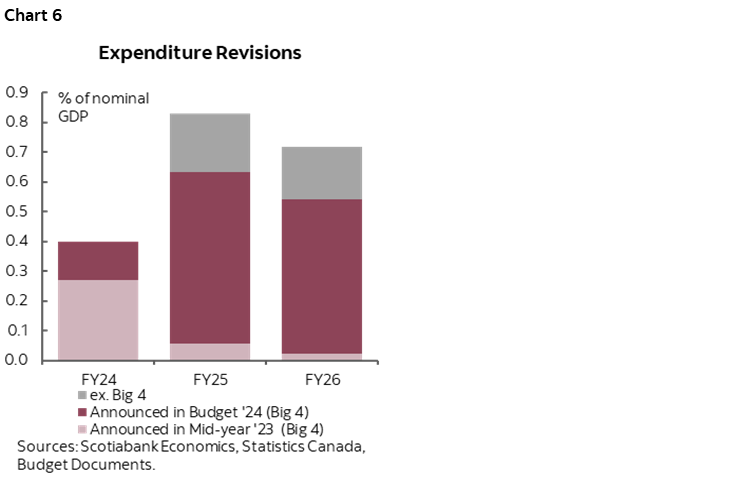

- The provinces collectively announced $23 bn (0.8% of GDP) new spending in FY25 and another $21 bn (0.7%) in FY26, which should provide further support to growth this year and next while having an impact on inflation.

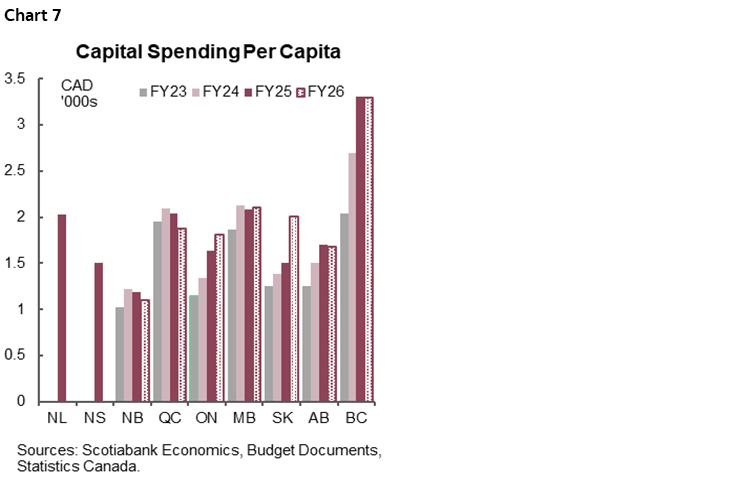

- Provinces have ramped up infrastructure spending, totalling $86.5 bn this year—a 15% surge from the previous year—with elevated levels set to continue next year.

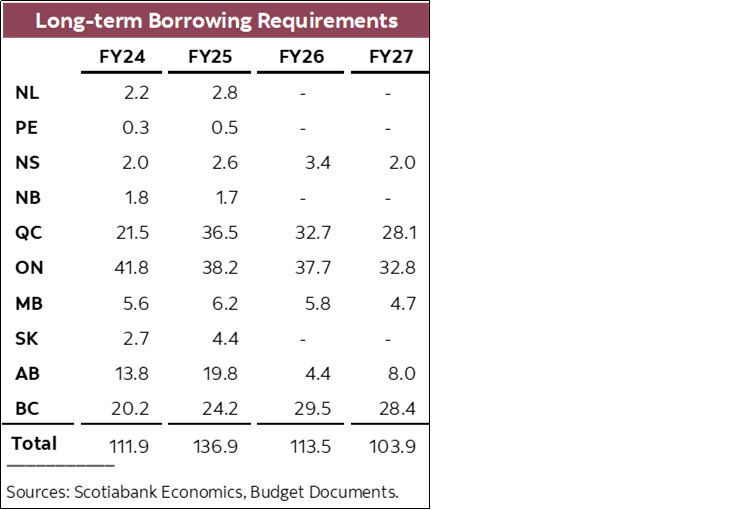

- Provinces’ borrowing requirements are expected to total $136.9 bn in FY25, up from $111.9 bn completed in FY24.

