- Provincial governments released their 2026 budgets with somewhat less uncertainty from trade issues, but in the midst of a new conflict in the Middle East.

- The budgets showed that the provinces generally expect another year of relatively modest revenue growth and continuing spending pressures from health and other core services. Some governments announced new affordability measures, but these were generally quite narrow in scope—helping keep incremental costs low.

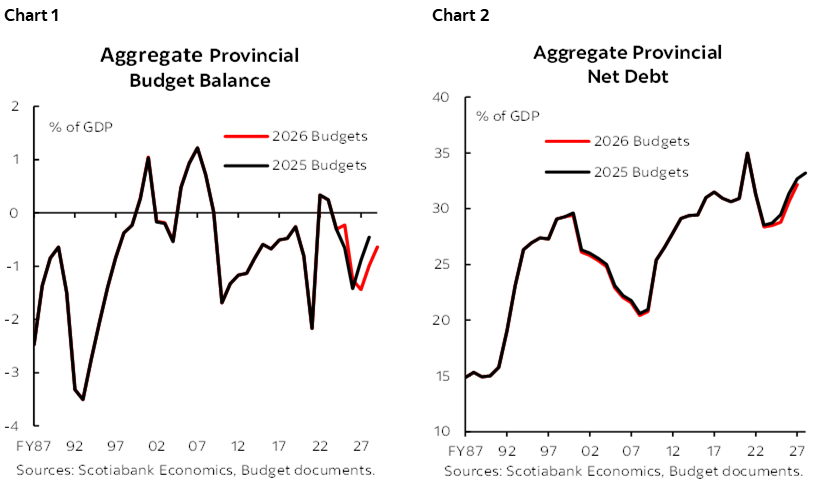

- Taken together, the provincial budgets’ baseline scenarios project a slight increase in the aggregate provincial deficit from $40.3 bn (1.3% of nominal GDP) in FY26 to $47.8 bn (1.4% of GDP) in FY27.

- Despite the increase in the aggregate provincial deficit, as a share of GDP it remains lower than recessionary periods, and less than half the level of the fiscal stress period of the early 90s (chart 1).

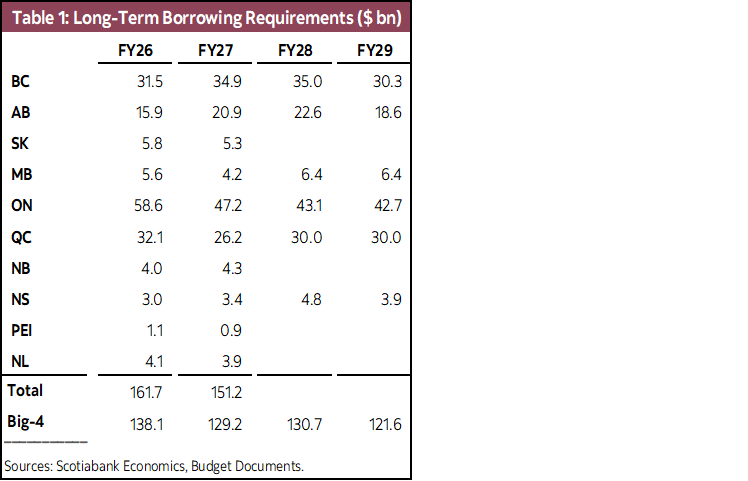

- Provinces’ borrowing requirements are expected to remain elevated at $151 bn in FY27, a bit lower than the $162 bn raised in FY26 but still substantially more than most years. This reflects the ongoing operational deficits and elevated capital spending in most provinces.

