- Justin Trudeau’s Liberal Party secured another minority mandate in Canada’s 44th elections with results nearly identical to 2019 polls.

- The Liberals put forward a largely “stay-the-course” platform with its biggest signature initiative—$30 bn for $10/day childcare—already pledged last April. It proffered up an additional $52.6 bn in net new spending over five years dispersed across a range of initiatives: continued COVID-19 supports, added social spending, housing affordability measures, and climate plans, among others.

- In a minority context, the Liberals would rely on other left-leaning parties—notably the NDP—to maintain confidence in Parliament. This does not substantially change the political dynamics of the past two years, but it puts a shorter shelf-life on the government.

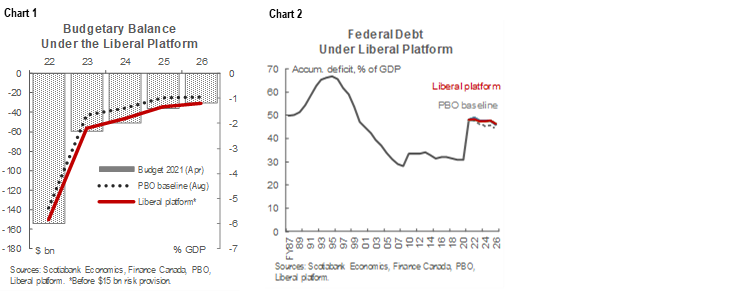

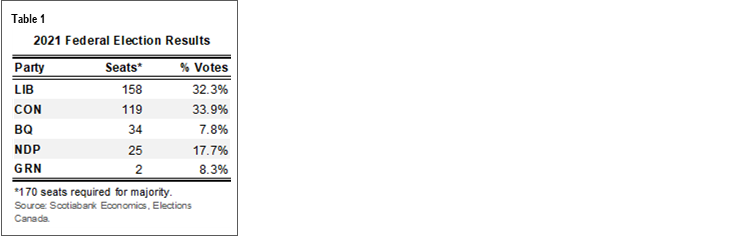

- Deficits would run modestly higher (about 0.5% of GDP added to the bottom line in the next two years, ramping down to an incremental 0.2% by FY26), bringing the budget balance to about -1% of GDP over the horizon (chart 1). This would put debt on a marginally slower downward trajectory as a share of GDP relative to earlier projections (chart 2).

- A degree of fiscal activism has likely already been priced-in by markets, which are expected to shrug off additional modest deficit spending, particularly in the context of global market developments. With election risk behind (for now), markets will likely put sector-specific impacts on their radar as campaign promises are translated into policy.

- Beyond a very modest near-term boost to consumption, broader economic impacts are expected to be minimal. Nevertheless, the added fiscal support would underpin expectations that the Bank of Canada begins tightening its policy rate by the middle of next year.

- The next move is in the hands of the next Finance Minister. Greater clarity on immediate policy intentions and timing would likely be revealed in a late-Fall fiscal statement at which point decisions (ostensibly) would be informed by a few more job and inflation reports.

- More likely, though, it will be left to the central bank to put the brakes on the recovery as it takes stock of additional fiscal measures that materialize over the coming weeks and months against still-elevated price pressures.

DÉJÀ VU

The Liberal Party secured a minority mandate in Canada’s 44th elections on September 20th. In what looked like an easy path to a majority mandate 36 days ago, margins quickly narrowed between the incumbent (the Liberals) and the Conservative Party of Canada with parties polling neck-to-neck on the eve of elections. In the end, the race was not nearly as close, with the Liberals again falling shy of the 170 seats needed to secure a majority in the House (table 1). It garnered 158 seats in the house, only one more than it held under the previous mandate. The Conservative Party will remain in Opposition with 119 seats, though it led in the popular vote. In much the same fashion as the past two years, the Liberals must now build sufficient support among other parties—notably the further-left-leaning New Democratic Party (NDP) with its 25 seats—to maintain confidence of the House.

