PROMISES, PROMISES AND MORE PROMISES

Canada’s Parliament re-convened today with a ceremonial Speech from the Throne delivered by the Governor General.

Canada’s continued response to the COVID-19 pandemic took centre-stage, while providing a lens for a plethora of broader promises: an extension of the wage subsidy, expanded employment insurance, investments in childcare, reaffirmed commitments to universal pharmacare, and green infrastructure investments among many others.

Given the exhaustive list of priorities, this Speech is unlikely to bring the minority government down as it provides plenty of hooks for negotiations in the lead-up to a Fall update where details will be laid out.

It clearly signals more fiscal spending ahead for Canada leaving the question not if but how much. But this was largely channeled ahead, so the market reaction has been muted—or more likely, it is eclipsed by broader US and global developments.

There is little beyond lip service by way of fiscal restraint. This will be left to the Finance Minister to make inevitable trade-offs in her first budget this Fall, particularly as she may need to reserve some firepower for second waves.

NUMBER ONE JOB

Today’s Speech from the Throne delivered by Governor General Julie Payette officially opened the second session of Canada’s 43rd Parliament. These speeches traditionally lay out in broad swathes the key priorities that will guide the sitting government’s policy actions (and fiscal spending) over the course of its mandate. This Speech falls less than a year after Prime Minister Trudeau laid out his last policy agenda following his minority government election win. Parliament has been prorogued for six weeks awaiting a new mandate.

The pandemic was a central theme of the Speech, largely eclipsing any comprehensive economic recovery plan. Only weeks earlier, the Prime Minister had been talking up an “ambitious green recovery” and “bold new solutions” for Canada’s economy. The direction shifted abruptly as Cabinet colleagues met last week to discuss the forward-looking agenda against a backdrop of mounting COVID-19 cases across most of the country. For now, the “number one job” remains the continued battle against the pandemic and supporting those most impacted (chart 1).

Other sweeping promises are made, but with few details by design. A second pillar focuses on supporting people and business through the crisis “as long as it lasts, whatever it takes”. The third pillar reflects a “build back better” agenda including clean growth among others. There is also a fourth broad commitment to “stand up for who we are as Canadians”. A four-part agenda focuses the reader, but has not evidently facilitated the narrowing of priorities as the list is comprehensive.

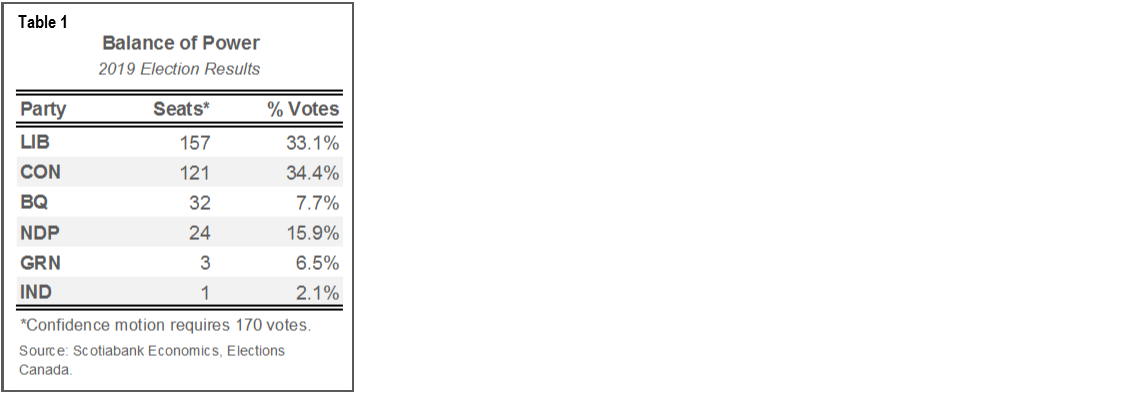

This is unlikely to bring down the government. The party likely holding the sway vote—the NDP—in a vote of confidence had already signalled that it would need to see details fleshed out in a budget to assess the credibility of the promises. They would be hard-pressed to find fault with much of the comprehensive and socially-leaning priorities laid out today. The Conservative and Bloc Québécois parties have already signaled they will not support the Speech but this would be insufficient to tip the vote (table 1).

