CERTAINTY OF SPENDING SECURED

- Canada’s federal Finance Minister will table Budget 2024 on April 16th. There should be little fanfare as the big-reveals have been rolled out on a near-daily basis over the past fortnight.

- Announcements to-date amount to $43 bn with major new spending in housing, pharmacare, military, and AI. About 60% (or $26 bn) of this would likely hit the bottom line directly. Allow for a few more surprises on budget day for a reasonable final budgetary toll of about $31 bn over the horizon.

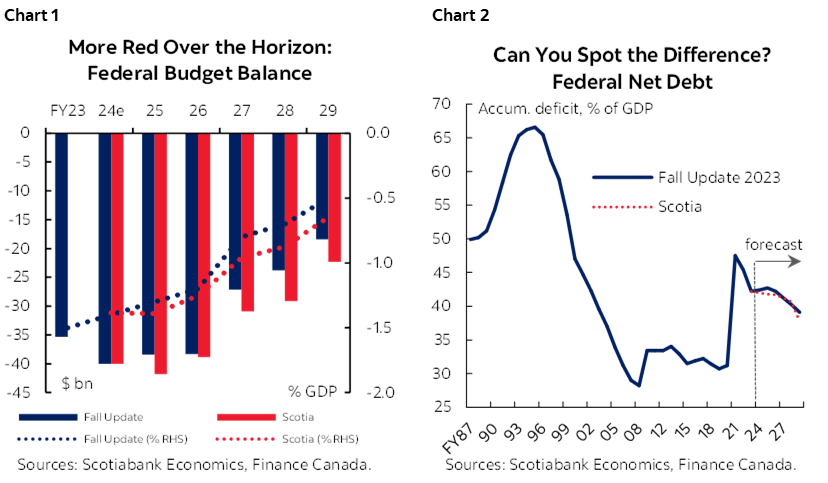

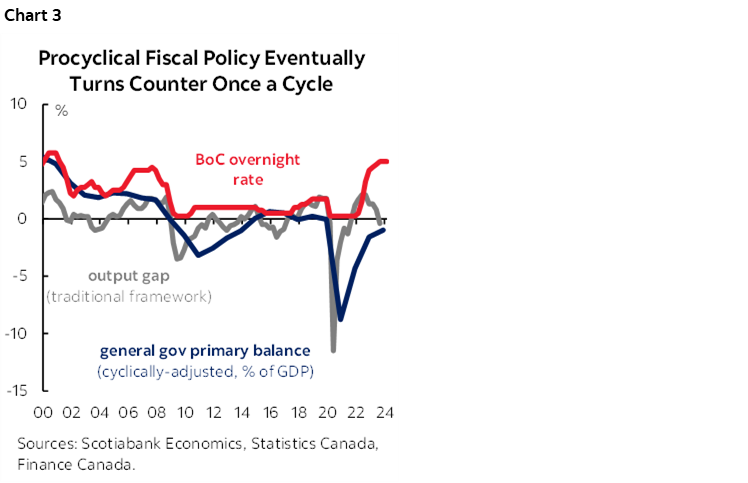

- Modest economic (and revenue) tailwinds in the near-term should partially offset some of the final price tag, while denominator effects should further minimise the impact on the bottom line as a share of GDP. This would yield a marginally higher path for deficits as a share of GDP and only slight GDP-driven differences for the debt profile (charts 1 & 2).

- In isolation, near-term demand measures in the budget are likely to be modest but the cumulative impact of government spending across all levels over time have made the Bank of Canada’s job all the more challenging. Provinces have added another $44 bn in incremental new spending over the next two years alone this budget season.

- This budget won’t likely trigger an election but it is clearly a warm-up lap as Canadians brace for the polls within the next 12–18 months. The taps are unlikely to be turned off any time soon.

- On the margin, this budget will very likely reinforce Scotiabank Economics’ call that it is premature to begin interest rate cuts just yet.

