- Canada’s Parliament continues to debate long-awaited legislation for a new disability benefit that was promised in the early days of the pandemic.

- The challenges are significant: more than one in five Canadians live with a disability, only three in five find employment, and those with disabilities are twice as likely to live in poverty (and thrice as likely if those disabilities are severe).

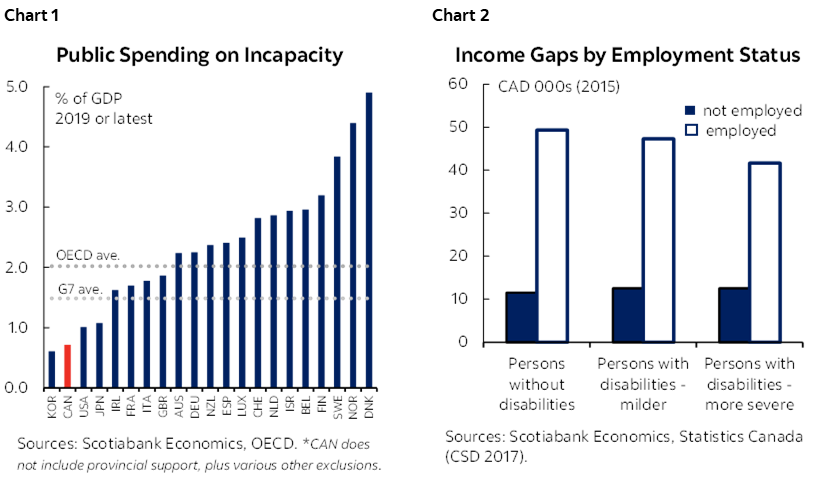

- Despite relatively generous social spending overall, Canada’s federal outlay directly targeting those with disabilities is among the lowest across OECD countries at around 0.7% of GDP (chart 1).

- A new disability benefit should be a step in the right direction, but, alone, it may either be very costly or insufficient. It could take around $4–5 bn annually just to lift those living in deep poverty—estimated at 550 k individuals—to the poverty threshold. (To be clear, the government is not likely to put this quantum on the table when details are revealed.)

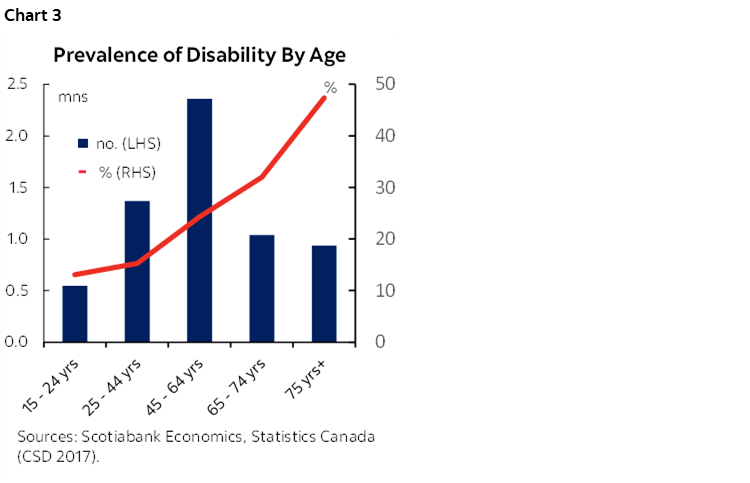

- Inclusive labour markets need to do more of the heavy lifting to help Canadians with disabilities achieve financial security. Statistics Canada estimates that there are over 850 k Canadians with disabilities who have the potential to work, but are not currently employed. Those with jobs earn triple the income of those without gainful employment (chart 2).

- Employment is a key pillar in the federal government’s new Disability and Inclusion Action Plan. This is backed by a doubling of the Opportunities Fund for Persons with Disabilities, which provides various supports and wage subsidies, but these investments will likely still pale against the (eventual) new transfer program.

- It is a collective responsibility across stakeholders to significantly scale up efforts to facilitate access and attachment to the workforce. A stepped-up wage subsidy linked to the individual could be just one example. Existing tools such as the disability tax credit, various employment-related insurance programs and the cross-walks to provincial programs must also be fit-for-purpose such that they balance the incentives to work with the wide ranges in need and potential.

- This is no doubt a complex and delicate issue, but one that Canada cannot afford to ignore. Moral arguments aside, structural labour shortages and an aging population suggest the impacts will be all the more acute if left unaddressed. Or worse, a poorly-designed transfer program could further exacerbate these challenges.

