As the Prime Minister is set to lay out an “ambitious” economic recovery plan this Fall, early signals suggest this will come with a potentially big price tag.

With a clear intent to spend, this could be an opportune time to address two longstanding challenges to prosperity in Canada: low female labour force participation and weak investment and productivity.

We propose substantial increases to household transfers linked explicitly to childcare expenses along with a large increase in tax credits for early childhood education, to remove a substantial barrier to greater female workforce participation. These could be delivered through existing programs, notably the Canada Child Benefit and the Canada Childcare Tax Credit.

We also propose a temporary 25%-matching grant for investment in machinery, equipment and intellectual property to spur additional outlays during the recovery phase as uncertainty may continue to weigh on activity.

These investments would be costly—in the range of $40–65 billion combined—to make a dent in the gaps, but should lift Canada’s growth potential and thus strengthen government revenues over time.

Canada’s net debt would still rank among the lowest in G7 countries, while low interest rates offer an opportunity to undertake such investments.

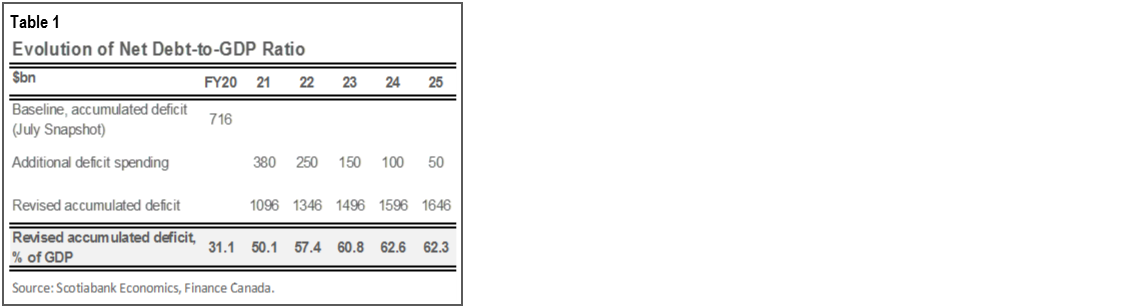

However, a fiscal anchor will be an important signal of discipline and responsibility. We propose setting an upper limit on net debt-to-GDP of 65% over the next 2 or 3 years with a legislated commitment to bring down the debt-to-GDP ratio every year beyond that, barring a substantial economic shock.

BUILDING BACK BETTER

The Trudeau government is considering a range of economic measures to “Build back better” in the context of their upcoming Speech from the Throne and Budget. Raising potential output should be high on their list of priorities. The Government should think big in addressing two of the key challenges to long-term prosperity in Canada: low labour force participation rates for women, and low investment and productivity. With interest rates expected to remain low for the foreseeable future and the likely need for policy support to help our economy manage the post-COVID transition across a number of dimensions, a set of economic policies squarely designed to address two of our greatest economic challenges and opportunities seems appropriate, even as the deficit is rising in an historic manner this year.

There are a number of low-hanging fruits to increasing prosperity which governments have avoided tackling with full seriousness. The full liberalization of interprovincial trade, a wholesale reform of the tax system, measures to deal with housing affordability, and initiatives to increase equality of opportunity for Canadians are but a few of a myriad of reforms that have long been discussed. This note does not focus directly on these very important issues.

This note focuses on two conceptually simple interventions, which, in our view, have the potential to fundamentally reshape our growth prospects by removing impediments to work and strengthening business investment: a heavily subsidized national childcare program and a time-limited matching grant from the federal government for firms investing in machinery, equipment and intellectual property.