DIVVYING UP THE PIE

The Liberal Party offered a little bit of something for everyone in its platform. It laid out 100 different spending proposals at a gross cost of $78 bn over five years—or $108 bn once already-pledged funding for $10/day childcare is included. Childcare aside, there was no signature measure under the campaign platform with two-thirds of spending spread across almost 20 initiatives (chart 3). However, clear themes emerged with almost 40% of spending pledges (or $29 bn) targeting social supports, delivered mostly through conditional transfers to provinces related to healthcare, mental health, and long term care. Housing measures captured another 20% of the platform commitments (or $17 bn), followed by government expenditures (at 12% or $9.5 bn) spread across an expansive set of priorities, and targeted household transfers (11% or $8 bn), notably increases to the Guaranteed Income Supplement for seniors as well as student loan provisions (chart 4).

The platform promises to pay, in part, for the new spending by targeted tax measures. Revenue measures would raise $25.5 bn over five years. Roughly half of this would come from efforts by the Canada Revenue Agency to reduce tax gaps—a laudable goal, but one subject to uncertainty. Another 40% of proposed revenues ($10.8 bn) would come from financial institutions through a Canada Recovery Dividend to be developed in consultation with OSFI, as well as 3% surtax on banks and insurers posting profits above $1 bn. A minimum tax rule for top earners is only projected to raise $1.7 bn over five years, and is also subject to revenue risk.

POINTS FOR PREDICTABILITY

Deficits did not sway the vote. The net cost of the Liberal platform came in at $52.6 bn, only marginally higher than Conservative and NDP platforms. The plan front-loads spending, adding about 0.5% of GDP to the budget balance in each of the next two years before slowly tapering down with an incremental 0.2% of GDP added to the bottom line by FY26. Consequently, the budget balance would taper quickly from -6% of GDP in FY22 as temporary measures are unwound to -1% of GDP by FY26. (These figures do not include a $15 bn risk provision set aside for the first three years over the horizon.)

Numbers land almost to a tee on the fiscal path laid out in April’s federal budget. The PBO has since revised its projections based on a stronger economic growth profile with its mid-August baseline projecting an $86 bn improvement over the five-year horizon relative to the budget’s forecasts. Deficit watchers have been able to fairly consistently rely on Trudeau Liberals to prudently provision for fiscal risks, but generally spend windfalls in a practice that predates the pandemic.

Federal debt should (more) gradually decline over the horizon. The federal government’s accumulated deficit stood at 48% of GDP ($1.1 tn) at the end of FY21 with the PBO projecting a gradual wane to 44% of GDP by FY26 absent further policy changes. The Liberal platform sticks to the party’s go-to fiscal anchor since 2015: keeping debt on a modestly downward trajectory as a share of GDP (never mind that the starting point is now 17 ppts points above pre-pandemic levels).

A minority government context raises spending risks to be monitored. While the NDP’s platform net costing was broadly similar to the Liberals, its gross spending promises were more than double those of the Grits. A flashpoint to compromise could be universal pharmacare, which is costed at $38.8 bn over the horizon and would leave a structural hole of over $11 bn per year by the time it is fully implemented under the NDP’s proposal. The Liberals had promised pharmacare in the 2019 Speech From the Throne, but made no reference to it in this election campaign. Historically, minority governments have been too short-lived to claim that there is evidence of upside spending pressure in a coalition-building context. In the current context, the Liberals have shown a proclivity to readily loosen the purse strings on their own, but it would likely only be in the context of more fiscal space opening up down the road—and potentially on the next campaign trail—that they may act on something like pharmacare.

POLICY PLANS

A Liberal-minority win should translate into largely stay-the-course policies (for better or worse). Continued support for COVID-19 can be expected. The party’s platform pledges to extend the Canada Recovery Hiring Program and provide additional wage and rent support to hard-hit businesses, while it would not be surprising to see employment benefits extended beyond their slated expiration at the end of October amidst fourth waves. Canada has provided among the largest temporary fiscal support in response to the pandemic and that will not likely change in the coming months. Last spring’s federal budget baked in an additional $100 bn in support over three years that has only started to flow.