FORWARD GUIDANCE

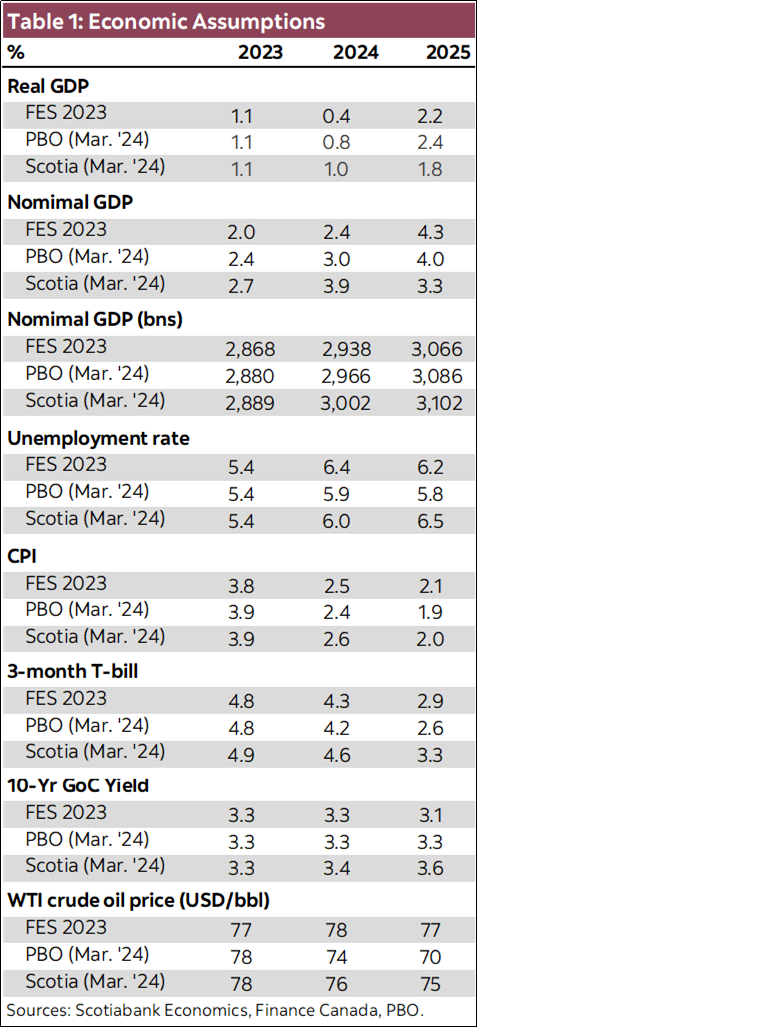

Canada’s federal Finance Minister delivers her annual budget on April 16th. Nominal economic growth has been substantially stronger than the official outlook last Fall but the misses are narrowing. Scotia Economics projects nominal growth 1.5 ppts higher in 2024 relative to the Fall update, albeit with some pull-forward from 2025. The net impact would still see output levels 1.2% higher at the end of 2025. Otherwise, there has been little change to near-term inflation and interest rate outlooks, though long term rate risk may be down-played over a longer horizon (table 1, at the end).

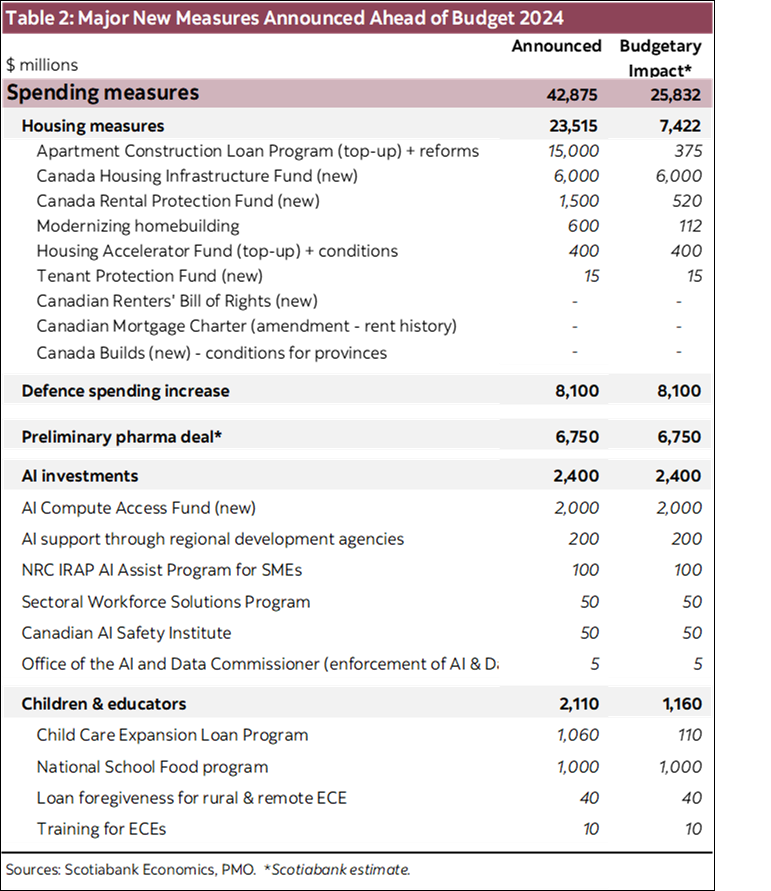

Spending is clearly set to continue. Departing from past years’ practices of “unofficial leaks” ahead of fiscal updates, the Canadian federal government has gone on the offensive with a slew of official announcements across the country in the weeks ahead of this budget. The preliminary tally—we’re still five days out—runs at $43 bn with a lions’ share directed towards housing, along with steps to lock in universal pharmacare, ramped up military spending, and AI investments. (See box 2, at the end for a list of measures announced to-date). Not all of this will impact the budgetary balance, nor will they likely stop there.