MAXIMIZING LABOUR FORCE POTENTIAL

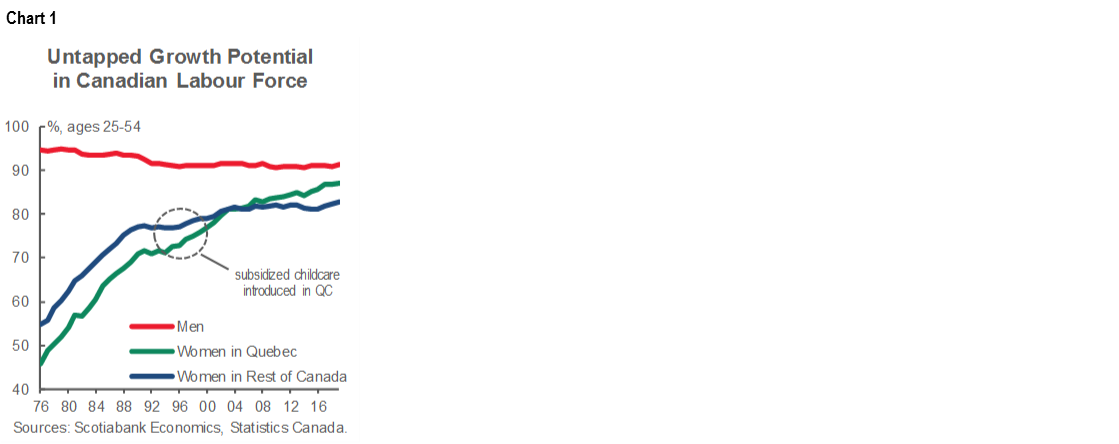

Canada’s labour force could be lifted by more than half a million if women were to match their male counterparts in workforce participation. The participation gap stood at almost 8 ppts (ages 25–54) prior to COVID-19 (chart1). The number is even bigger when pandemic-related declines are included as women dropped out of the workforce disproportionately and have been slower to return. The International Monetary Fund has estimated that closing this gap could lift Canada’s GDP levels by 4% over the medium term, reflecting not only greater supply, but also a productivity boost given higher educational attainment levels of Canadian women relative to men.

