HISTORIC DOWNTURN, FISCAL PRESSURES IN WILD ROSE COUNTRY

SUMMARY

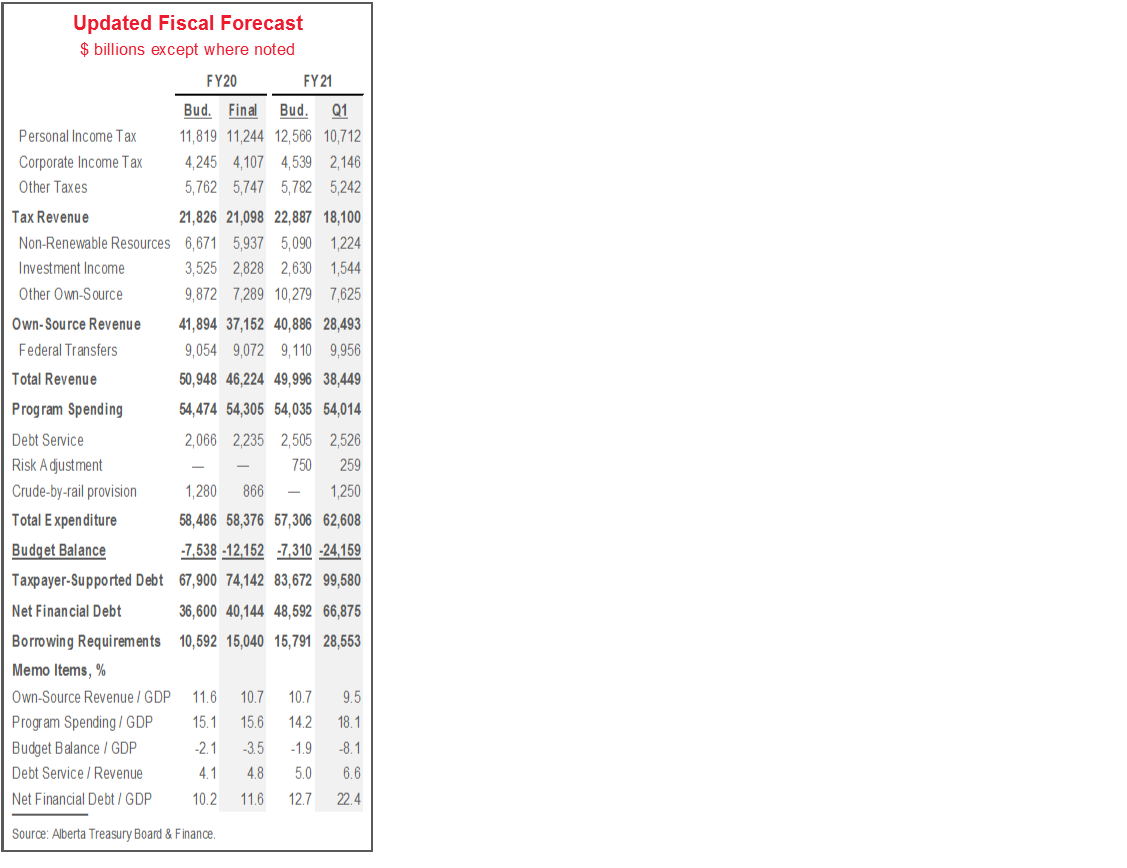

Alberta’s first official update since COVID-19 reached Canadian shores projected a record deficit of more than $24 bn (8.1% of nominal GDP) and a record 22% net debt-to GDP ratio for fiscal year 2020–21 (FY21).

In another sign of the pandemic’s outsized early impact on the resource-intensive economy, deficits and debt loads were also revised higher for FY20—now complete.

Borrowing requirements of $28.6 are penciled in for this fiscal year—$12.8 bn higher than as of the Province’s February budget; FY21 capital expenditures are forecast to reach about $10 bn as already reported.

In our view, Alberta’s ongoing use of fiscal stimulus to support the recovery is necessary given the severity of this downturn, but we await details of medium-term consolidation and diversification plans.

OUR TAKE

Since the onset of the pandemic, Alberta’s economy and finances have been widely forecast to be particularly hard-hit; this update confirms those expectations, and puts the Province on a far more challenging fiscal course. The pre-virus plan for a return to black ink by FY23 was ambitious, and this year’s record fiscal pressures plus the prospect of a gradual oil price recovery will make a return to sustainable public finances over the longer-run even more exigent.

In light of the severity of the current downturn, the government’s ongoing efforts to bolster the recovery are likely necessary. While Alberta’s light COVID-19 caseload has enabled earlier reopening than in many other regions, drilling activity and oil production levels may well take longer to recover in a weak oil pricing environment. And despite the outsized hit to Alberta’s economy and finances, the Province’s still modest debt-to-GDP ratio relative to other jurisdictions leaves some room for economic stimulus.

Ultimately, however, these efforts must be balanced with credible medium-term consolidation plans. For details on this front as well as on the range of economic diversification initiatives announced this summer, we await a fall update.