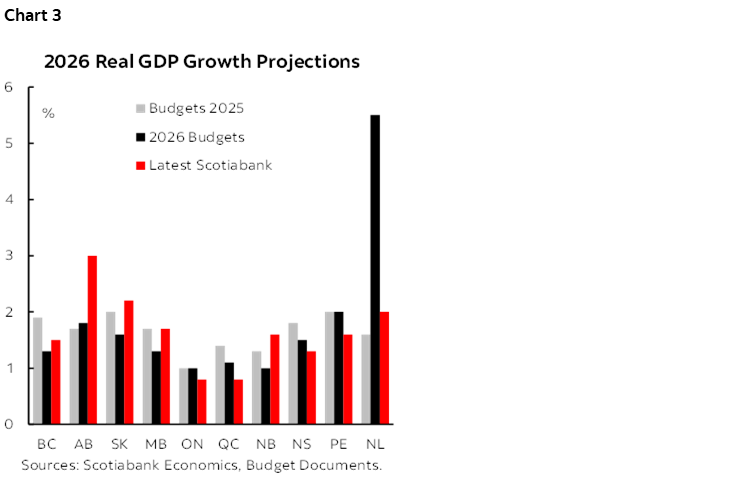

- Aggregate net debt as a share of GDP is projected to increase from 30.6% in FY26 to 32.2% in FY27 (chart 2), with the largest increases expected in British Columbia, Nova Scotia, and Prince Edward Island. Aggregate debt service as a share of revenues will rise from 6.3% to 6.8% in FY26.

- All of Canada continues to face headwinds from the U.S. tariffs and related uncertainty, but perhaps less than at this time last year. In addition, the oil-producing provinces could see their revenues overperform their budget projections, especially Alberta.

- As impacts from the trade war and associated uncertainty gradually subside in the medium term, fiscal outlooks should improve, especially if provinces can deliver on promised spending restraint over the medium-term. However, health care costs continue to climb, challenging provinces’ desires to slow spending growth.

DEFICITS MOSTLY HIGHER AND/OR FOR LONGER

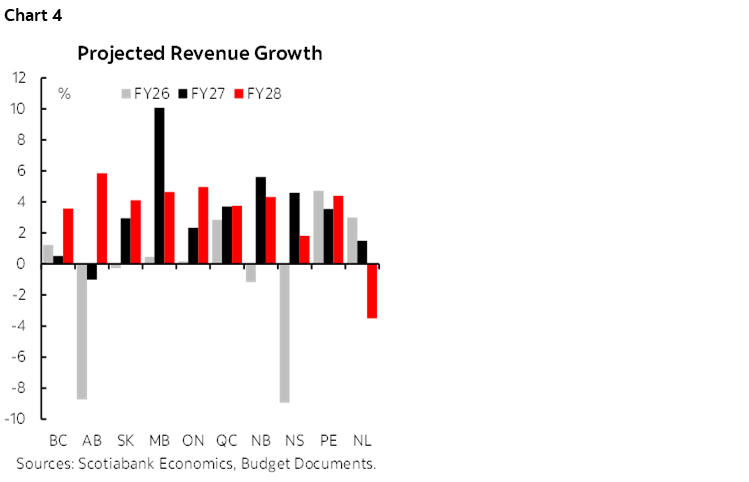

Most provincial governments downgraded their expectations for near-term economic growth (chart 3). While Canada has so far avoided the worst-case scenarios related to trade (e.g., U.S. withdrawal from CUSMA), the U.S. tariffs continue into their second year and are having significant impacts—especially in the sectors facing the Section 232 tariffs (steel and aluminum, autos, forestry, etc.). Many provinces hoped that the trade war would be more short-lived, and therefore have needed to revise somewhat lower their expectations for economic growth this year, compared to their assumptions last year. British Columbia (BC) saw the largest downward revision of 0.6 percentage points, followed by Saskatchewan and Manitoba at 0.4 pp. Newfoundland and Labrador (NL) is the main exception to this, as strong oil production growth helped the province achieve an impressive 3.5% growth last year and has led it to substantially increase its expectations for growth this year. Overall, Central Canada continues to expect to face the brunt of the economic slowdown, anticipating growth of around 1% this year—which is broadly in line with our expectations. Provinces in Western and Atlantic Canada are expecting somewhat higher growth, also broadly in line with our expectations, though we see particular upside risk in Alberta given recent increases in the price of oil.