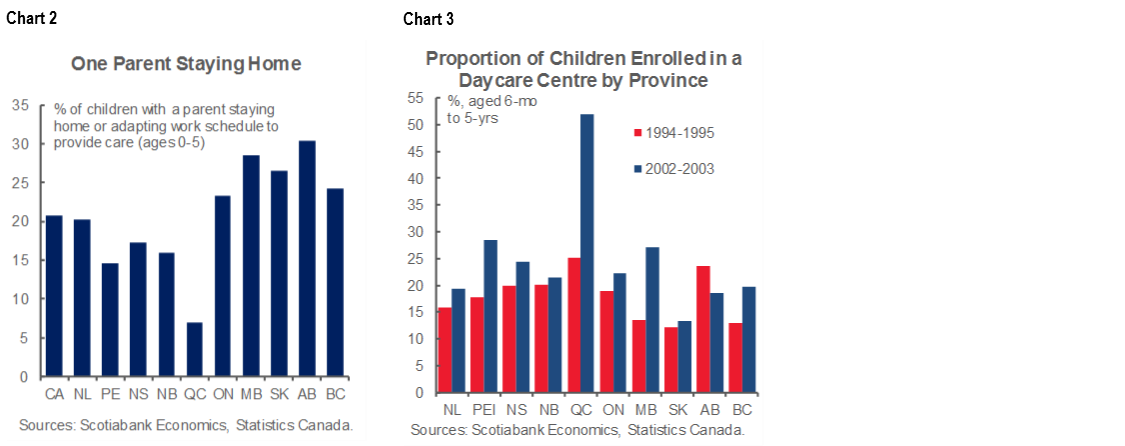

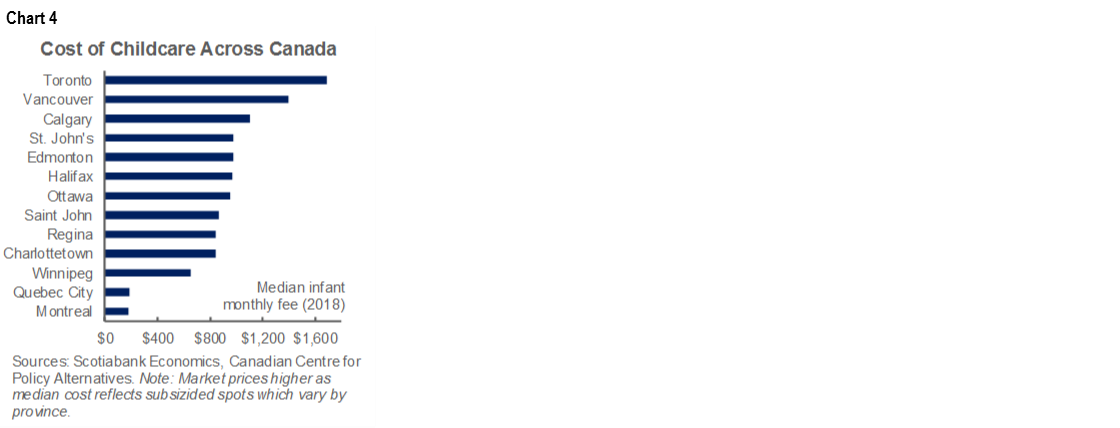

Affordable childcare is a substantial barrier to greater workforce participation for many women. The marginal benefit to working is simply overwhelmed by its cost in most jurisdictions across Canada with many women opting to stay at home (chart 2). Québec is a well-known exception with its introduction of a universal, low-fee childcare program in the mid-90s. Childcare attendance doubled in the aftermath, whereas improvements across the rest of the country were modest (chart 3). This gap persists today with more recent data indicating that almost 80% of Québec children (0–5 yrs) are in childcare versus a rest-of-country average of around 55%. Importantly, Québec has also made substantial progress in narrowing its labour force participation gap whereas the rest of the country has been relatively flat over the last two decades.

Canada could capitalize on today’s fiscal opportunism to make a substantial down payment towards universal access to affordable childcare across the country. Upfront costs would be high, but would pay dividends over time. A subsidy equivalent to Québec (incidentally also around the OECD average at $5k per child) would translate into gross costs of around $11.5 billion per year for Canada’s 2.3 million children between the ages of 0 and 5. However, provinces are already likely spending in the order of $5–6 billion per year on childcare, the bulk of which occurs in Québec. But higher labour force participation fuels higher tax receipts, directly and indirectly. Recall, last year the 400k boost in job growth in Canada drove a $7 billion increase in personal income tax receipts alone.