THE SHEER NUMBERS ARE STRIKING

More than one in five Canadians live with a disability. That number may very well be closer to one-in-four as the most comprehensive count (6.2 mn Canadians 15 years and older) under the Canadian Disability Survey (CDS) is dated at 2017. A new count is underway, while imperfectly-aligned data from the annual Canadian Income Survey counts 8.9 mn Canadians aged 16 years and older with a disability (or 28%). An aging and growing population will continue to nudge these up both in percentage and number terms.

The pandemic may be adding further pressure to these numbers. Some 1.4 mn Canadians are reporting prolonged symptoms or long COVID. Workplaces have also seen an uptick of almost 3 ppts in the prevalence of disability in the labour force (to 21.5%) between 2019 and 2021. Statistics Canada largely attributed this change to an increase in mental-health-related disabilities among those already employed versus an increase in employment of those with disabilities.

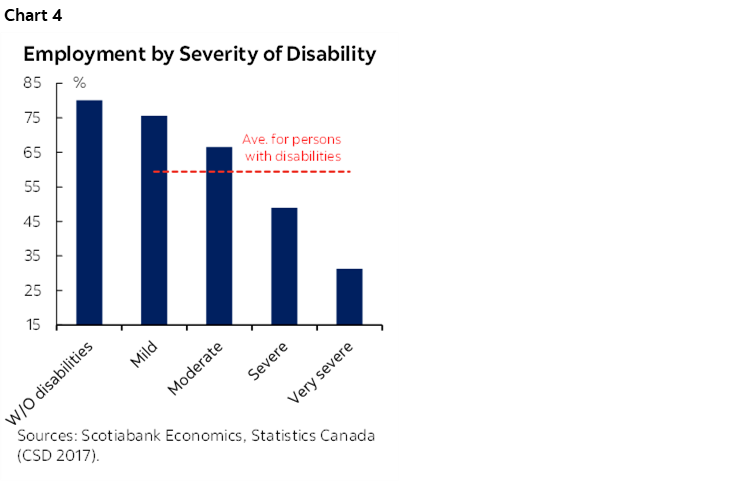

There is no uniform picture of disability. Common disabilities range from pain, flexibility, and mobility to mental health. Certain disabilities are more common within age cohorts: developmental disabilities are most prevalent for youth, mental health for young adults, and mobility for seniors. A quarter of disabilities among the working-age population are work-related, according to Statistics Canada. Prevalence increases with age from 13% among ages 15 to 24 years to 47% for those 75 years and over (chart 3). The severity can also vary widely with over 40% of the 6.2 mn Canadians reporting severe or very severe impacts.

THE HURDLES ARE HIGH

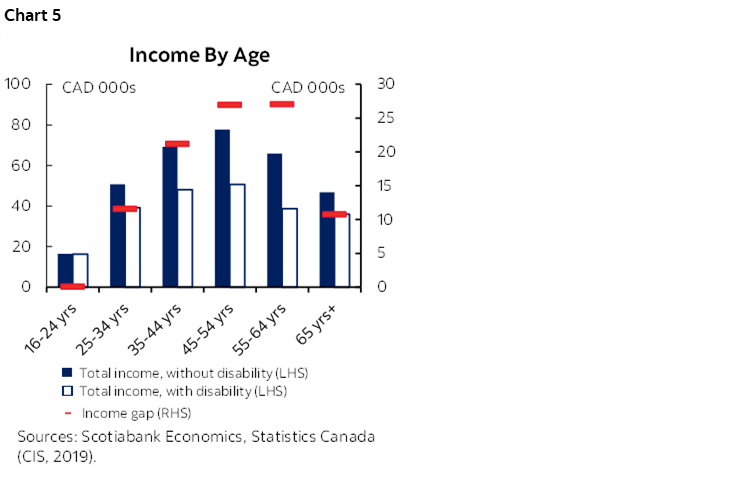

Canadians with disabilities can face serious impediments to labour force participation. Just under 60% of those with disabilities of working age (25–64 years) are employed. This is more than 20 ppts below the rate for peers without disabilities. This gap widens with severity: less than half of those with “severe” disabilities are employed while less than a third with “very severe” disabilities have a job (chart 4).

A staggering 45% of persons with disabilities have the potential to work in an inclusive labour market. The federal government estimates 1.9 mn Canadians aged 15 to 64 years with disabilities are neither in school nor employed, of which about 852 k have the potential to work. Statistics Canada’s methodology excludes a range of individuals from this count, including those whose conditions prevent them from working and/or for which no workplace accommodation would enable work.

