STEPPING UP TO THE PLATE ON THE GREEN TRANSITION (AND COVERING ALL BASES)

- Canada’s Federal Budget 2023 delivers mostly against expectations as priorities were well-channeled ahead of its March 28th release and readied markets for another fiscally expansive plan.

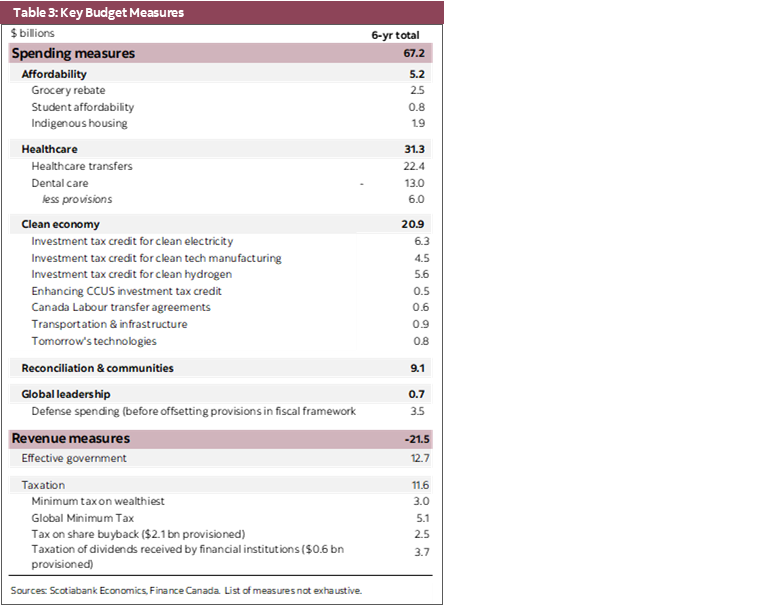

- Gross new spending measures tally $67 bn over the planning horizon through FY28, including $21 bn in “clean economy” investments, $31 bn for healthcare (most announced earlier but with some cost inflation), a $9 bn catch-all category, and $3.2 bn in near-term affordability measures.

- Revenue-raising measures in the budget are material: $12 bn in additional targeted tax measures—including a change to dividend taxation for financial institutions—along with a somewhat opaque $12.7 bn in government savings and reallocations in outer years. These render net new spending lower at $46 bn in Budget 2023.

- Unlike recent updates, a weakening economic outlook adds another $26 bn in fiscal needs over the horizon. Folding in new budgetary measures, the net impact amounts to a $69 bn deterioration in the bottom line relative to earlier projections.

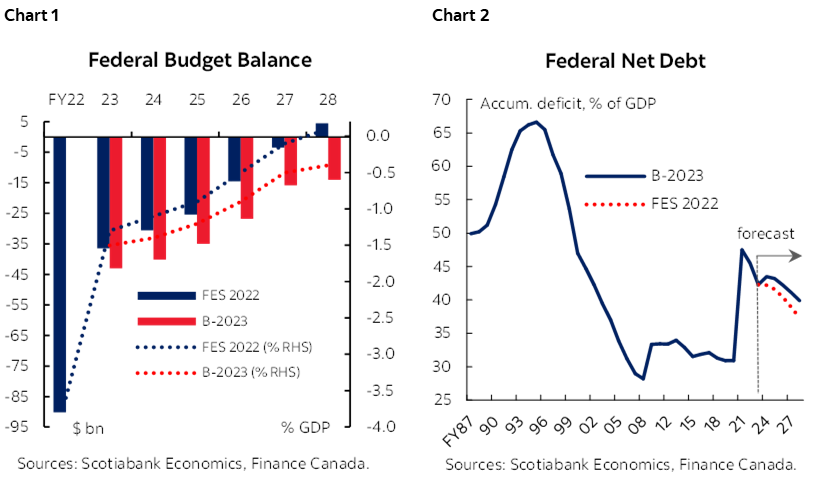

- The fiscal balance is still projected to decline over the horizon, albeit at a slower pace, from -1.5% of GDP in FY23 to -0.4% of GDP in FY28 (chart 1). Net debt trends downward over the medium term, but is expected to temporarily breach the government’s soft fiscal anchor this year owing to weak output (chart 2).

- Two signature initiatives are new refundable investment tax credits for clean manufacturing industries and clean electricity (30% and 15%, respectively). These are welcomed developments that should go some way in addressing anemic investment within strategic sectors and put Canada on stronger footing vis-à-vis the US.

- Near-term demand measures in the order of $3.2 bn are well-targeted, but are additive to a host of other supports already in the system, which, cumulatively don’t make the Bank of Canada’s job any easier as it tries to steer inflation back to target against a range of upside risks.

- Nevertheless, the budget will be digested in a volatile market environment where exogenous factors are mostly carrying the day. Continued federal fiscal activism is largely anticipated and Canada’s relative debt advantage should still be intact when the dust settles.