A best-guess for the final tally of net new budgetary measures on B-Day is $31 bn. Roughly 60% of already-announced measures (or $26 bn) would likely impact the budgetary balance, while the remainder likely hits only non-budgetary financing requirements (i.e., it matters for bond supply but doesn’t show up on the bottom line). Pencil in another $5 bn between now and 4 pm E.T. on April 16th when the curtain lifts. This is in the ballpark of recent spending packages irrespective of economic or fiscal performance.

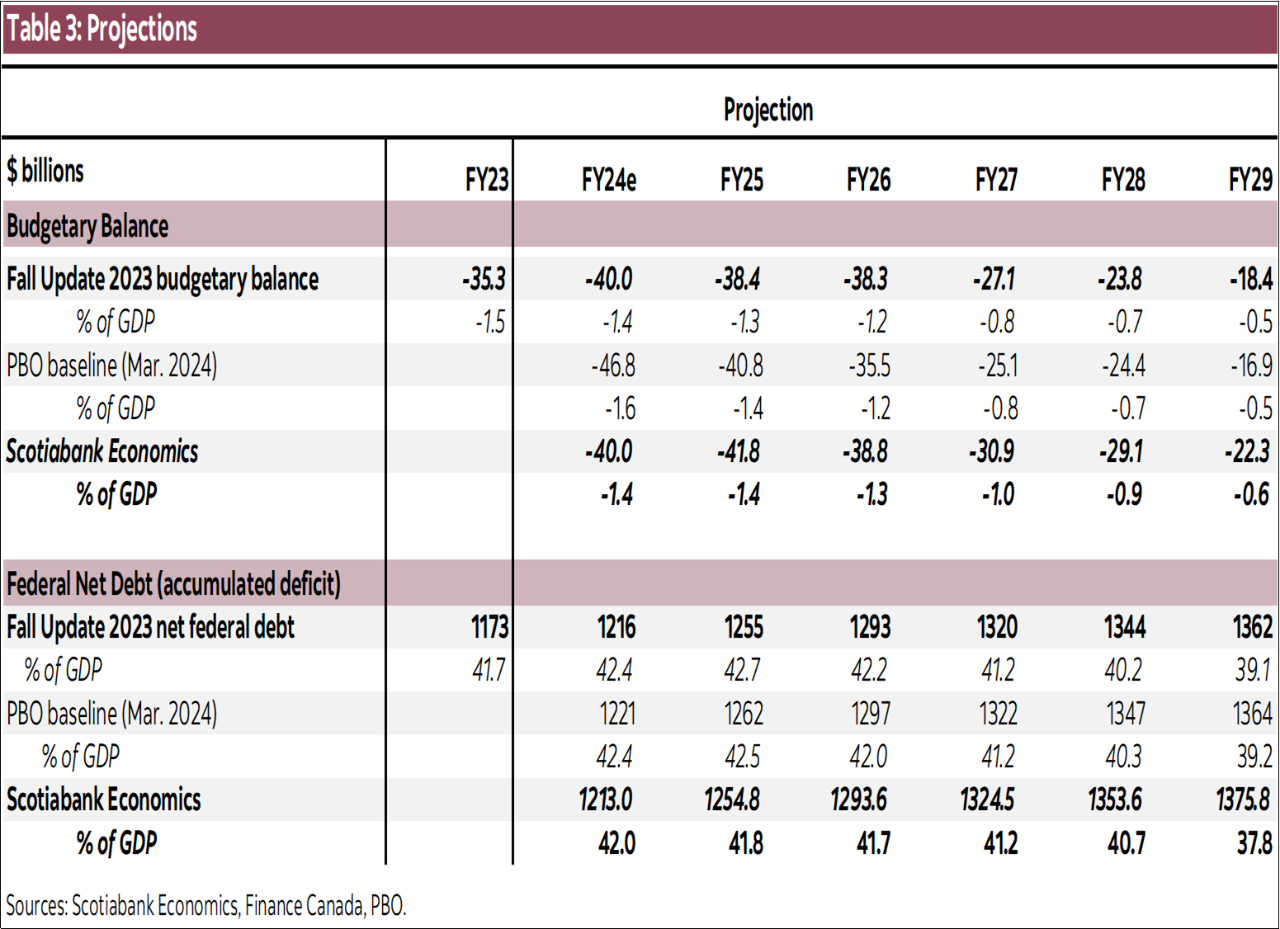

Fiscal trajectories could look broadly similar to paths set out last Fall. An estimated (albeit tenuous) $15 bn in economic and fiscal improvements over this horizon would partially cushion new spending, leaving an incremental budget shortfall of about $14 bn over the planning horizon (through FY29). Meanwhile, stronger-than-anticipated nominal output this year would mostly render marginally higher—but mostly imperceptible—differences to the deficit and debt trajectories as a share of GDP (chart 1 & 2). (Though with stale forecasts and conservative budgeting, they may not book all of this just yet.)

This budget is not expected to trigger an election, but it does appear to be a warm-up lap. With the Liberals trailing in the polls and its alliance with the NDP relatively safe until later next year, neither have an interest to rock the boat just yet. But it does signal continued fiscal ambivalence ahead.

SYSTEM OVERLOAD

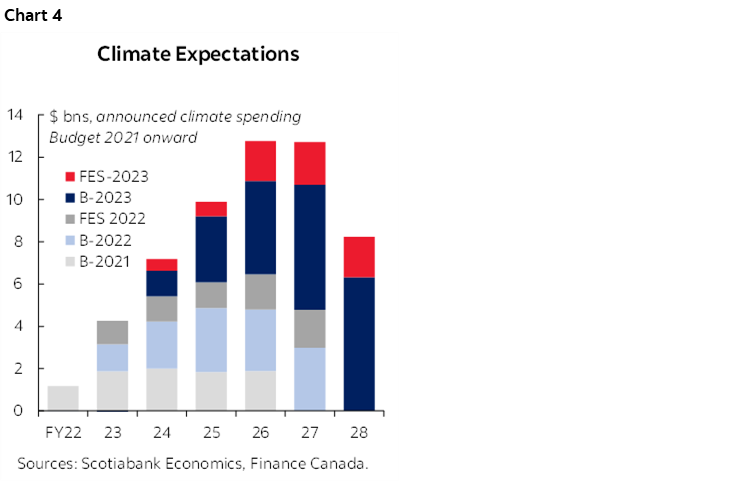