- Despite broad-based deterioration, most provinces maintain relatively sound fiscal standings. As the pressure from inflation and population growth gradually subsides in the medium term, fiscal outlooks should improve, albeit contingent on continued prudent planning amid heightened uncertainty.

DETERIORATION ACROSS THE BOARD

2024 budgets revealed deteriorations across the board relative to the mid-year updates and last year’s budgets, mainly driven by broad-based spending increases in essential government services. With the exception of Nova Scotia and New Brunswick, most provinces found themselves on a worsened fiscal path due to spending increases well surpassing limited revenue windfalls. Aggregate deficit is expected to come in at -$12.7 bn (-0.4% of nominal GDP) in FY24 before widening to -$30.1 bn (-1.0% of GDP) in FY25—over -$20 bn (-0.7%) higher than projected in provinces’ previous plans. Over the medium term, the provinces expect robust revenue growth to gradually reduce the shortfall to -$20.7 bn (-0.7% of GDP) in FY26 and -$7.9 bn (-0.2%) in FY27.

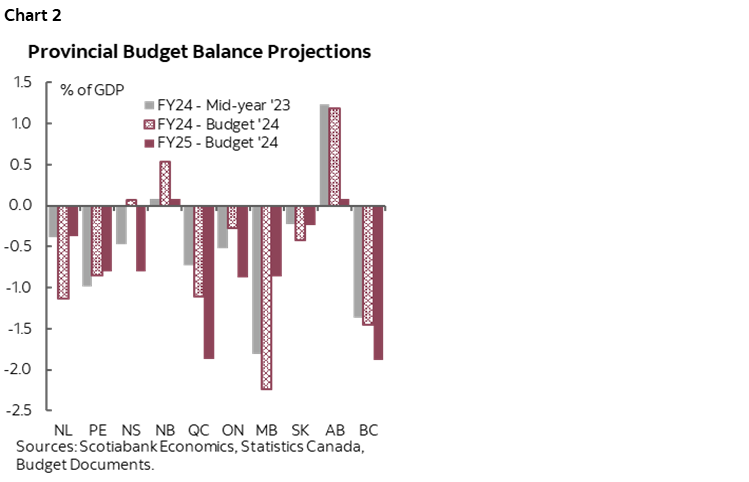

Deterioration is widespread, albeit with pockets of optimism (chart 2). Alberta remains a bright spot despite a lifted spending plan. The streak of surpluses persists in New Brunswick with heightened spending absorbed by continued windfalls. Saskatchewan holds a slight advantage despite dipping into deficit. Manitoba anticipates a fiscal turnaround in FY25 driven by a revenue boost, slashing the deficit by half. On the other hand, deeper deficits loom for British Columbia (-1.9% of GDP), Quebec (-1.9%), Ontario (-0.9%), Nova Scotia (-0.8%), and Prince Edward Island (-0.8%) in FY25.