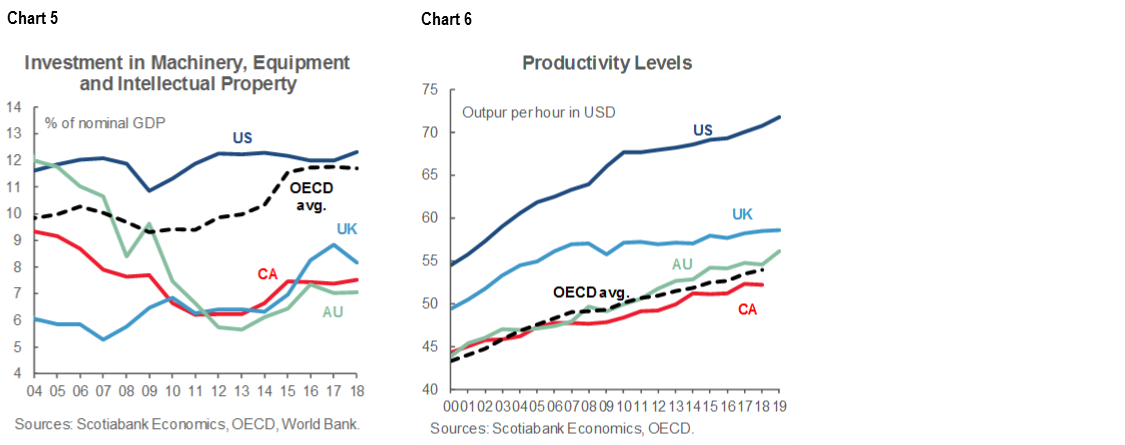

A universal childcare program in Canada will take time but there the Government could take some transitional steps with potentially immediate impacts. More generous transfers to households in support of childcare expenses could both underpin the current recovery while narrowing the participation gap over time. There are a variety of ways this could be delivered but a simple approach would be to top-up the Canada Child Benefit (CCB), but instead of means-testing the increment, make it contingent on a child being in a daycare program. At $5k per child (or roughly $400/mo.), this would still fall short of actual childcare costs in Canada (chart 4), but it would mirror the new Canada Caregiving Benefit, providing women with symmetrical incentives to return to the labour force. The CCB has made important strides in lifting more children out of poverty with substantial costs exceeding $25 billion annually before the pandemic; however, it has not materially improved labour force participation, as there was little change to the uptake of the Canada Childcare Tax Credit (CCTC) which still runs at a cost of less than $1.5 billion annually.

This measure should also be supplemented with a substantial increase to the Canada Childcare Tax Credit. The CCTC currently allows parents to deduct up to $8k a year per child under 7 from taxable income. There is no one-size-fits-all here as childcare costs vary dramatically across cities but increasing the tax credit to $20k a year should cover the cost of daycare in Toronto, for example (which has the highest daycare costs in the country). These combined measures still fall short of a universal, low fee childcare program but they would be substantial first steps in negotiating a pan-Canadian approach with provinces that would address supply constraints to affordable childcare options. Moreover, increasing female participation in the labour force by lowering out-of-pocket childcare costs will increase disposable income and indirectly increase housing affordability.

BOOSTING PRODUCTIVITY THROUGH GREATER INVESTMENT

Canada has long had a productivity and business investment challenge. Productivity lags that of our peers, and investment in machinery, equipment and intellectual property badly trails that of the United States (chart 5), for example. Attempts to encourage investment through tax changes and a range of general and targeted measures to raise business investment have hardly registered at the macro level. The same is true on the productivity side where—despite years of attempts to reduce the barriers to productivity growth—we remain international laggards (chart 6). Both challenges are of course inter-related: low investment leads to disappointing productivity growth. It is not clear what precisely drives under-investment in Canada, though much has been written on potential causes, and much has been tried. But it is clear that low business investment in Canada is a joint responsibility of the business community and various levels of government. There is a role for both sides to build on collaborative efforts to level shift business investment in Canada, one that leverages public finance and allows the private sector to invest in areas they deem most productive.

We propose a very simple approach to kickstart business investment in Canada: establish a time-bound matching grant that would see the Federal Government provide some fraction, say 25%, of the funds deployed by firms as they invest in machinery, equipment and intellectual property. The fraction of the matching grant could be tailored to achieve any number of objectives whether in the context of industrial policy or not. Investments designed to green the economy could receive a higher percentage grant, as could those that are designed to achieve distributional or diversity objectives. Similarly, it could deal more generously with investments by firms that may want to seek to exit one sector for another in light of the economic realities of a post-COVID world. In all cases, we envision a reasonably simple process, akin to the Canada Emergency Wage Subsidy, in which firms submit qualifying investment expenses that are subject to standard CRA verification procedures.

This would be a costly undertaking, one which would have seemed prohibitively expensive in the pre-COVID world. Investment in machinery and equipment and intellectual property has oscillated between $100 and $120 billion annually since 2010. A matching grant of 25% to 50% would therefore cost roughly $25–$50 billion a year. While large, this is substantially less than CERB or CEWS funds paid out this year, for instance, and could easily be financed as these programs roll off. It should also yield significant economic payoffs over time, as the government would only disburse funds if investments are actually undertaken.