The incremental impact of this budget alone could be fairly modest—in the order of 0.2 ppts of GDP annually—but it is folded into an environment of proliferate fiscal spending over time and across levels of government. Another $5 bn in federal spending this year (i.e., FY25) would top up $23bn in incremental provincial outlays announced in recent weeks (and $21 bn in FY26). It also piles onto the $45 bn and $42 bn in (net) new federal measures for FY25 and FY26, respectively, announced since Budget 2021. The Bank of Canada has revised upward the expected impact of government spending on its growth outlook for 2024 (to 0.7 ppts) against a real GDP outlook of 1.5% before incorporating forthcoming federal actions. It has been explicit that government spending compounds ongoing challenges to bringing inflation (and inflation expectations) on a firm path back to target. Fiscal policy has been running procyclical for over two years now, and while the impulse is decelerating, it is still accommodative (chart 3).

There are a host of laudable policy measures in the pipeline that could start chipping away at structural bottlenecks and/or boost economic potential over the medium term, but there is substantial execution risk. Housing and housing-related infrastructure investments in this budget ($23.5 bn announced with an estimated budgetary impact likely around $7.4 bn)—along with ramped up capital spending across most provinces—are sorely needed, but some provinces are already balking at conditions attached to federal pledges. Labour is also likely a binding constraint to the speed at which housing supply can come online and that limit is likely substantially lower than the shortfalls estimated by CMHC. Policymakers don’t yet appear ready to tackle the thornier issue that housing markets—as structured presently—are likely crowding out other potentially more productive uses of capital.