The clock is ticking for a budget with an update promised this fall. The government has not tabled one since early 2019. Unlike opening Parliaments in normal times where the policy agenda is usually rolled out over subsequent years, all parties will be looking for concrete details on policy plans in the near term. There will be no shortage of funding pressures and the Finance Minister’s job became a little tougher today.

TACKLING THE PANDEMIC

The government has signaled that tackling the pandemic remains at the top of its agenda. The Speech for the most part reemphasises its current strategy, namely supporting vaccine development, ensuring adequate supply of personal protective equipment, and enabling timely testing and contact tracing in order to rapidly isolate localized outbreaks. Central messaging remains that a more “surgical” approach to second waves is preferable to broad-based lockdowns.

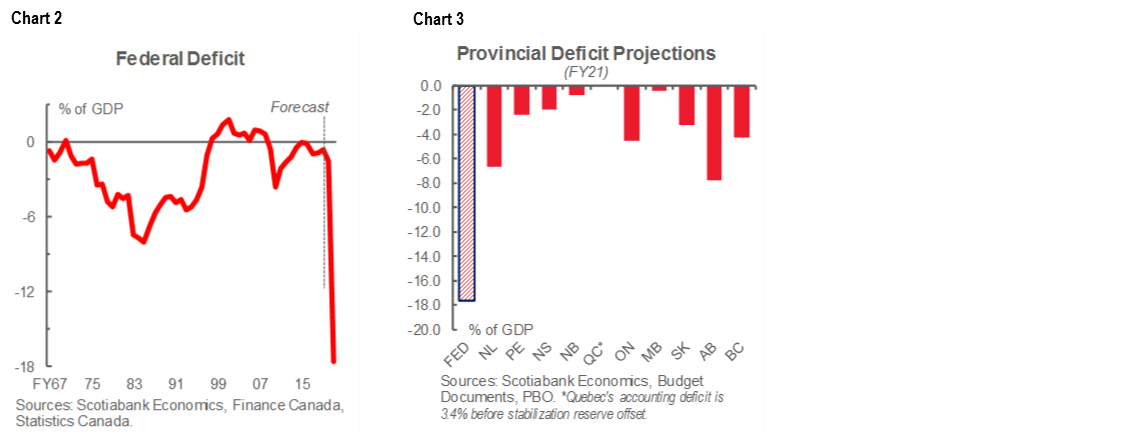

Provinces shoulder the bulk of health-related costs. During the pandemic, the federal government has taken much of the broader pandemic response on its balance sheet with its deficit approaching 18% of GDP—or $380 bn (chart 2). This includes exceptional transfers to provinces, currently totalling $21 bn, largely through the recently-finalised Safe Restart Agreements. Even though provinces face more modest budget shortfalls this year (averaging 3.5% of GDP), they still face collective deficit spending of around $90 bn in FY21 (chart 3) with more upside pressures still on the horizon.

Premiers are pushing for substantial increases to provincial transfers. Last week, Leaders from Alberta, Manitoba, Ontario and Quebec called for a permanent increase in the federal share of health costs to 35%. This would translate into a $28 bn annual increase (and rising) to the Canada Health Transfer which is currently pegged to nominal GDP growth (chart 4). Premiers also outlined changes to the fiscal stabilization fund that would substantially increase compensation to provinces suffering exceptional revenue declines. Under the proposed changes, all provinces would be eligible for compensation and in some cases, substantially more. Premier Kenney, for example, has upped his ask from a pre-pandemic $2.4 bn to $6 bn.