Some provinces announced new measures to improve affordability, but most were targeted and/or temporary. With the economy continuing to face headwinds from U.S. trade policy, there was limited fiscal space in most provinces to announce new measures. Most wanted to address affordability challenges, but ultimately chose measures that were relatively small in order to minimize the incremental fiscal costs. Manitoba is removing the PST from the (relatively few) remaining taxable grocery items and somewhat increased its homeowners tax credit. Prince Edward Island (PEI) announced a new Essentials Benefit for lower-income residents, replacing its provincial sales tax credit and energy rebate program. Ontario announced the elimination of the HST on new houses, but only for the coming fiscal year. NL was an outlier in announcing a number of permanent tax cuts (most notably a substantial increase to the basic personal exception and a series of cuts to the small business tax rate—both commitments from its recent election campaign) as well as increases to its child and seniors’ benefits.

Several provinces announced tax increases and/or spending cuts in order to improve their fiscal positions. BC increased its lowest tax bracket, expanded the PST to cover certain professional services, and announced a 3.4% reduction of the public sector workforce. Alberta and Saskatchewan committed to review their program spending and identify savings. All three Maritime provinces announced significant spending reduction plans, with Nova Scotia and PEI also increasing some taxes (most notably PEI’s new 20% tax bracket on incomes over $200k). However, Nova Scotia has also walked back some cuts, which will require new savings to be identified in order to stay on track with its fiscal plan.

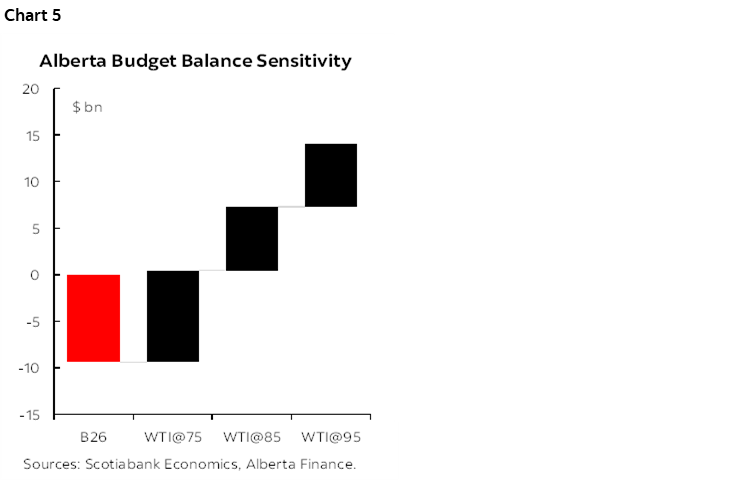

Revenue growth is expected to increase in most provinces (chart 4). For the 2025–26 year, most provinces’ latest estimates anticipate modest or even negative revenue growth compared to the previous year. Alberta is tracking a drop in revenues of more than 8%, mainly driven by lower natural resource revenues, and Nova Scotia is expecting a similar decline—driven by a cut to the HST as well as some normalization from an unusually strong 2024–25. However, most provinces are expecting to see a pick-up in revenue growth in FY27—especially Manitoba, which is forecasting a 10% increase in revenues, driven by higher federal transfers and a return to profitability for the provincial electric utility. Most provinces are also expecting a further revenue pick-up in FY28 and future years, helping deficits gradually shrink. NL is also an outlier here, expecting revenues to fall in FY28, driven by an assumed drop in oil prices.