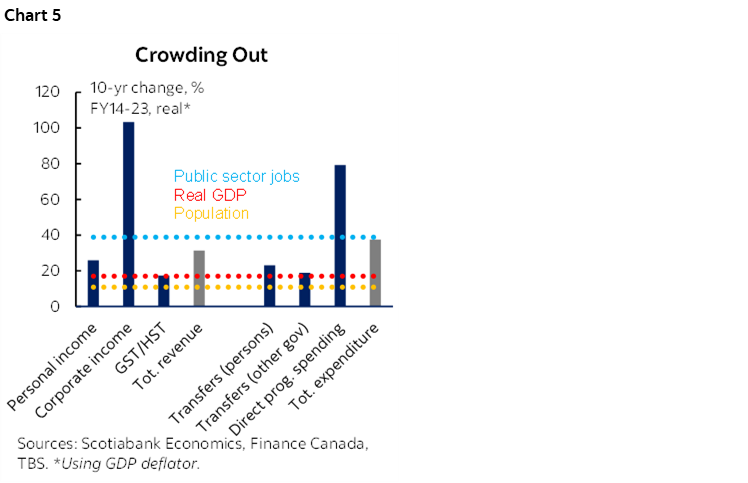

There is also an estimated $16 bn in prior green transition pledges—largely tax credits—to be detailed in or around this budget that rely on private sector uptake. These are part of the $60 bn in transition commitments promised since Budget 2021 (chart 4). Implementation risk is compounded by a host of factors including a bias towards highly prescriptive and carefully circumscribed policy design in Canada compounding the inherent uptake uncertainty of any tax incentives, cut-throat competition from the US for investments, and more generally a highly uncertain geo-political landscape not only south of the border, but domestically as well.

New imbalances are also emerging. The federal government has had to lean heavily on corporate taxes—which have doubled in real terms over the past decade—to offset direct program spending that has shot up 40% (again, real terms) over the same period even as real GDP growth has turned out a mere 17% gain. The public sector footprint has grown with expenditures (chart 5). Operating costs in FY24 were pacing at 3.6% ytd growth through January despite earlier plans for a contraction. As the rest of the economy normalises, the federal government will need to right-size as it butts up against limits to its spend-then-tax approach.

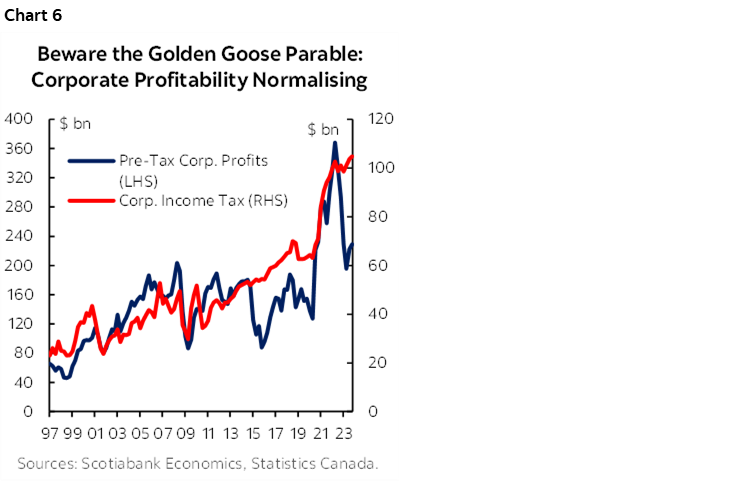

Engines of sustainable sources of growth and productivity—the private sector—are still largely viewed as a means to footing the bill. Corporate profits are rapidly descending back to pre-pandemic trend levels (chart 6), and provincial budgets provided a peak preview of the headwinds for government revenues. Nevertheless, federal ministers have been evasive in recent media scrums when asked about more taxes in the pipeline as rumours of a possible windfall tax circulate.

This budget is not likely to “break the glass” with a comprehensive and coherent growth agenda. A credible productivity agenda would need to put rigorous growth filters across all budgetary decisions. It would need to dig deeper into the base—the ongoing reallocation exercise would amounts to less that 1% of total program expenditures annually—perhaps even a one-time bottom-up budgeting exercise. And it would need to embark on a long-called for comprehensive review of Canada tax structure that would involve provincial and municipal counterparts.

FISCAL ENGINEERING

The government will likely hit its fiscal targets set out last Fall with a bit of curve control. Recall, the Fall update laid out a contortionist set of anchors: the FY24 deficit at or below Budget 2023 projections in dollar terms (e.g., $40.1 bn), a declining deficit as ratio of GDP in FY25 and beyond, and deficits below 1% in FY27 and beyond. It also pledged to lower the FY25 debt ratio relative to the Fall outlook (e.g., 42.7%) and keep it sloping downward thereafter. Our spending guesswork—not incidentally—just adheres to these rules.

The fiscal framework has a bit of wiggle room across years to make the math work. For the FY24 anchor (i.e., ending March 31, 2024), the space looks tight based on balances through January, especially given expenditure over-runs, but there is quite a bit of leeway for reprofiling (with childcare being a likely contender in the near term). Over the horizon, uncertain tax credit timing and uptake, along with a two billion provision for unannounced measures, adds to the flexibility.

Admittedly, our faith that they’ll abide by their fiscal targets in this budget is based less on firm math, more on the disbelief that they’d run the risk of joining the list of basket case countries that blow through fiscal rules in calm times (especially half a year after setting them). There is a reasonable chance that they add on even more new spending than we have assumed, and/or adopt more conservative revenues assumptions over the medium term while announcing new targeted taxation measures to force the math (giving new meaning to fiscal ‘target’).