All this to say, the “Team Canada” approach that was celebrated in the Speech likely implies further—and possibly substantial—cost pressures for the federal government. While its default would likely be to provide one-off, exceptional transfers, they will be under pressure to make unconditional structural increases. Time may be on the side of the Feds with transfer negotiations often protracted, multi-year affairs while the Speech provides few hooks to kick-start these talks.

GETTING BACK TO WORK

The Speech underscores the importance of getting Canadians back into the workforce. It pledges to “create 1 million jobs” through a series of initiatives including an extension of the wage subsidy by another six months that could reasonably add another $40 bn to the current program. At the height of shutdowns, unemployment had peaked at 13.7% in May—and would have been closer to 20% if those simply not looking for work were included. Steady gains since then leave aggregate employment at 94% of pre-pandemic levels, though this masks disparities across sectors with some surging above and others such as accommodation and food services still 20% below February levels (chart 5).

The Speech acknowledges reskilling and retraining need to be a part of the policy response in the next phase of the recovery, arguably even more so if second waves further widen the divergence in job recovery across sectors. Given a near-majority of the Canadian workforce worked in sectors deemed ‘difficult’ for physical distancing by Statistics Canada prior to the pandemic, some Canadians could face prolonged unemployment (chart 6). Details on an “historic investment” in job training are left to be seen.

Two competing narratives continue to dominate the job discourse. The dominant one is the unprecedented and unfortunate job losses, while the lesser-appreciated one is the substantial overshoot in government wage replacement. About one-half of Canada’s 19 mn workforce tapped into Canada Emergency Response Benefit (CERB) with $78 bn disbursed to-date. Aggregate transfers to households from the government in the second quarter (i.e., April–June) exceeded aggregate household income losses by about $30 bn (chart 7). Not surprisingly, the household savings rate shot up to 28% from pre-pandemic levels of around 2–3%.

While the Speech does not extend these income supports, there has already been a substantial safeguard baked into the fiscal outlook over the next year. Minister Freeland announced what essentially amounted to an extension of CERB-like benefits for another year in late August. Specifically, the Canada Recovery Benefit (CRB) takes the baton from the CERB where Canadians will see a modest drop in support (from $500/week to $400/week) for up to 26 weeks, but should leave households better off overall as they can earn up to $38.4 k before benefits are clawed back. EI-eligible recipients will also benefit from an equivalent floor on support. Unlike the US, Canadians are not facing a fiscal cliff when it comes to income support in the near-term.

If second waves are effectively managed through more surgical interventions, this should mitigate the massive job losses experienced as a result of the lockdowns under the first wave. The CRB, EI, and a spattering of other safety nets related to caregiving and illness should provide a backstop while, at least in theory, minimising disincentives to work. The temporary changes also give a year’s sightline on support that should help minimize precautionary behaviours that could slow the recovery.

A BIGGER (AND BETTER?) EI DOWN THE ROAD

The Speech flags a forthcoming overhaul to Canada’s employment insurance program. The pandemic laid bare a gap that less than half of Canada’s unemployed are eligible for EI in its dated form. This may disappoint some observers—including the NDP—that were looking for signs of a guaranteed basic income in Canada whereas today’s announcement denotes a reformed program would still retain some form of labour attachment to supports.

There is little light shed on design-specifics which could have big impacts. Any permanent changes to the employment insurance program would need a solid financing plan through a gradual (re-)introduction of premiums as the recovery takes hold and base-broadening to spread these costs across a wider portion of the workforce. The government is rightly buying time to observe behaviours under the temporary CRB: namely, does it encourage a return to the labour force in practice and/or does it dampen demand either through wage pressures or an expectation of increased premiums? It is these details that will determine the medium term fiscal and economic impact of today’s announcement.

BETTER TARGETTING

The Speech promises to support vulnerable Canadians. Specifically, it calls out seniors, racialized Canadians, Indigenous Peoples, youth, frontline workers, disabled Canadians, those with rare diseases, and “moms”. A host of pledges are made including a reformed disability benefit, a renewed commitment to universal pharmacare, a sustained investment in childcare, increased youth work placements, and enhancements to the first-time homebuyer program.