Revenues in the oil-producing provinces should overperform. The 2026 budgets were released around the beginning of the U.S.-Iran conflict, and as such most provinces assumed oil prices would be lower than we have seen since. While oil prices are likely to drop when the U.S.-Iran conflict ends, prices are likely to remain at least somewhat elevated for some time, given the accumulated impacts on oil production and supply chains. As a result, resources revenues in oil-producing provinces are likely to exceed budget estimates—especially in Alberta, where this year’s projected $9.4 bn deficit could turn into a small surplus if WTI averages $75/bbl for the year (all else equal), or a surplus of nearly $15 bn if prices average $95/bbl (chart 5). Saskatchewan and NL are also in line to benefit from higher oil prices, but not to the same extent as Alberta; these provinces would need WTI to average $95/bbl to see their deficits turn into small surpluses. In addition to oil, prices of many other commodities have increased and should also help boost provincial revenues.

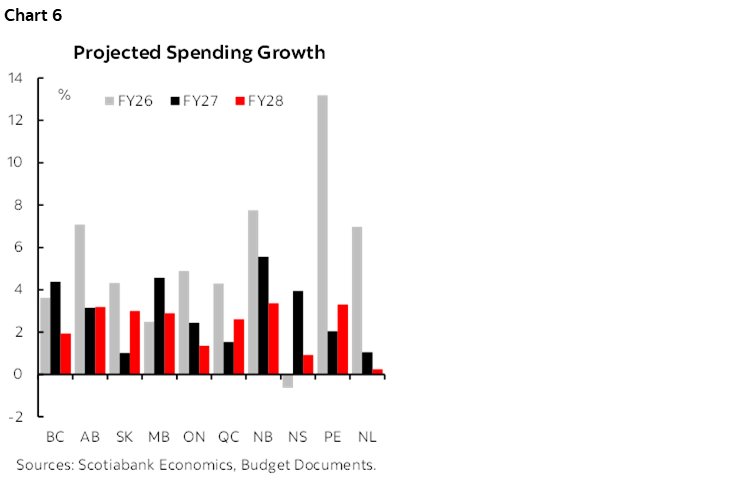

Spending growth is projected to slow (chart 6). As is common, all provinces increased their spending plans for FY26 over the course of the year. PEI is leading the pack, with its updated plan showing 6.4% higher spending compared to its 2025 budget. Most provinces are in the 3–4% range, with Manitoba closest to their Budget 2025 plan at only 1.1% higher. These spending overruns, combined with the initially planned spending growth, have led to high spending growth in some provinces. PEI in particular is tracking 13% higher spending in FY26 compared to the previous year. New Brunswick, NL, and Alberta are also above 6%. Nova Scotia is the lone province tracking year-over-year decline in spending (though it follows a year of a nearly 10% spending increase). Aggregate provincial spending growth is forecast to slow to 2.7% in FY27 and 2.1% in FY28 on aggregate, but with considerable differences across provinces. Saskatchewan and NL are planning to increase spending by only 1% this year, with New Brunswick planning for a further increase of nearly 6%. In all provinces, health care spending growth is a dominant driver.

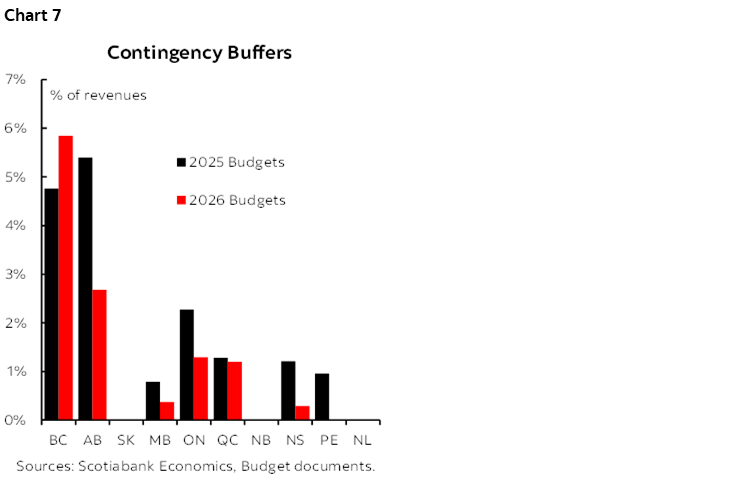

Several provinces have lowered their contingency buffers (chart 7). Many provinces increased (or established for the first time) their contingency buffers last Spring in order to protect against downside economic risks and spending pressures. Alberta and BC set aside the largest amounts, around 5% of revenues. With economic risks somewhat lower, most provinces have reasonably set aside lower amounts this year. BC is the exception, actually increasing its buffers to nearly 6% of revenues. This should help the province beat its deficit projection, assuming revenues roughly meet expectations and spending overruns are limited.