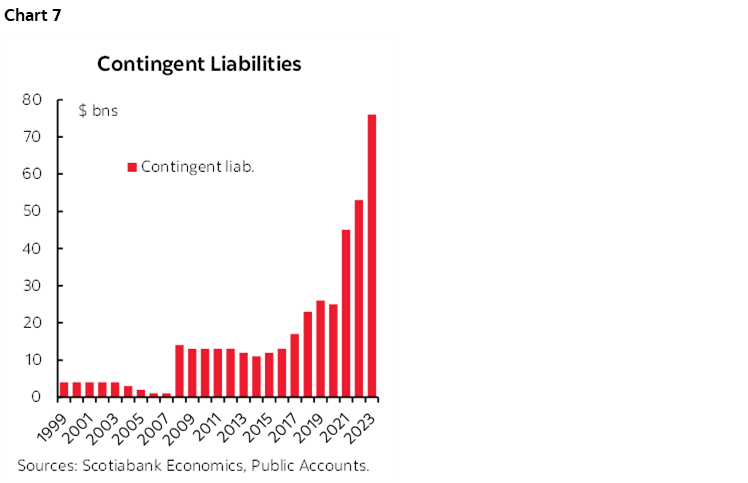

Either way, there is not much headroom to accommodate materially greater spending under these targets over the next few years... but there is no shortage of pressures. It would not take much of a growth shock in 2025 (or an imagination as to the trigger) to breach at least one of these constraints. There are also substantial contingent liabilities ($76 bn in FY23) that will very likely rightly be folded into the balance at some point, notably around Aboriginal settlements (chart 7). Despite tabling legislation for a new disability benefit, numbers have not yet been revealed (factor in a couple billion annually), while a long-promised revamped EI program is still on the watch-list (expect a phase-in). A full-blown pharmacare program is also not yet reflected in the fiscal profile (add another $10 bn annually) but will be punted to election time.

It is reasonable to assume policy (and fiscal) resets at election time (under the current or new government).

MORE THAN MEETS THE EYE

Off-budget items will be an important space to watch (and notoriously difficult to forecast). A sizable chunk of housing measures (we estimate $17 bn) would likely be carried on the non-budgetary side of the ledger. Adjustments to earlier CEBA loan provisions are possible with the repayment deadline past. On the flip side, with the Trans Mountain pipeline expansion complete, this will be a space to watch for signs of divestiture timing. The Fall update had already incorporated a substantial ramp-up in the near-term outlook for non-budgetary financial requirements in the order of $30 bn and more is on the way.

Near-term bond issuance has already been accelerating in recent months. Scotiabank’s Fixed Income expert Roger Quick covers this space comprehensively but a few points of reference could be helpful to anchor potential changes. Last (fiscal) year’s planned bond issuance was $204 bn and came in close to the mark. Quick would easily put another 20–25% increase in supply this year mostly on non-budgetary drivers (with a host of caveats) but notes the pace of issuance had accelerated in the final months to an annualised pace of $244 bn. Markets shouldn’t be surprised when the FY25 borrowing plan is tabled next week though announcements over the past few weeks clearly put upside risk to the supply estimate.