The usual ‘middle class’ mantra has been somewhat toned down but is still present. Recall a series of “middle income” income tax cuts in recent years that benefited the vast majority of Canadians (21 mn Canadians in the last round, according to the PBO). More recently, emergency supports directed at households at the onset of the pandemic were only loosely targeted given the imperative in getting cheques to households. Over three-quarters of the $100+ bn in transfers to households flowed through the CERB versus those with more binding income tests including the CCB, GST, or GIS top-ups (chart 8).

A more ‘surgical’ approach is needed to supporting the most vulnerable Canadians. While overall equality in Canada is comparable to peers (and significantly better that the US) according to the OECD, there are still some gaps in social safety nets that pre-date the pandemic. According to StatsCan, 13% of Canadians reported moderate to severe food insecurity—and a similar number with unmet housing needs— prior to the pandemic. Around one in five Canadians have reported difficulties meeting basic needs during the pandemic, but only about a third was accessing CERB suggesting they had little attachment to the workforce prior to COVID-19. All this to say, broad-based tools would not likely be effective in reaching the most vulnerable.

(IM)POSSIBLE CHOICES

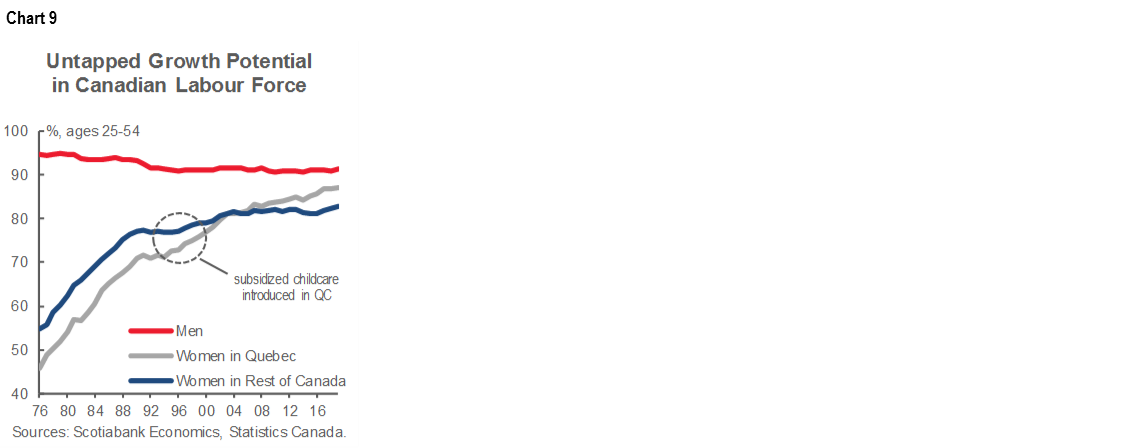

Childcare is a welcomed add-on to the government’s new priorities. Business leaders among others have urged for greater support for childcare in the lead-up to the Speech, reframing the issue through an economic lens. The Quebec experience has demonstrated that universal, low-cost childcare removes a substantial barrier to workforce participation for many women (chart 9), paying economic (and fiscal) dividends. It can also increase household disposable income and indirectly alleviate housing affordability pressures. The IMF has estimated that raising Canada’s female labour force participation to that of male counterparts could increase Canada’s GDP level by 4% over the medium term.

The Speech promises a “significant, long-term, sustained investment” in childcare. An action plan will be developed to this end. But this is not likely to happen in a timely fashion to help those parents—and mothers in particular—make those “impossible choices between kids and career” anytime soon. In the meantime, there are transitional measures the government could introduce to directly support these households while longer term plans are negotiated with provinces as we have outlined here.