The barriers to workforce participation can be complex. Challenges can differ according to the type, severity and persistence of disabilities. Workplace barriers can include awareness, biases, discrimination and (real or perceived) resource constraints to the provision of greater accessibility. These may vary across sectors and organisational sizes. Greater strides are still needed in fostering accessible workplaces by design that would translate into less need for accommodation at the individual level. Participation can also be influenced by policy environments (e.g., tax and benefit structures) in some instances. The OECD categorizes such barriers into capabilities, opportunities, and motivations.

THE FINANCIAL TOLL IS TREMENDOUS

While the impediments to labour force participation may be complex, the impacts on household financial security are not. Canadians with more severe disabilities, for example, live on incomes half that of their peers without disabilities according to the 2017 survey. These numbers mask even wider disparities once employment status is considered. Employed Canadians with disabilities have income levels about three times higher than their counterparts not working—but still 15% below those without disabilities. And there are further wage penalties for females.

The income gap widens over prime working years. Canadians aged 25–54 years without disabilities, for example, have total incomes (market income and government transfers) that are about 40% higher (or $19 k) than peers with disabilities, with the premium widening to 70% (or $27 k) by ages 55–65 years (chart 5). The income gap then narrows in retirement consistent with shifts to retirement income, generous old age transfers, along with late-onset disabilities. Government transfers reflect about 20% of total income for working-age Canadians (25–65 years) with disabilities versus about 10% of those without disabilities.

DISABILITY AND POVERTY GO LARGELY HAND IN HAND

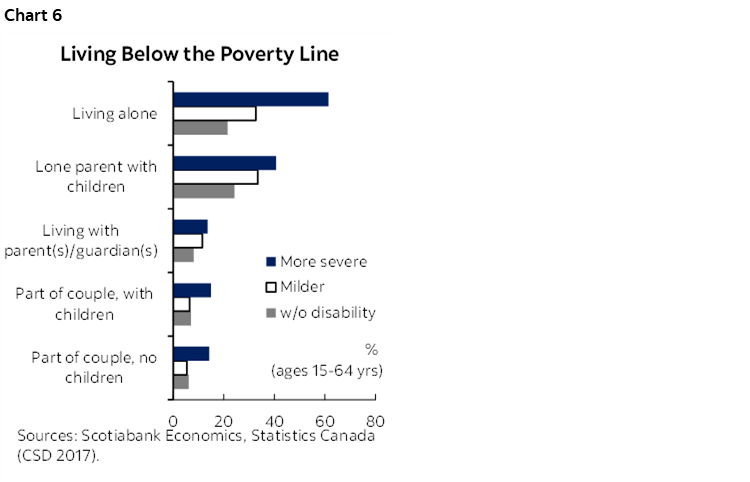

Poverty rates for those living with a disability are high. Almost 30% of Canadians with more severe disabilities were living below the poverty line according to the 2017 survey—three times the rate of peers without disabilities. The share is halved for those with milder disabilities (close to 15%), but still uncomfortably high (chart 6). Poverty rates are particularly exacerbated among lone-adult households with more severe disabilities where more than 60% fall below the threshold. In numbers, over a million Canadians with disabilities were living below the poverty line in 2019 before the pandemic struck.

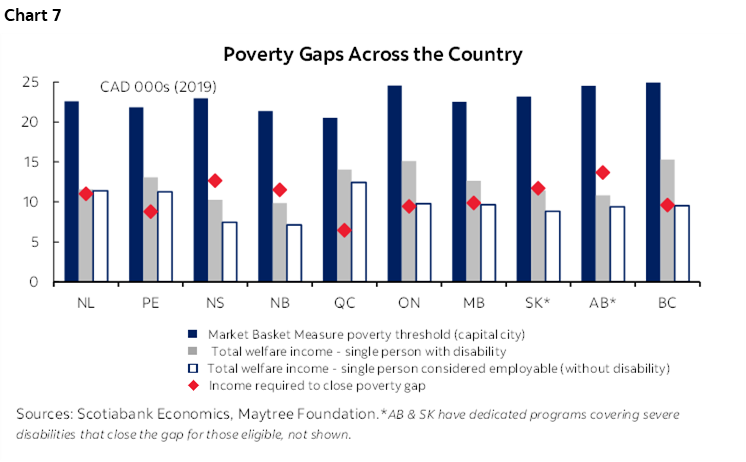

Most live well below the poverty line if exclusively reliant on government support. The poverty gap—or the difference between income and a low-income threshold as defined by the Market Basket Measure—varies across the country given differences in provincial government benefits as well as costs of living. The Maytree Foundation helpfully estimates these values across the country putting the average (weighted) gap in the order of $7,500 k annually for a single person with a disability (chart 7).

