OIL PRICE GAINS DRIVE FISCAL WINDFALL

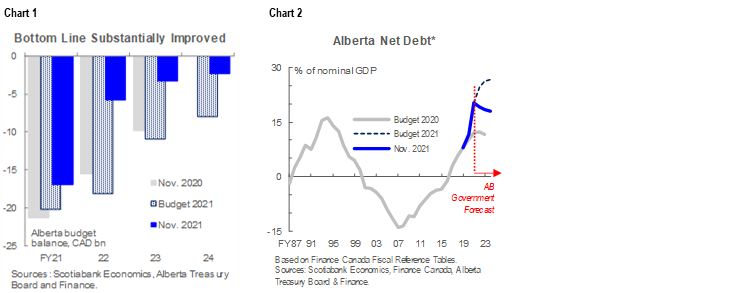

- Budget balance forecasts: -$5.8 bn (-1.7% of nominal GDP) in FY22, -$3.3 bn (-0.8%) in FY23, -$2.2 bn (-0.6%) in FY24, respective anticipated windfalls of $12.3 bn, $7.7 bn, and $5.7 bn versus Budget 2021 (chart 1).

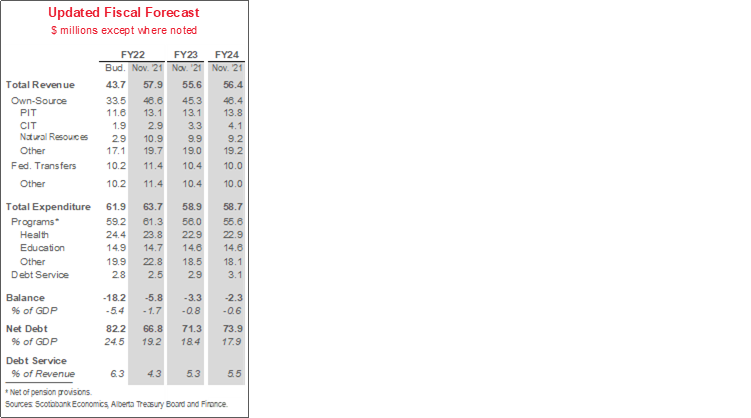

- Net debt: now expected to decline steadily to 17.9% of nominal GDP by FY24, in stark contrast to the climb to almost 27% pencilled in at budget time (chart 2, p.2).

- Economic forecasts: nominal GDP forecast raised from 8.8% to 18.1% (2021) and from 7.5% to 11.5% (2022); WTI price projections lifted by 25 USD/bbl in FY22—now two-thirds complete—and by 9 USD/bbl in FY23.

- Borrowing requirements: $13 bn in FY22, $12.4 bn in FY23, $7.6 bn in FY24; combined FY22–24 projections are $22.7 bn lower than expected in Budget, which mirrors the deficit improvement over that period.

- Capital spending: planned outlays raised by $140 mn versus Budget in FY22, by about $850 mn relative to the previous plan in FY23.

- Update puts Alberta on considerably firmer fiscal footing; while that in part reflects conservative assumptions in the February 2021 budget, it should be well-received by creditors.

OUR TAKE

The Update outlines a massive multi-year revenue windfall that clearly puts Alberta on much firmer financial footing than previously forecast. FY22–24 balance projections were cut by a whopping $25.8 bn, and shortfalls are now expected to tally less than 1% of GDP in FY23 and FY24. Over the next three fiscal years, the province’s debt burden as a share of GDP is expected to be between 5 and 9 ppts lower than budgeted and bend downward. That indicator is on pace to remain well below the 30% upper limit that the government previously targeted; among the provinces that have released updated forecasts, Alberta expects the smallest net debt burden as a share of GDP over FY23–24. Projected debt servicing costs are still on pace to rise as a share of revenue, but hit just 5.5% by FY24.

That windfall was not unexpected given the very conservative oil price assumptions that underpinned the last plan (chart 3, p.2) and the subsequent rise in crude values. Nearly half of the $14.2 bn increase in projected FY22 revenues versus Budget stems from bitumen royalties alone; over FY23–24, that category accounts for more than 60% of the windfall. For calendar years 2022 and 2023, the government assumes WTI prices of 66 USD/bbl and 64 USD/bbl, which are 5 USD/bbl and 4 USD/bbl below the private-sector average, respectively. That profile acknowledges the present risks associated with the omicron variant of COVID-19—which have already driven a selloff of crude—and the potentially dampening impacts of persistent global supply chain-related issues.

Still, the Update is more positive about economic prospects through FY24 and now expects a full recovery of real GDP to pre-pandemic level by mid-2022. That is supported not only by a stronger energy price outlook, but also by an expansion of non-energy investment. The province continues to project a pick-up in population growth following the pandemic-induced slowdown; with continued net interprovincial outflows projected through 2024, immigration is expected to underpin population growth.

Spending restraint still features prominently in the fiscal blueprint, but cuts are scheduled to begin one year later and are now more significant (chart 4). Instead of the 2% and 6.5% reductions in program spending previously planned for FY22 and FY23, respectively, the province plans to increase non-interest expenditures by 6% in FY22, then has built in declines of 9% (FY23) and 1% (FY24). However, the level of planned FY23 program expenditures is about $2 bn higher than forecast in the last pre-COVID-19 fiscal plan. Some of the increases relative to Budget planned for this year relate to the pandemic. Expenses related to Alberta’s severe fourth wave of COVID-19 this summer are expected to erode two-thirds of the $1.25 bn contingency included in Budget. The province also created a $1.4 bn contingency for crop insurance payments in the wake of this summer’s drought.

Alberta’s FY22–24 Capital Plan is now expected to total $21.6 bn, more than $900 mn more than anticipated in Budget 2021. The Capital Plan is the government’s infrastructure spending program that aims to support recovery and long-term development. In FY22, planned outlays increased by $140 mn versus Budget, driven by Federally funded municipal support. In FY23, they were raised by a larger $850 mn relative to February due to some Capital Maintenance and Renewal (CMR) project reprofiling and carry forward. Over the three years, the government allocated another $150 mn to expand broadband internet in rural, remote, and Indigenous communities, $136 mn for the Alberta Petrochemical Incentive Program (APIP), and $190 mn for flood prevention-related projects.

FY22–24 borrowing requirement projections were revised significantly lower than anticipated at Budget time. The government now expects to borrow $13 bn this fiscal year, $12.4 bn in FY23, and $7.6 bn in FY24—reductions of $11.1 bn, $6.3 bn, and $5.2 bn, respectively.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.