A GREEN RESILIENT RECOVERY

Green watchers will have to wait for more details on how the government intends to “exceed” its climate targets. The Speech will legislate an existing commitment to achieve net-zero emissions by 2050 while bringing forward a plan to exceed its 2030 goals. It emphasises win-wins, namely accelerating infrastructure investments towards green building-retrofit, delivering more transit systems, making electric vehicles more affordable and its charging infrastructure accessible, and investing in low-carbon technologies. None of this is new though and Canadians will have to wait for a comprehensive plan.

But this space does hold promise (and a price tag). A prominent group of stakeholders under the Task Force For a Resilient Recovery recently priced a reasonable set of measures at $55 bn over 5 years, with the bulk of this biased towards infrastructure-type investments. (To put this in perspective, the Liberals had campaigned on a $1bn per year green plan in 2019.) Public infrastructure funds are notoriously slow out the door, while an exceptionally hot recovery in construction activity may constrain near-term benefits, but over the medium term such investments could strengthen growth potential.

There are few signals on how the government would mobilize markets towards these goals. This is arguably the missing piece to scaling up government efforts in a sufficiently substantive manner to meet Canada’s ambitious climate targets. Last year’s Expert Panel on Sustainable Finance, led by now-Governor Tiff Macklem, centred its advice on creating the regulatory frameworks and policy incentives with limited public funds to scale up private investment. It challenged Canada to set a global standard for transition-oriented financing, in particular, recognising Canada’s unique economic make-up, while positioning Canada’s energy industry to capitalize on a low-emissions, globally competitive future. The Speech parks these reasonable recommendations for another day.

It is not only a political imperative, but an economic one also, that an eventual green plan adequately addresses transition issues. A comprehensive response is needed that not only reduces emissions, but also supports industries affected on the path to lower emissions. The Speech reinforces support to affected workforces and provinces but stops short of actually using the word “oil”. Canada’s energy sector has been hit by successive oil price shocks that pre-date the pandemic. Uncertainty—on top of dampened demand—has eroded investment substantially in these regions. This will take a toll on Canada’s overall economic output (and consequently its ability to re-invest towards green(er) goals if a unifying and credible vision is not set out.

ADDING IT ALL UP

There is not yet a price tag on promises, but further spending is clearly signaled. The list of measures is exhaustive: wage subsidy extensions, reformed EI, pharmacare, childcare, green infrastructure investments...items that alone each come with annual estimates potentially in double-digits (of billions). Though realistically, many of these big items such as childcare, long-term care, pharmacare and training will require agreements with provinces that are far from certain so many are still aspirational. This year’s federal deficit is already approaching $400 bn. Next year, the starting number is likely around $125 bn (or 6% of GDP) before adding any further spending. Necessary trade-offs against today’s competing priorities are put off to another (budget) day.

The government is still testing waters with respect to its perceived ‘fiscal headroom’—or how much more it can spend before markets start to question the sustainability of all this borrowing. There is no general consensus on such thresholds: advanced economies are generally afforded higher limits, while those with strong governance and policy frameworks (and substantial assets against liabilities) can borrow further at lower premiums. Canada’s federal government boasts all of these advantages, in addition to offering a positive yield pick-up. It should still have among the lowest net debt levels among the G7 even if it undertakes additional spending as countries around the world are unleashing comparable spending.

But composition matters as the government pieces together its next budget. Measures that boost growth potential over the medium term can expand its fiscal headroom, while also strengthening the attractiveness of Buy Canada. But the Speech offers no real ambition on this front with little that will tackle some intractable challenges in Canada such as waning productivity (and you cannot tax your way to stronger growth). On the other hand, measures that create on-going funding pressures with no revenue offsets may raise concerns about long term sustainability and/or may dampen demand in anticipation of aggressive future fiscal consolidation. Some of this headroom may yet be needed should second waves evade management or if a vaccine takes longer than anticipated.