Canada’s targeted support towards this vulnerable population pales relative to most advanced economies. Despite considerable social spending overall—at a pre-pandemic 18% of GDP that is roughly on par with the OECD average—Canada’s federal spending directly targeting incapacity (an outdated term used by the OECD) is among the lowest at 0.7% of GDP or about $18 bn across all levels of government (chart 1 again). This does not include provincial support which can be substantial, nor does it include broad-based federal supports as well as some targeted tax, savings, or labour programs. Nevertheless, even a doubling of the reported amounts through the OECD would not substantially improve its overall standing.

A STEP IN THE RIGHT DIRECTION

The new Canada Disability Benefit should be a welcomed development once it is passed. This long-time Liberal pledge is currently being debated in Parliament. Draft legislation provides few details, but it has been pitched as a monthly payment to low-income, working-age individuals with disabilities. The federal government makes parallels to the Canada Child Benefit (CCB) and the Guaranteed Income Supplement (GIS) for seniors, both income-tested transfers to individuals.

Arriving at a base will be the first of many design challenges. About 4.3 mn working-age (15–64 years) self-identified with having a disability(s) in the 2017 survey, whereas 1.4 mn Canadians were designated under the federal Disability Tax Credit in 2020. The new Action Plan references over 900 k working-age Canadians living in poverty (and 550 k in “deep poverty”), which hints at the targeted base.

The price tag may either be very high...or the amounts small. For illustrative purposes, closing the approximate $7,500k annual poverty gap for 550k Canadians living in deep poverty would amount to about $4.5 bn annually. These are purely ballpark numbers to grasp the magnitude of the shortfall, but they are not out of the range of other income-tested transfers: 3.7 mn households receive the CCB at an annual fiscal cost of about $25 bn (FY23), while about 2.2 bn seniors receive GIS checks at an annual cost of $15.5 bn (stacked on top of broad-based Old Age Security transfers together amounting to $68 bn annually).

Meanwhile, the federal government (and other levels) will be facing pressure to constrain spending against inflationary pressures and elevated debt levels. Merits aside, major new transfers would add to structural deficits. Given Canada benefits from relatively robust social expenditures as a whole (and more promises are still in the pipeline) and has a very progressive personal income tax structure, a comprehensive review of household transfers may be merited to ensure redistribution is reaching those who need it the most in a world of limited resources. And as complex and contentious as it may be, the concept of impact, not just income, may also have merit in the design of this new transfer.

INCLUSIVE LABOUR MARKETS ARE ESSENTIAL TO MEANINGFUL PROGRESS

Employment could—and should—shoulder more of the weight. The biggest gains for household income and financial security would come from meaningful employment in an inclusive environment that fosters the potential of those with disabilities. The new Action Plan posits employment as a key pillar, backed with a number of measures including a pre-announced $270 mn for the existing Opportunities Fund for Persons with Disabilities. The fund provides a host of supports including training, placement and wage subsidies to just over 4,000 individuals with annual spending of about $40 mn. New commitments should more or less double its footprint.

Even while tackling some of the more challenging cases, the Opportunities Fund has demonstrated positive net benefits. A rigorous counter-factual evaluation calculates a social rate of return of 170%, that is $1 of investment in the program yields a social return of $1.70. Skills and wage subsidy interventions in particular deliver the largest returns, while first-year employment gains were just under 10 ppts and 6 ppts in subsequent years. The discounted benefits of the program exceeded program costs in just under 4 years once the impacts on earnings and other government expenditures are taken into account.

Estimating the economic impacts of higher labour force participation for those with disabilities is fraught with challenges, not the least because of poor data. According to annual income data (CIS), 6 mn Canadians (16–64 yrs) identified with a disability, of which 1.3 mn received no market income. Using Statistics Canada calculations that about 45% of these individuals has work potential, a very simplistic approach that lifts their income to the median market income of peers their age with disabilities would yield about $20 bn in income effects alone. This may be unrealistic given the underlying range in severity of disabilities within the group. But even a more granular approach (using CDS data) that attempts to account for this—for example, assuming the employment rate of those with milder disabilities approaches those without disabilities and that those with more severe disabilities benefit from a 10 ppts improvement in the employment rate—could bring income effects to around $10 bn.

The really big dividends (from a macroeconomic perspective) would come from closing the market income gaps for those with disabilities relative to their peers without disabilities. Lifting the income of those 4.7 mn Canadians working with disabilities to the median of their peers would translate into an additional $60 bn. In both instances, there would be indirect effects as well, through potentially reduced need for social supports, higher contributions through income taxes, and higher consumption (and investment) in the community.