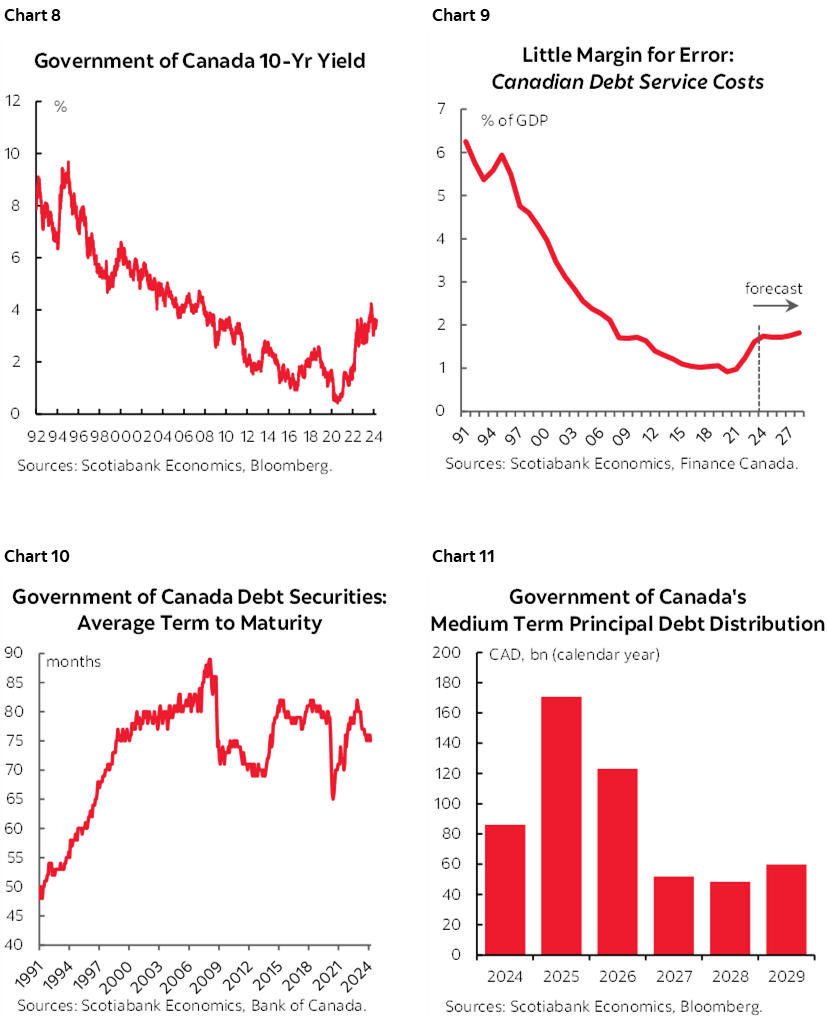

This supply is raised in global markets swayed by bigger players. Others—like Canada—are tethered to these trends with differentials largely determined by policy rate outlooks and to a lesser extent relative growth prospects. Canada’s 10 year bond yield has come down from last year’s peak north of 4%, sitting only modestly above expectations last Fall (chart 8). However, the Fall update projected long term rates returning closer to 3% by next year. Even under that more optimistic scenario, debt servicing—though low by historic standards—was only precariously stable (chart 9). The term structure of outstanding debt has given up some of its earlier gains, and is back below pre-pandemic levels (chart 10). It faces a wall of maturations in 2025 amplifying interest rate risk exposure (chart 11).

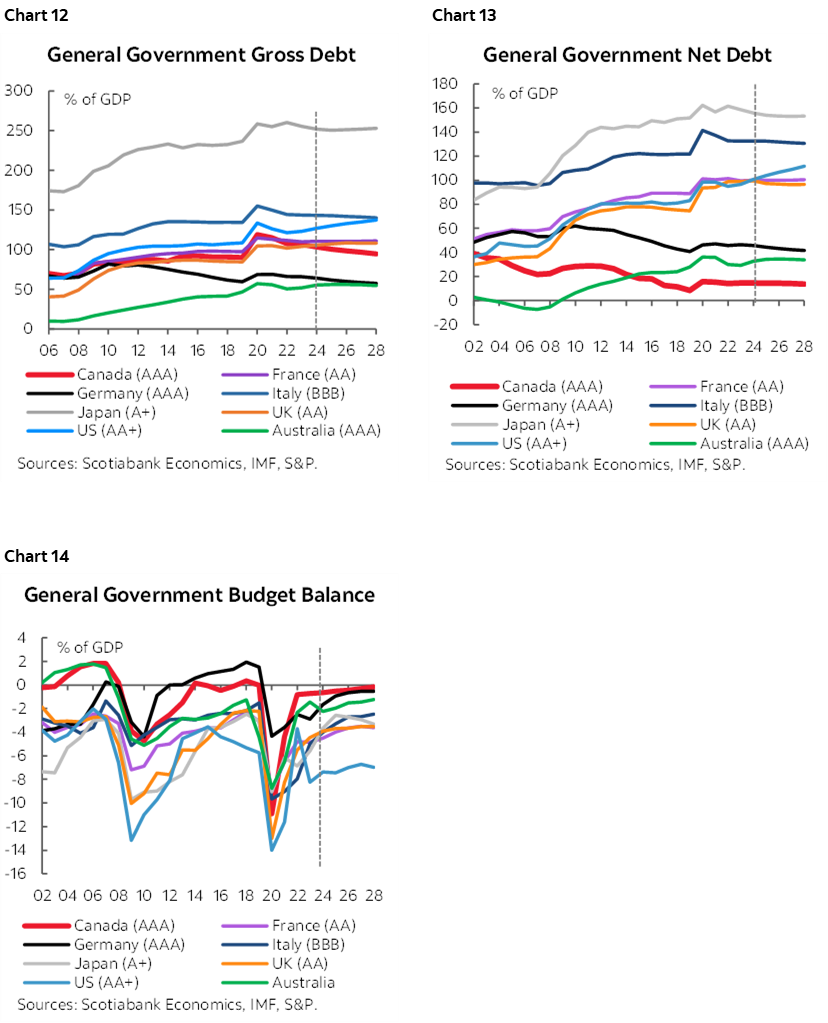

Markets are less discerning around fiscal fundamentals right now. Canada fares well on a relative basis. Government debt—general or federal, net or gross—is pretty good and its deficits relatively small plotted against peers (charts 12–14). But Canada doesn’t benefit from higher market risk tolerance afforded to reserve-currency countries. Complacency could come at a cost down the road especially as angst over affordability and increasingly productivity is hitting newswires outside the country, raising questions about Canada’s longer term growth prospects.