The government pledges “prudence” for now. The Speech stops shy of imposing any sort of fiscal anchor—not surprisingly as this is the bailiwick of the Finance Minister—despite mounting calls for one. Recall, the Liberals’ earlier anchor had been to maintain net debt on a downward trajectory as a share of the economy at a time when debt hovered just above 30% of GDP. In early July, it was forecast to reach 49% in FY21 (chart 10) and could reasonably be expected to approach 60% by next year with potential new spending. A self-imposed constraint by way of a fiscal anchor could counter-balance any further spending increases. This shop has suggested a reasonable approach would be setting an upper limit on net debt-to-GDP of 65% over the next 2 or 3 years with a legislated commitment to bring down the debt-to-GDP ratio every year beyond that, barring a substantial economic shock.

MARKETS PREOCCUPIED ELSEWHERE

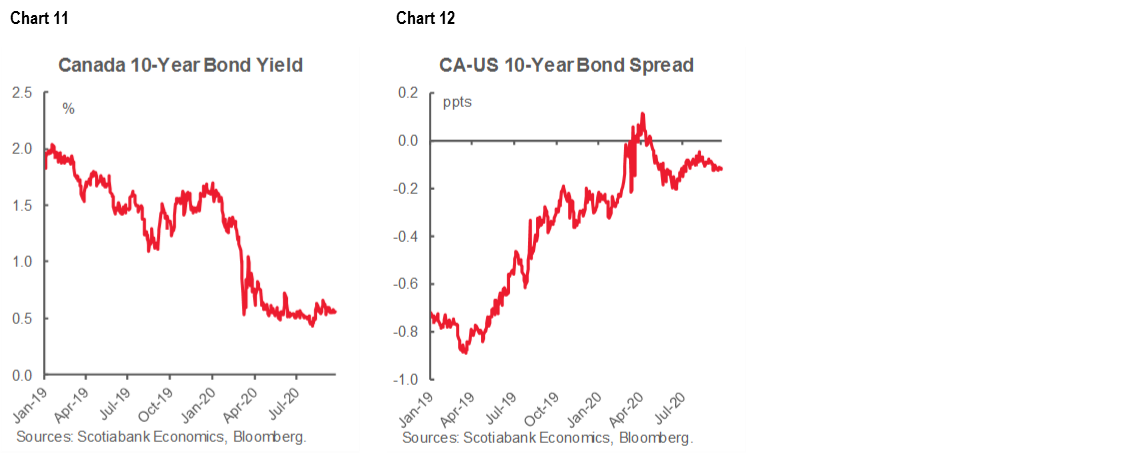

The Speech should not materially affect markets. There has been little evidence of sell-off in Canadian bond or currency markets in the immediate aftermath related to Canadian developments. Greater fiscal activism had been projected by the government in the weeks leading up to the event which likely contributed to a renewed downward trend in yields and a modest widening of spreads against the US (charts 11 & 12). An absence of concrete details today has also likely moderated any reaction as markets have tended to shift only in response to substantive policy announcements, while policy signaling has had no discernable impact beyond reinforcing the directional trend. Equally important, results are digested into the same global markets that are processing resurging COVID-19 cases around the world, US Fed talk on waning fiscal hopes, heightened US election risk, and renewed Brexit uncertainty.

However, this could change in the lead-up to the next budget particularly if spending signals grow stronger against fading messages of constraint. This is not our baseline, but the minority government context introduces a degree of fiscal uncertainty with the balance of power leaning towards further spending. In any case, markets could guardedly position for an election risk post-budget, particularly if a few more elections at home and abroad prove a pandemic popularity bump is universal. On the other hand, Canada’s ability to effectively manage a second wave of the pandemic while avoiding election turmoil could be sufficient to give it a relative leg up.

In short, it could take a while for the fuller effects of this Speech to be priced in, and implications will likely only be known once a budget is tabled. The same can be said for the political ramifications of the new policy agenda set forth today.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.