Housing markets may be stoked at the margins. The platform receives high marks for ambition with its target to build, preserve or repair 1.4 mn homes over the next four years, which is a vast improvement over its National Housing Strategy which vied to build 160 k new homes. But the past few years highlight federal funding alone is insufficient: the strategy was seeded with $40 bn over 10 years in 2017 with funding commitments growing to $70 bn since then but the policy levers to unlock supply sit largely with sub-national levels of government. It is not clear that platform commitments will materially change this gridlock; $4 bn to cities could be a step in the right direction but details will matter. On the contrary, a slew of other measures could fuel housing demand on the margins—including the doubling of the Home Buyers Tax Credit and reducing CMHC mortgage insurance costs by 25%—while foreign-ownership and speculation taxes are unlikely to dampen demand materially.

Climate ambitions offered few surprises on the election trail. The Liberals reaffirmed their reduction targets of net-zero by 2050 and 40–45% emissions reductions by 2030 with carbon taxes carrying the brunt of the effort (topping out at $170 per tonne by 2030 from $40 today). During the campaign, they further elaborated on 5-year targets for the oil and gas sector starting in 2025 that would aim to reduce emissions at a pace and scale to achieve the net-zero objective. The party also promises to eliminate subsidies to oil and gas by 2023, end thermal exports by 2030, achieve a net-zero electricity grid by 2035, and sets aggressive EV sales targets. It couples these aspirations with additional funding for green infrastructure, green-retrofits, clean tech investments and tax incentives. With the NDP, Greens and Bloc Quebecois all supporting aggressive climate action, the Liberals will unlikely face resistance on pushing forward on this front (with perhaps the exception of pipeline politics). At a minimum, election outcomes provide continuity in the policy landscape for businesses—many of which have aggressive climate reduction targets themselves—but there are still looming transition risks related to if and how (quickly) the US carbon reduction plans unfold under President Biden and, here at home, how effective transition supports are at smoothing the (economic and political) impacts on workers and businesses alike.

The platform misses the mark on leveraging Canada’s tax architecture for growth. Liberal rhetoric took a more punitive tone towards business with targeted corporate tax measures as a means to fund additional spending. With any (admittedly little) hope, the new government would come around to calls by the IMF and leading tax experts (and now the Opposition party) to reassess the country’s tax architecture. The large and growing wedge between Canada’s personal and corporate tax regimes, along with an increasingly complex architecture, create incentives for arbitrage. Furthermore, the interplay between the federal, provincial, and municipal tax regimes, as well as an evolving international tax landscape, underscore the criticality of a comprehensive tax review in Canada. A piecemeal approach has a high risk of creating unintended consequences, including undermining stronger growth that could eventually better support redistributive policies.

GROWING PAINS

There was little attempt at pitching a growth agenda on the campaign trail. (To be fair, no party offered up much vision on this front.) The Liberals’ earlier childcare commitment may boost growth over the medium term, but it is still subject to implementation and design risk and does little for parents possibly facing a third year of school interruptions. The jury is still out on whether prolonged COVID-19 supports—either to individuals or through business hiring incentives—will strengthen or impede job recoveries, with the best tool likely being vaccine efforts. Meanwhile, the stark contrast of chronically unemployed Canadians against businesses struggling to hire raises the policy stakes in getting it wrong. There are several research-oriented measures including the establishment of an equivalent to the US DARPA (Defense Advanced Research Projects Agency) with $2 bn in funding, $1 bn in research chairs, and another $1 bn in clean/green tax incentives, but it would be premature to revise up growth potential at this point given scale, time-horizons, and implementation risk.

There could be a small, near-term boost to demand as a result of some targeted transfers to households. The biggest would be the $4.1 bn (over five years) to increase the Guaranteed Income Supplement to seniors, as well as $1.6 bn in various student loan concessions, which would reach households with higher propensities to spend. To put this in perspective, these initiatives combined would be about half the size of transfers through the Canada Child Benefit top-up in 2016 that spurred several quarters of 3–4% q/q (sa) growth in real consumption before petering out. Thus, some transitory demand-driven activity could reasonably be expected though higher inflation would likely erode some of its affordability intentions.