REVENUE GROWTH STILL SUPPORTIVE BUT WITH DOWNSIDE RISKS

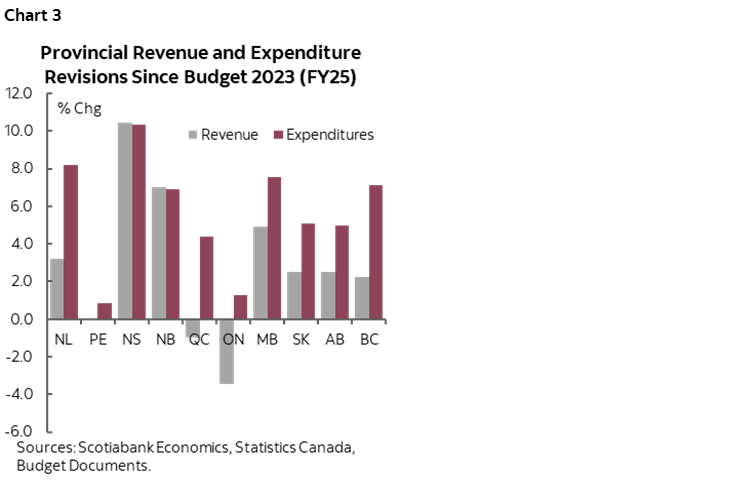

Revenue revisions present a mixed picture, with robust economic momentum supporting tax revenues but some soft patches remain. Relative to last year’s forecasts, most provinces saw upward revisions in revenue, with the exception of Quebec and Ontario (chart 3). Tax revenue outlook from previous plans still largely holds with upside in some provinces such as Alberta and the Maritime provinces, but idiosyncratic factors have led to some downside. Quebec anticipates a drop in Hydro-Quebec’s contribution, while Ontario expects weaknesses to persist following last year’s downward revision due to tax reassessment. Resource revenues are expected to drop in FY25, especially with Alberta’s conservative oil price assumptions, but a narrower light-heavy differential helps support resource revenues and corporate profits.

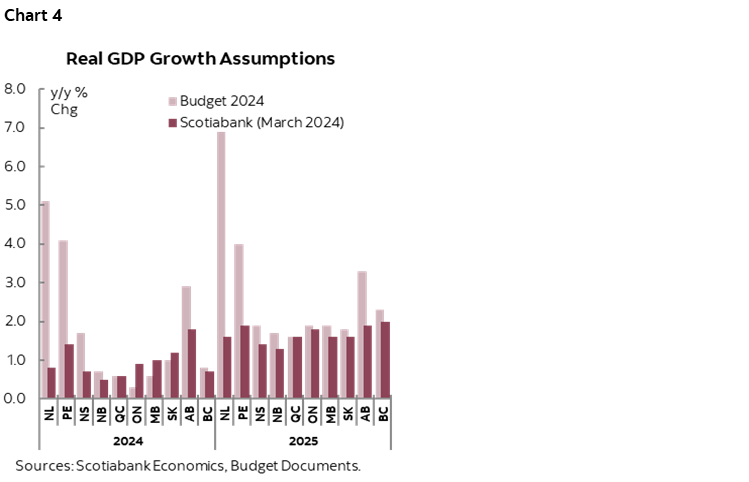

While prudently factoring in commodity risks, the economic assumptions appear plausible, albeit with a touch of optimism. With minor revisions since the mid-year updates, most provinces expect a slowdown this year, yet they do not anticipate a recession (chart 4). Alberta, Nova Scotia and Prince Edward Island defy the trend, projecting accelerated expansion in 2024 compared to the preceding year. We consider these projections realistic since we do not subscribe to the recession view, but some of them might be too complacent relative to our latest forecasts. Oil price assumptions—established before the ongoing upswing in the commodity market—appear prudent and could yield further upside over the course of the year if the current market momentum persists. Alberta and Saskatchewan expect WTI price to average 74 USD/bbl and 74 USD/bbl in FY25, respectively—well below the current price. The current oil price environment remains conducive to this forecast thanks to a tight supply-demand dynamic.