A NEW FISCAL DISCIPLINE

These programs would no doubt entail substantial fiscal hits. While there is justifiable concern over the fiscal path at the moment and the evident lack of fiscal anchor, the Federal Government could run up the net debt-to-GDP ratio to the 60–65% range in a few years and still remain among the least indebted G7 countries based on IMF projections for this year’s net-debt in the G7.

There is nevertheless a clear need for a fiscal anchor. There is no hard and fast rule on the optimal level of debt to help guide the government. Prior to COVID, we considered a general commitment to bring down the debt-to-GDP ratio as a sufficient fiscal anchor. That is no longer the case given the deterioration in the fiscal position and this government’s evident intent on spending to Build Back Better. A more concrete fiscal anchor is needed, along with a firm commitment to achieving it. The Conservative proposal to balance the budget over the next 10 years is a start, assuming there is no recession in that period of time.

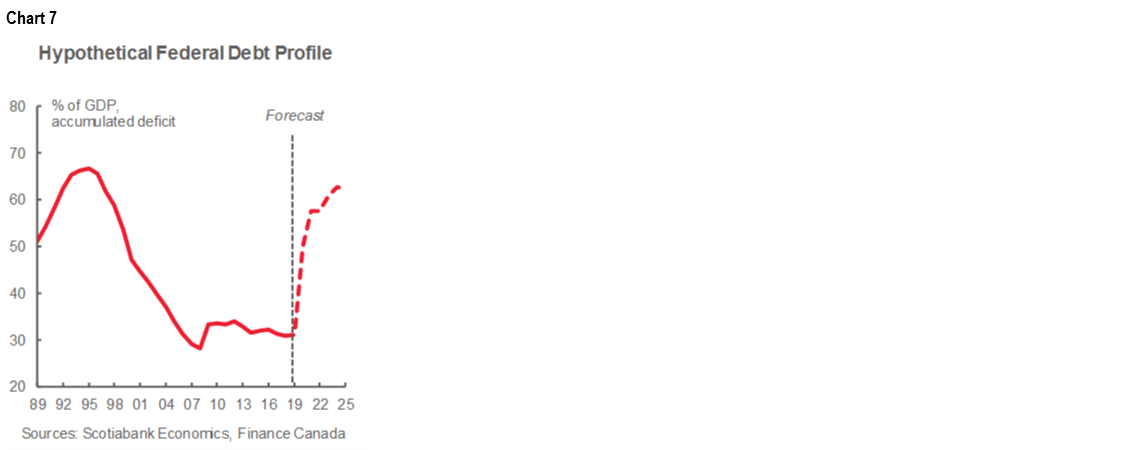

An alternative is to explicitly state a maximum level of debt, say 65%, that would be achieved, the time when this is expected to happen, and commit to a gradual reduction in the debt-GDP ratio thereafter. To strengthen such a commitment, the government could legislate a requirement to achieve this reduction in the debt-to-GDP ratio, but there must be some room to allow the government to respond to future economic recessions. Table 1 lays out a hypothetical path for the deficit and debt under these constraints. This path is not a forecast but, rather, suggestive of the type of deficit that could be realized and its impact on debt accumulation.

A net debt-to-GDP ceiling of 65% clearly contains fiscal room for the policies we propose herein, while still leading to a reduction in debt-to-GDP by fiscal year 2024/25 (chart 7). Debt servicing costs would still be expected to remain low under such a scenario and not lead to the type of fiscal pressure observed when debt-to-GDP in Canada was last at these levels.

(MORE THAN) THE BOTTOM LINE

As the recovery advances, there is an imperative to elevate the debate on the quality of spending, not just the quantum. Programs like the ones we propose are designed to raise Canada’s growth potential and would help bring down debt as a share of the economy even faster over the medium term. Broad-based rescue spending has been essential to averting a worst-case scenario for the Canadian economy in the early phases of the crisis, but now is the time for a more contemplative approach to underpinning the Build Back Better mantra with policies that we know will actually deliver on this ambition.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.