ECONOMIC CONDITIONS

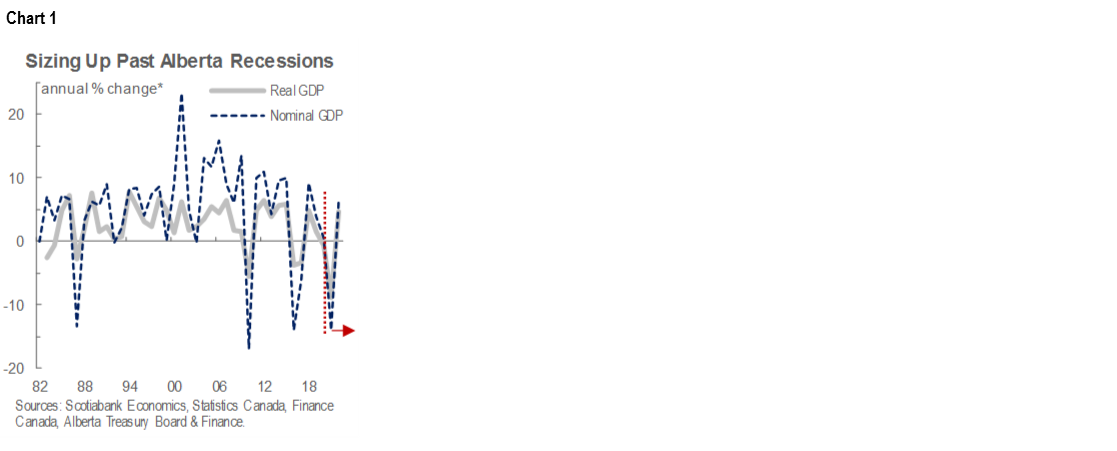

As widely anticipated, 2020 is set to be an historically challenging year for Alberta’s economy. As elsewhere in the world, a near-complete shutdown of the provincial economy to contain the spread of COVID-19 is expected to contribute to historic annual drops in employment (-7%), corporate profits (-73%), and real exports (-13%). Forecasts for WTI and WCS crude prices—under pressure since the virus crippled fuel demand—were both revised roughly $20/bbl lower than anticipated at budget time, in line with our own projections. All told, real GDP is expected to plunge by 8.8% in 2020—the worst annual decline since at least 1982. Nominal GDP is poised to drop 13.9%, the third-steepest ever-recorded drop (chart 1).

The particularly unfortunate timing of this downturn bears repeating. Prior to COVID-19, Alberta had been expected to finally recoup the two-year, 7% output contraction that began in 2015 following the last commodity price crash. That six-year period of convalescence—the longest in the province`s recorded history—will now be extended beyond 2021, with real GDP next year expected to remain more than 6% below its 2014 peak. And the oil and gas sector still faces a range of medium challenges and uncertainties related to egress capacity.

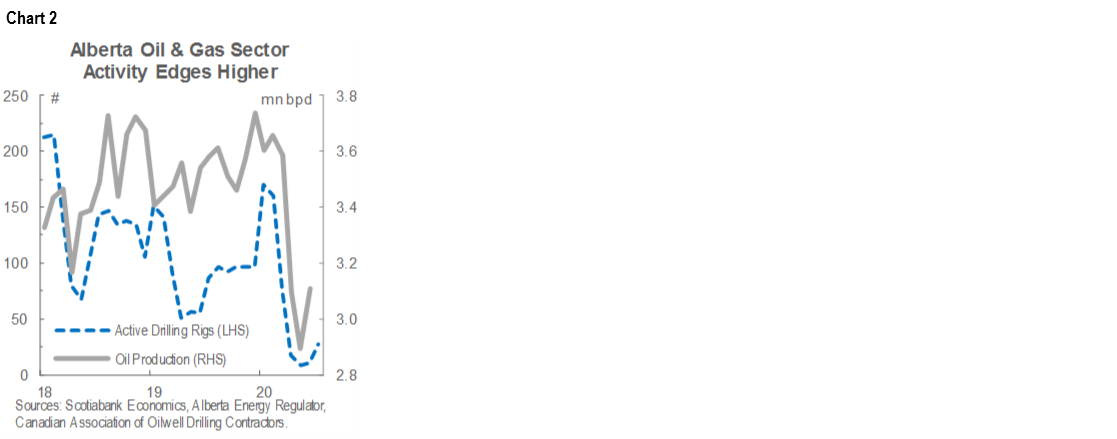

Still, as in many other regions, an economic recovery is beginning to take shape. Alberta-wide retail sales and home purchases in both Calgary and Edmonton rose above February levels as of last month, while provincial automobile sales sat just 5% below pre-virus levels in July. Recent oil price stability also looks to be supporting some improvement in oil production and drilling (chart 2)—albeit from extremely low levels—though Alberta’s full-time employment recovery thus far lags that in most other provinces.

