STICKING TO THE PLAN

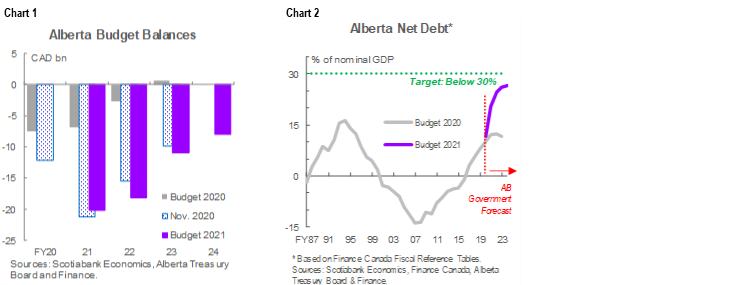

Budget balance forecasts: -$18.2 bn (-5.4% of nominal GDP) in FY22, -$11 bn (-3%) in FY23, -$8 bn (-2%) in FY24, all slightly wider than expected in the November 2020 mid-year fiscal update (chart 1).

Net debt: expected to climb steadily from 24.5% of provincial output in FY22 to 26.6% by FY24 (chart 2).

Real GDP growth: -7.8% in 2020, +4.8% this year, averages 3.4% through 2024; economy expected to return to its pre-pandemic peak in 2022—one year earlier than forecast in November.

Borrowing requirements: $24 bn in FY22, $18.7 bn in FY23, $12.9 bn in FY24; FY22–23 projections are a cumulative $2.6 bn higher than anticipated in the November Update.

Capital spending: edges lower to $8.1 bn in FY22, averages $6.3 bn in FY23–24; FY22–23 total increased by $1.4 bn versus February budget.

Fiscal anchors are unchanged from November. Alberta aims to bring per-capita spending in line with the provincial average and keep net debt-to-GDP ratio below 30%; path to balance to be outlined post- pandemic.

OUR TAKE

Budget stays the course. Anchors outlined late last year—per-capita spending in line with the provincial mean, a net debt-to-GDP ratio below 30%, and a path to balance to be outlined post- pandemic—will continue to guide provincial fiscal policy. Increased expenditures in health care and strategic infrastructure contribute to incremental changes in projected budget balances and debt levels, but are consistent with policy priorities identified by the Province in November.

Despite an improved economic outlook, Alberta continues to face significant challenges. The record output contraction estimated to have occurred last year and second-highest ever recorded deficit in FY21 speak to the outsized impact of the pandemic and related energy price plunge on the province’s economy. Sizeable deficits remain on the horizon and the forecast return to pre-pandemic output levels remains at least a year away. In the base case scenario, finally recouping the losses incurred since the commodity price plunge that began in 2014 would still take place in 2023 (chart 3).

However, conservative oil price assumptions leave considerable upside potential for provincial economic growth and budget balances. At the time of the last update, the key WTI benchmark was hovering near 45 USD/bbl; it has since climbed by almost 20 USD (read our analysis here), but the projections underlying Budget are virtually unchanged from November (chart 4, p.2). FY22–23 revenue projections are likewise very close to November forecasts. This is prudent planning given the extent to which price volatility has upended Alberta’s heavily energy-oriented revenue base in the past, but should a stronger-than-anticipated recovery materialize, the use of any windfalls must be deliberately and methodically considered.

Spending control continues to underpin financial planning, but the deepest cuts have been delayed. The previous update increased program expenses by more than 7% in FY21, then anticipated reductions of 8% and 1.6% in FY22 and FY23, respectively, as pandemic support was wound down. Budget builds a far more modest 1.6% decrease into FY22, with a 6.5% cut to follow in FY23. Much of the more muted drop penciled in for FY22 reflects new spending to combat COVID-19’s pressures on the health care system. The FY22–23 cuts would not be the largest in Alberta history (chart 5) but will be challenging if price and population gains materialize over the medium-term as anticipated. Any revenue upside could reduce the need for outer-year spending reductions.

Alberta’s fiscal anchors are still appropriate. The 30% upper limit on the debt-to-GDP ratio maintains its pre-pandemic advantage versus other provinces, provides flexibility to address COVID-19-related costs and further bolster the province’s recovery, and also signals discipline to creditors. Aligning per-person spending with the provincial average, though challenging as noted, can generate long-term benefits to the extent that it facilitates more efficient delivery of critical government services as intended. Balancing the books and paying down debt are prudent once the pandemic has passed, as is the Province’s openness to review its revenue structure and tax system once post-COVID-19 fiscal dynamics become clearer.

Economic diversification remains Alberta’s holy grail, but may require a lengthy quest. Ultimately, without further broadening of the revenue base away from natural resources, government balances will continue to fluctuate with commodity cycles. Budget outlines several encouraging initiatives on this front—it allocated $3.1 bn to its economic recovery and a range of sectoral strategies in FY22—but they will take time to bear fruit. These include: attraction and development of skilled workers in the technology industry, strategies to drive investment in the agricultural sector, efforts to reduce the regulatory burden for FinTech startups, and new funding for tourism. The planned $1.7 bn increase in FY22 Capital Plan outlays (chart 6)—concentrated in municipal infrastructure funding—should also support these objectives.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.