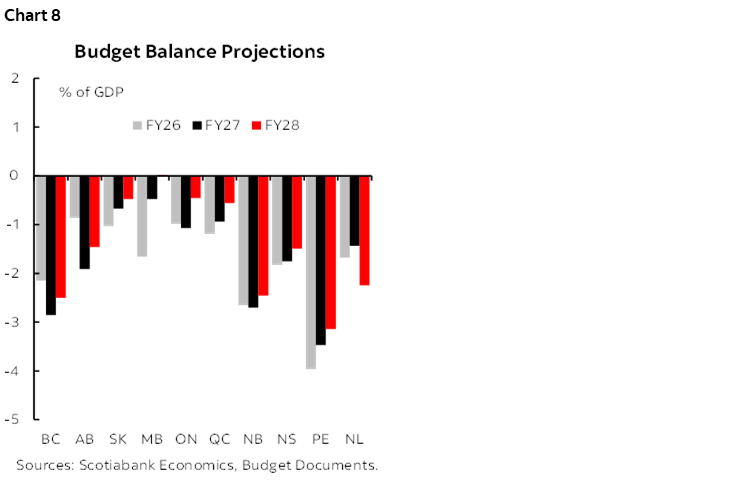

The aggregate provincial balance is expected to drop from -$40.3 bn in FY26 to -$47.8 bn in FY27 before improving to -$34.2 bn in FY28, with all provinces planning for deficits this year (chart 8). While several provinces ran surpluses (Alberta, Nova Scotia) or essentially balanced budgets (Ontario, Saskatchewan, New Brunswick) in FY25, all provinces fell into deficit last year and are projecting to be in deficit again this year. BC and Alberta are projecting increases to their deficits, but could overperform (as discussed above). Most other provinces are projecting slight declines to their deficits as a share of GDP, and most plan to be in the manageable 1–2% of GDP range this year. The provinces projecting larger deficits include PEI (3.5%), BC (2.9%), and New Brunswick (2.7%). On the other side, Manitoba is projecting Canada’s smallest provincial deficit at 0.5% of GDP, and continues to plan for a balanced budget next year.