Post-pandemic population growth remains a key question for the outlook in Alberta as elsewhere in Canada. Reflecting travel restrictions and provincial policy changes, population growth is expected to ease below 1% per year by 2021, in contrast to the 1.7–2% gains forecast through 2023 at budget time.

FISCAL DETAILS

As projections for overall economic activity and commodity prices were revised lower than the prior fiscal blueprint, so too were treasury revenues. FY21 government receipts are expected to come in $11.5 bn less than budgeted just six months ago; in line with provincial output revisions, that 16.8% drop would be the steepest since at least FY87. Of the major components of revenue, income tax receipts are forecast to see the largest level decline versus February projections, at $4.2 bn. A nearly as precipitous $3.9 bn (-76%) downward revision to non-renewable resource revenues—which last year contributed almost $10 bn less to the bottom line—underscores the depths of the challenges in the oil and gas sector.

Total expenditures were revised $5.3 bn higher than anticipated in February, and are now on pace to climb by a healthy, but not historic 7.2% in FY21. Recall that Alberta’s pre-pandemic path to balance the books by FY23 was anchored by plans for flat total expenditures beyond FY19. About $3 bn of the FY21 overshoot stems from expenses related to the Province’s COVID-19 and economic recovery supports, which include waiving WCB premiums, re-launch grants to small and medium-sized business, and rent relief. New provisions for exiting the previous administration`s crude-by-rail (CBR) program—reflecting a softer CBR revenue trajectory—are expected to add a further $1.25 bn to the bottom line.

In respect of the severe ongoing economic challenges, Capital Plan expenditures are now expected to total $8.4 bn in FY21. Since scaling back infrastructure outlays in its maiden fiscal plan in 2019, the government has laid out a series of spending increases (chart 3, p.2). The two most recent boosts reflect the severity of COVID-19 downturn, with the largest funding increases since February allocated to the Departments of Municipal Affairs and Housing, and Transportation, reflecting economic stimulus efforts. With the previously announced $1.5 bn investment to accelerate work on the Keystone XL pipeline, the Province has allotted nearly $10 bn to infrastructure in FY21.

Together, changes to revenue and expenditure profiles are expected to widen Alberta’s FY21 deficit to $24.2 bn (8.1% of nominal GDP). That is even wider than the informal projection of $20 bn outlined in June, and would represent the largest fiscal shortfall—in both level and output share terms—since at least FY87. As a portion of nominal GDP, it is also the largest deficit projected by any Province in FY21.

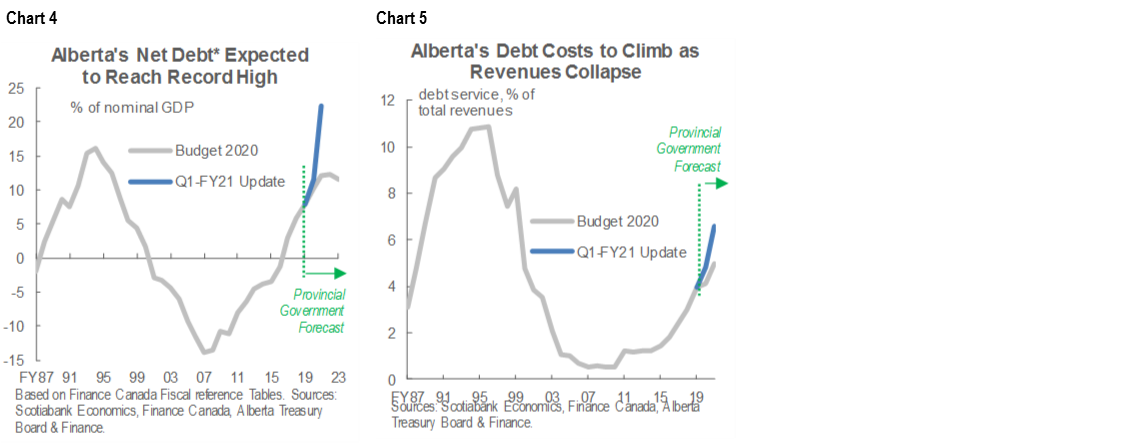

Mirroring the record deficit, Alberta expects to carry a net debt burden of more than 22% of nominal GDP this fiscal year (chart 4). That is almost eight ppts higher than anticipated at budget time, and the heaviest recorded load since at least FY87. Jarring as those figures may seem, however, the Province looks set—for now—to retain one of the most modest such burdens of any jurisdiction in Canada. Only BC and Saskatchewan expect smaller shares this fiscal year. With interest rates on a softer trajectory than in the months leading up to the pandemic, debt servicing cost projections are roughly in line with those from February, though the erosion of government receipts puts them on track to hit 6.6% of revenues—the highest rate in Alberta since FY99 (chart 5).

Also mirroring the deterioration of the Province’s budget balance, forecast borrowing requirements shifted $12.8 bn higher than outlined in February—to $28.6 bn. The government noted that it had already completed a significant portion of that sum late last year and early this year, thereby locking in lower rates than anticipated at budget time.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.