PUNTING OFF TO TOMORROW

As the global economy is well into its fifth year of serial shocks and ever-evolving uncertainty, the federal government gets points for predictability. The federal government has continued to spend irrespective of the economic conditions and ahead of this budget, it has sent a loud signal that it intends to continue. To be fair, a reasonable share of new spending over the last few years is directed to investments that should unlock stronger growth down the road, but systems are in overdrive. The federal government will need a heavier dose of pragmatism as it looks to execution including quick-fail valves for programs that under-deliver.

Stronger growth down the road also inevitably involves trade-offs. By definition, it implies forgoing consumption today for greater investment that mostly delivers results tomorrow. Governments aiming to backstop those trade-offs risk working at cross-purposes. Canadians need to have a more fulsome debate on some of those bigger-picture trade-offs sooner rather than later.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

CERTAINTY OF SPENDING SECURED

- Canada’s federal Finance Minister will table Budget 2024 on April 16th. There should be little fanfare as the big-reveals have been rolled out on a near-daily basis over the past fortnight.

- Announcements to-date amount to $43 bn with major new spending in housing, pharmacare, military, and AI. About 60% (or $26 bn) of this would likely hit the bottom line directly. Allow for a few more surprises on budget day for a reasonable final budgetary toll of about $31 bn over the horizon.

- Modest economic (and revenue) tailwinds in the near-term should partially offset some of the final price tag, while denominator effects should further minimise the impact on the bottom line as a share of GDP. This would yield a marginally higher path for deficits as a share of GDP and only slight GDP-driven differences for the debt profile (charts 1 & 2).

- In isolation, near-term demand measures in the budget are likely to be modest but the cumulative impact of government spending across all levels over time have made the Bank of Canada’s job all the more challenging. Provinces have added another $44 bn in incremental new spending over the next two years alone this budget season.

- This budget won’t likely trigger an election but it is clearly a warm-up lap as Canadians brace for the polls within the next 12–18 months. The taps are unlikely to be turned off any time soon.

- On the margin, this budget will very likely reinforce Scotiabank Economics’ call that it is premature to begin interest rate cuts just yet.

FORWARD GUIDANCE

Canada’s federal Finance Minister delivers her annual budget on April 16th. Nominal economic growth has been substantially stronger than the official outlook last Fall but the misses are narrowing. Scotia Economics projects nominal growth 1.5 ppts higher in 2024 relative to the Fall update, albeit with some pull-forward from 2025. The net impact would still see output levels 1.2% higher at the end of 2025. Otherwise, there has been little change to near-term inflation and interest rate outlooks, though long term rate risk may be down-played over a longer horizon (table 1, at the end).

Spending is clearly set to continue. Departing from past years’ practices of “unofficial leaks” ahead of fiscal updates, the Canadian federal government has gone on the offensive with a slew of official announcements across the country in the weeks ahead of this budget. The preliminary tally—we’re still five days out—runs at $43 bn with a lions’ share directed towards housing, along with steps to lock in universal pharmacare, ramped up military spending, and AI investments. (See box 2, at the end for a list of measures announced to-date). Not all of this will impact the budgetary balance, nor will they likely stop there.

A best-guess for the final tally of net new budgetary measures on B-Day is $31 bn. Roughly 60% of already-announced measures (or $26 bn) would likely impact the budgetary balance, while the remainder likely hits only non-budgetary financing requirements (i.e., it matters for bond supply but doesn’t show up on the bottom line). Pencil in another $5 bn between now and 4 pm E.T. on April 16th when the curtain lifts. This is in the ballpark of recent spending packages irrespective of economic or fiscal performance.

Fiscal trajectories could look broadly similar to paths set out last Fall. An estimated (albeit tenuous) $15 bn in economic and fiscal improvements over this horizon would partially cushion new spending, leaving an incremental budget shortfall of about $14 bn over the planning horizon (through FY29). Meanwhile, stronger-than-anticipated nominal output this year would mostly render marginally higher—but mostly imperceptible—differences to the deficit and debt trajectories as a share of GDP (chart 1 & 2). (Though with stale forecasts and conservative budgeting, they may not book all of this just yet.)