TAKING LABOUR MARKET MEASURES TO SCALE

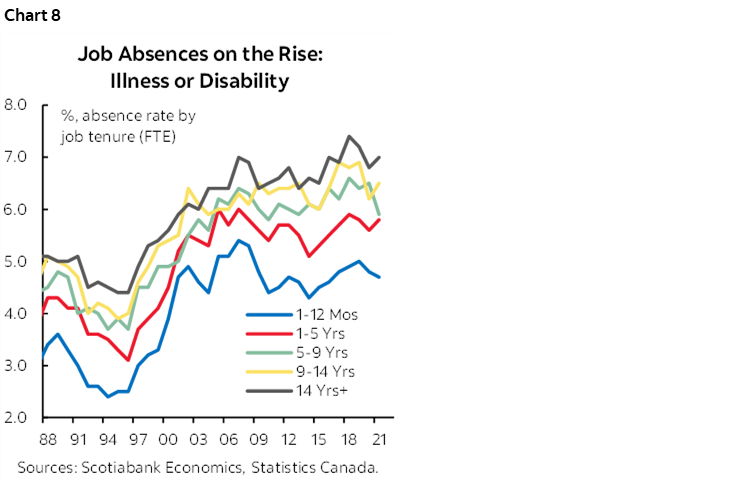

It is a collective responsibility across government, the private sector, and social actors to massively scale up efforts to unlock employment opportunities. Structural labour shortages against an aging society should underscore the urgency for employers to tackle some of the barriers to inclusive working environments. A compelling case is not only based on vacant positions—or soon-to-be-vacated ones with one-in-five Canadians approaching retirement age—but also on retaining employees. With a higher prevalence of disability with age, employees will increasingly need to embrace an inclusive and accessible environment. Workplace absences related to illness or disability have trended up over the last several decades (chart 8).

Business still has large strides to make in fostering an accessible workplace. There is evolving work by the likes of Disability:IN (Scotiabank is a corporate partner) that is advancing the business case for hiring and supporting talent of all abilities. Beyond simply filling vacancies and driving higher retention rates, people with disabilities can bring unique skills and perspectives that foster innovation within an organisation and influence its decision-making to reflect the society within which it operates. Early research is also exploring the link to stronger corporate performance, but it is challenging to disentangle the impacts of simply good governance.

At the same time, government(s) may need to consider greater financial supports to facilitate faster progress in closing gaps. This could include, for example, scaled-up wage subsidies that are commensurate in size and ambition embedded in the (eventual) new disability benefit. Overcoming some of the drawbacks of the pandemic wage subsidy program, these benefits could be linked to individuals themselves as a portable benefit with clear crosswalks to the new disability benefit. The design could ensure appropriate incentives to work to one’s full potential in an inclusive environment while ensuring adequate resources to accommodate individual needs. The government could also review the federal disability tax credit as a tool to smooth potential distortions to the financial decision to work in light of the eventual new benefit. A case could be made to even further tilt incentives in favour of labour force participation if viewed through the lens of total social returns and/or wage penalties for those with disabilities. (The recent changes to the Ontario Disability Support Program are a positive step in this regard.)

Securing stronger attachments to the labour force would also open up other existing safety nets to individuals with disabilities. The case for an insurance-based approach to disability is strong: it is not generally known a priori who will be born with a disability or may acquire one later in life so the costs can be spread across a wider range of potential beneficiaries. The federal Employment Insurance program, the Canada Pension Plan, and various provincial workplace insurance programs have disability clauses, but these programs require an attachment to the labour force.

At the end of the day, a wide range of tools tailored to circumstances will be required. Examples offered here are not intended to be exhaustive, but rather illustrative only. We very likely need more tools, they need to be deployed at a much larger scale, and the interaction across them should balance considerations of workplace capabilities, opportunities, and motivations, in addition to financial security.

LOOKING AHEAD

The eventual federal disability benefit might successfully lift more Canadians with disabilities above the poverty threshold, but more effort is needed to achieve meaningful employment gains that could afford these Canadians an even higher standard of living. And in doing so, it would also enable much deeper support for some of the most vulnerable among disabled Canadians where employment is simply not an option. There is still a lot of work ahead that is needed on definitions, data, and policy design, while the landscape is further complicated under decentralised delivery of many programs under provincial Labour Market Agreements. But the sheer scale of the challenge and its impacts and implications for households, businesses and governments means the country cannot afford complacency.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.