Otherwise, broad fiscal multipliers would be expected to be relatively weak. Recall, social spending—while perhaps merited on other grounds—does little for economic output (at least on time horizons currently measured). Targeted transfers to households—which tend to have higher multipliers—comprise a relatively small share of total pledges. Meanwhile, a more advanced stage of the economic recovery would erode the benefits of additional support by the time it hits the ground. A reasonable range for fiscal multipliers of 0.3–0.5 on the approximate $13 bn in projected spending both this year and next would translate into about 0.15–0.25 ppts over this horizon, potentially closing the output gap earlier than mid-year 2022 as currently expected.

The Canadian economy likely faces a confluence of expansive fiscal policy set against a tightening monetary stance. Consumer prices should be stabilizing—albeit still elevated in the mid- to high-3% range—towards the end of the year, but any surprise otherwise, coupled with additional fiscal spending, would likely force a harder look by the Bank of Canada on its pace of tightening. As a point of reference only, according to Scotiabank Economics modeling by René Lalonde, a one-year hike of the overnight rate by 50 bps would temporarily dampen economic activity by about 0.2 ppts of GDP. Needless to say, expansive fiscal policy could necessitate an offsetting monetary response.

YESTERDAY’S NEWS

The election outcomes alter the composition of federally-driven market risk. Markets may have been guarded against election risk, but another Liberal-minority government offers some continuity in governance...at least for a year (or two?) as Trudeau had implied he may take another run at a majority at some point and, generally speaking, the shelf-life of minority governments in Canada is rarely longer. Some degree of fiscal activism has likely already been priced into Canadian sovereign bonds given the similarity of party platforms, otherwise markets can be expected to take a wait-and-see approach as policies are enacted. The Liberals’ approach to regulated sectors (e.g., banks, insurance, telecoms) could have sectoral consequences and consequently market impacts. Markets may guard against these risks pending further details.

Otherwise, any near-term market impacts from election outcomes will quickly fade against broader global developments. Results will be digested into the same global markets that will be dealing with several state-side developments including Wednesday’s meeting of the Federal Open Market Committee (FOMC), which is expected to offer further clarity on its taper timeline. With Congress returning this week, markets will be looking for progress (or lack thereof) on US debt ceiling negotiations, as well as the potential for additional fiscal stimulus (with USD5 tn on the table). Shifts (even modest) on these fronts would quickly overwhelm any impacts of Canada’s federal elections.

Canada still remains attractive. In a search-for-yield environment, Canadian spreads have remained tight, offering still-positive yields in a market where about USD17 tn in sovereign bonds are trading negative. Central bank interventions continue to drive market rates in Canada marginally below its policy rate, while other market metrics such as repo rates, swap markets, and FX hedging costs point to Canada’s relative attractiveness as elaborated by Derek Holt here.

Canada’s low federal debt should offer some comfort, but arguably poses more down- than up-side risk over the medium term. The IMF projects Canada’s general government net debt (i.e., federal plus subnational debt after netting out assets) to be the lowest among G7 countries at around 37% in 2021, while its general government gross debt would be middle-of-the-pack (charts 5 & 6). Three of the four major rating agencies have recently reaffirmed Canada’s top tier borrowing status contingent on the wind-down of pandemic support and a resumption of trend-growth. Layering on Liberal platform commitments would not substantially change this picture, but spending pressures in a coalition-context and structural pressures over the medium term warrant monitoring.

In markets where relatively matters, actions by other countries may affect Canada’s relative appeal with some countries such as the UK and Switzerland already initiating public discourse on more active fiscal consolidation. Some others could be expected to follow, suggesting a laissez-faire approach may not be sufficient over the medium term, but, politically speaking, it would most likely take another election for Canadian policy to pivot in this regard. So far, voters and markets alike have shrugged off debt-fueled spending around the world. These federal elections underscored few Canadians are presently occupied with concerns over federal debt levels. This may only change if debt charges start ticking up materially higher than currently anticipated under baseline projections (chart 7).

TOMORROW’S NEWS

With a shift from who will govern to how they will govern, markets will refresh their risk radars. A Speech From the Throne could be expected as early as next month, but with all its pomp and circumstance, would not likely offer much more clarity of the policy and fiscal landscape beyond the party platform. A fiscal update would likely follow before winter holidays which should give a clearer line of sight on which policies will be prioritized first and how they will be executed.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.