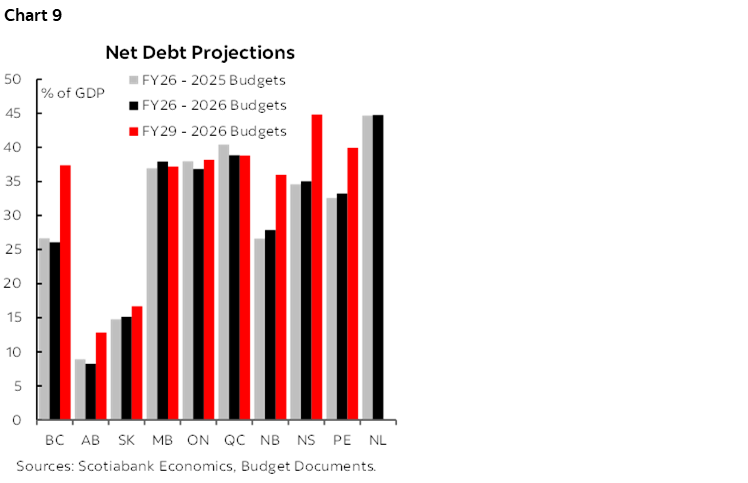

Debt burdens are projected to increase in most provinces (chart 9). Several provinces are seeing their FY26 debt burden estimates decrease over the course of the year, driven by upward revisions to nominal GDP in most provinces, and smaller deficits in some. However, given ongoing deficits and robust capital spending, most provinces are projecting increases in their debt burdens over the coming years. The largest projected increases in debt are by BC, Nova Scotia, New Brunswick, and PEI. NL hasn’t released new debt projections, but its planned deficits will push its debt burden higher as well (from an already-elevated level). Alberta and Saskatchewan have projected smaller increases to their debt burdens, and from a much lower starting level—with higher commodity prices likely to lead to even smaller increases. Quebec, Ontario, and Manitoba are projecting their net debt burdens to remain stable just below 40% of GDP, thanks to shrinking deficits.

Aggregate debt service as a share of revenues is projected to rise from 6.3% in FY26 to 6.8% in FY27. With debt trending higher, and new debt with higher interest rates replacing lower-rate, pandemic-era debt, most provinces are seeing interest charges eat up a larger share of their budgets. NL is already seeing public debt charges take more than 10% of its revenues, and BC is projecting a rise from 6% in FY26 to 9.5% in by FY28. Despite the increase, the aggregate provincial interest bite remains less than half of the peak provincial interest burden experienced in the mid-90s. However, provinces with higher debts leave themselves more exposed to higher interest rates eating up even larger shares of revenues, competing with pressures for health care and other program spending.

Provincial borrowing is projected to remain elevated (table 1). After a 26% increase in FY25, provincial borrowing increased another 12% in FY26—in part because of significant pre-borrowing for FY27. Provincial issuance for FY27 is planned to be somewhat lower than last year, in part due to the significant pre-borrowing—and could be even less than set out in the 2026 budget plans due to the impact that higher oil prices will have on Alberta’s revenues and therefore financing needs. While all provinces don’t release multi-year borrowing requirements, the plans of the largest four provinces indicate that borrowing is likely to remain elevated in the coming years.

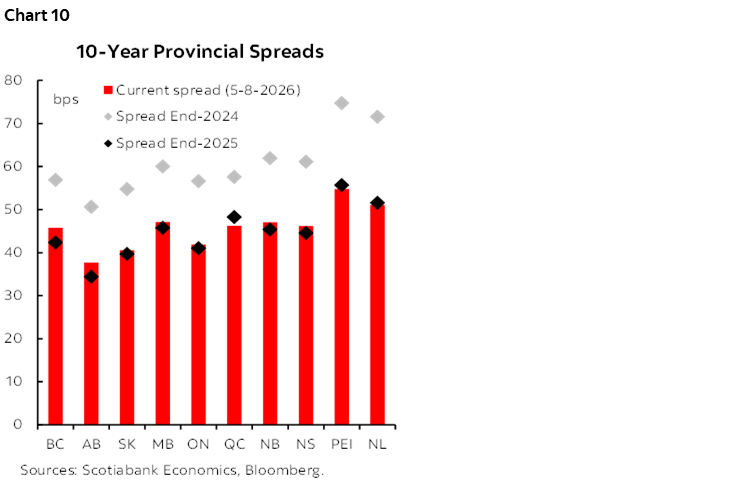

Provincial spreads have gradually trended lower (chart 10). Despite increased supply over the last year, provincial spreads have continued to trend lower, falling 10–20 bps since the end of 2024. BC and Quebec have seen the smallest compression in their spreads, likely reflecting the deterioration in the former’s fiscal outlook and the possibility of a third sovereignty referendum in the latter. Spreads have not changed significantly in the last few months, aside from a slight widening in BC and Alberta’s spreads, and a slight narrowing of Quebec’s.

Credit ratings have been largely stable. After a spate of provincial credit rate or outlook downgrades last Spring, further changes have been limited to BC, which saw a further downgrade this Spring from all four major credit rating agencies. Markets don’t seem to be pricing in any further provincial downgrades at this time, with all provinces trading roughly in line with their current credit ratings—and Alberta bonds trading in line with a higher credit rating, perhaps reflecting the likely fiscal overperformance from the higher oil prices.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.