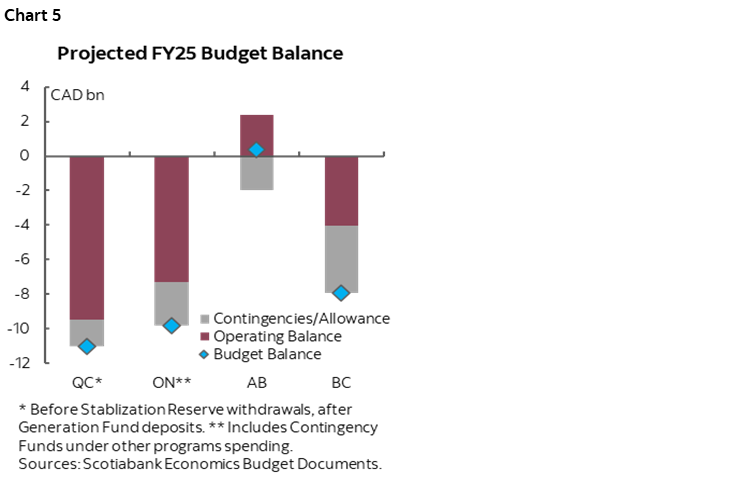

The four largest provinces incorporated prudence through the use of contingency funds and forecast reserves, which, if unused, could contribute to sizable improvement (chart 5). Ontario allocated $1.0 bn in a forecast reserve along with $1.5 bn in contingency funds under program spending in FY25. British Columbia (BC) has set aside a hefty $3.9 bn in contingencies vote in anticipation of future cost increases, no forecast allowance. Quebec and Alberta have allocated $1.5 bn and $2.0 bn respectively as forecast reserves in FY25. Manitoba is the only other province that included contingencies, which amount to $100 mn.

SPENDING SURGE CENTRES ON WAGE PRESSURES

All provinces have announced significant spending increases to address rising structural spending needs from public wage pressures and population growth. In their 2024 budgets, the provinces collectively announced $23 bn (0.8% of GDP) of new spending in FY25 and another $21 bn (0.7%) in FY26 (chart 6). Program spending is now set to rise by 4.2% in FY25—commensurate with the rate of growth in FY24. The majority of the increases stem from rising operational costs resulting from public-sector wage negotiations, with the remaining funds directed toward critical priorities such as improving provinces’ healthcare systems. Additional spending beyond public services appears incremental and properly targeted, which could prove beneficial for growth. Debt servicing costs are projected to grow by 7.6% in FY25 but remain affordable at 6.1% of total revenues—still below their pre-pandemic levels.

Provinces once again announced hefty infrastructure spending to meet growing demand, collectively boosting planned outlays by around 15% in FY25 (chart 7). Ontario is aiming to raise capital spending per capita notably in the next two years by over 35% and bringing it to levels more in line with its peers following a history of consistently lagging behind. BC and Saskatchewan have also planned significant infrastructure investments in the next two years with capital spending per capita growing at respective rates of 22% and 44%, supporting growth in the ongoing slowdown. Investing in public infrastructure plays a pivotal role in fostering long-term economic growth and bolstering essential services, yet maintaining capital spending momentum can prove increasingly challenging due to persistent labour shortages within the construction industry.

TREADING CAREFULLY WITH A GROWING DEBT BURDEN

The provinces still face challenges from an elevated net debt burden. The combined net debt burden is expected to rise in FY25 to 30.9% of GDP and run at levels just below 32% of GDP in the coming years (chart 8)—1–2 ppts higher than the trajectory laid out last year. Most provinces face high and increasing levels of indebtedness. Newfoundland and Labrador continues to carry the largest debt burden in FY25 but is projected to improve slightly relative to last year. Quebec and Ontario hold the second and third place with notable projected increases in net debt-to-GDP through FY25–FY26 to 41% and 39.5%, respectively. BC foresees the fastest growth in net debt burden in the next two years but still ranks favourable compared to its peers. On the other hand, Alberta, New Brunswick and Saskatchewan maintain low and stable net debt burden over the planning horizon.

Planned total borrowings are projected at $25 bn higher in FY25 than in the year prior (table 1). Increased supply could put upward pressure on provincial spreads, particularly for provinces such as BC and Quebec which saw the largest bottom-line deteriorations. However, given the abundant contingencies and allowances built into the budget and the possibility of capital project delays, borrowing requirements will likely come in lower over the course of the year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.