A COUPLE OF LEFT-FIELDERS

Canada’s federal Finance Minister delivers another budget amidst heightened uncertainty. The baseline economic projections underpinning this budget provide limited value. Despite pre-dating recent financial market turmoil, it reflects persistent bearishness on economic resilience, while underestimating inflationary pressures (table 1). Projections for real and nominal growth this year are 0.3% and 0.9%, respectively. This leaves room for some potential upside (and this budget includes such a scenario), but clearly a downside scenario is not far-fetched.

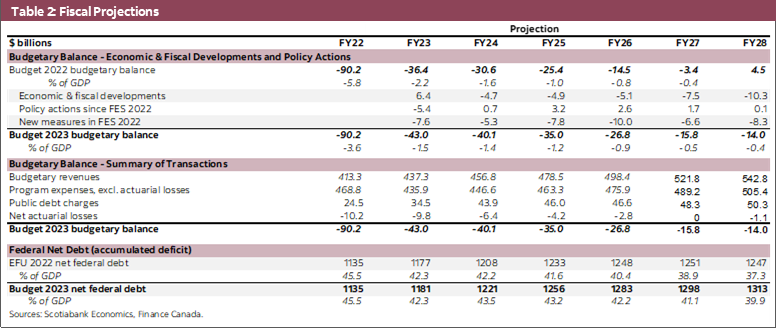

The budget delivers a fresh round of spending (and then some) mostly channeled ahead of budget day. Gross new spending measures amount to $67.2 bn through FY28, offset by $21.6 bn in revenue-raising measures, for net new measures of $45.6 bn. A deteriorating economic outlook further weighs on the outlook in the order of $26.1 bn yielding a net budgetary impact of $68.9 bn (table 2). This is expected to drive a modestly looser fiscal path over the horizon relative to earlier projections, with a -1.5% deficit in FY23 declining to -0.4% of GDP by FY28. This would keep net federal debt on a downward over time (from 42.2% of GDP in FY23 to 39.9% of GDP by FY28), but not before breaching its own soft fiscal anchor with a near-term uptick this year (to 43.4% of GDP) owing to weaker expected growth.

Key thrusts of the budget were widely reportedly ahead of Tuesday’s release. A “clean economy” is the centerpiece with $21 bn in new spending, notably refundable investment tax credits for green manufacturing (30%) and clean electricity (15%). Healthcare measures are mostly expected though surprise on the upside as dental costing doubles bringing total new health-related spending to $31 bn. Targeted affordability measures are costed at $3.2 bn, mostly via a one-time Grocery Rebate. A residual $9 bn ticks off boxes in a wide range of other areas.

Revenue-side measures may raise some eyebrows. New tax measures raise $11.6 bn over the horizon, mostly delivering on earlier commitments (an Alternative Minimum Tax for high-income Canadians; a Global Minimum Tax for multinational corporations; a tax on share buybacks), while expanding an earlier one: changing the tax treatment of dividends received on Canadian shares held by financial institutions that is expected to yield $3.15 bn over five years starting in FY25 (and $790 mn ongoing). The government also tables an opaque $12.7 bn in government savings involving a combination of savings on travel and consultants ($7.1 bn) and reallocation of existing spending but with no discernable impact on operating costs relative to the Fall outlook (flat), while program expenses increase by $42 bn expenditures over this horizon relative to earlier projections.

Major new investments in the “clean economy” should help enhance Canada’s growth potential over the medium term. It is not likely enough to alter our growth outlook this year or next (though clearly there are sector-specific implications in this budget overall), particularly as pervasive uncertainty is working in the opposite direction and implementation will lag, but it should overall be viewed positively. Along with earlier-announced measures amounting to $37 bn in the last two years, Budget 2023’s $21 bn should put Canada on firm footing with US policy measures in key sectors. (Further details on new spending are included in Box 1 and table 3.)

Near-term demand-side measures won’t make the Bank of Canada’s job easier, but they likely represent a risk—not a revision—to its baseline. Fiscal activism across all levels of government has been predictable, if not persistent. Budget announcements layer in about $3.2 bn (0.1 % of GDP) in near-term support measures that are well-targeted, but are additive to a host of previously-announced federal and provincial measures that are likely closer to 0.5% of GDP. This is likely already embedded in fiscal expectations for the most part. While acknowledging inflation is not exclusively a Canadian phenomenon, continued household supports will likely keep the Bank of Canada guarded against premature policy loosening absent a substantially worse-than-warranted deterioration in the economic outlook as demand sits above capacity.

The government looks to markets to finance the new plan. Borrowing requirements for FY24 are estimated at $421 bn (85% reflecting refinancing needs) slightly higher than FY23 requirements of $394 bn reflecting in the fall update. This includes $172 bn in bond issuance versus $185 bn issued in FY23, while increasing treasury stock. Though bond issuance will lighten up its pandemic-era long-term emphasis, 10-year and over issuance will still sit above historic levels), while canceling the 3-year sector. (Note, the incremental change in supply would be overwhelming offset by maturing government bond assets rolling of the Bank of Canada’s balance sheet.) Otherwise, the debt management strategy signals some potentially big changes underway including a review of Canada Mortgage Bonds (with a view to consolidating them into regular borrowing and reinvesting savings in affordable housing programs, an area mostly absent in the budget) absent in the budget) and it continues to hold its cards close with respect to green bond issuance and an eventual sustainable bond framework.

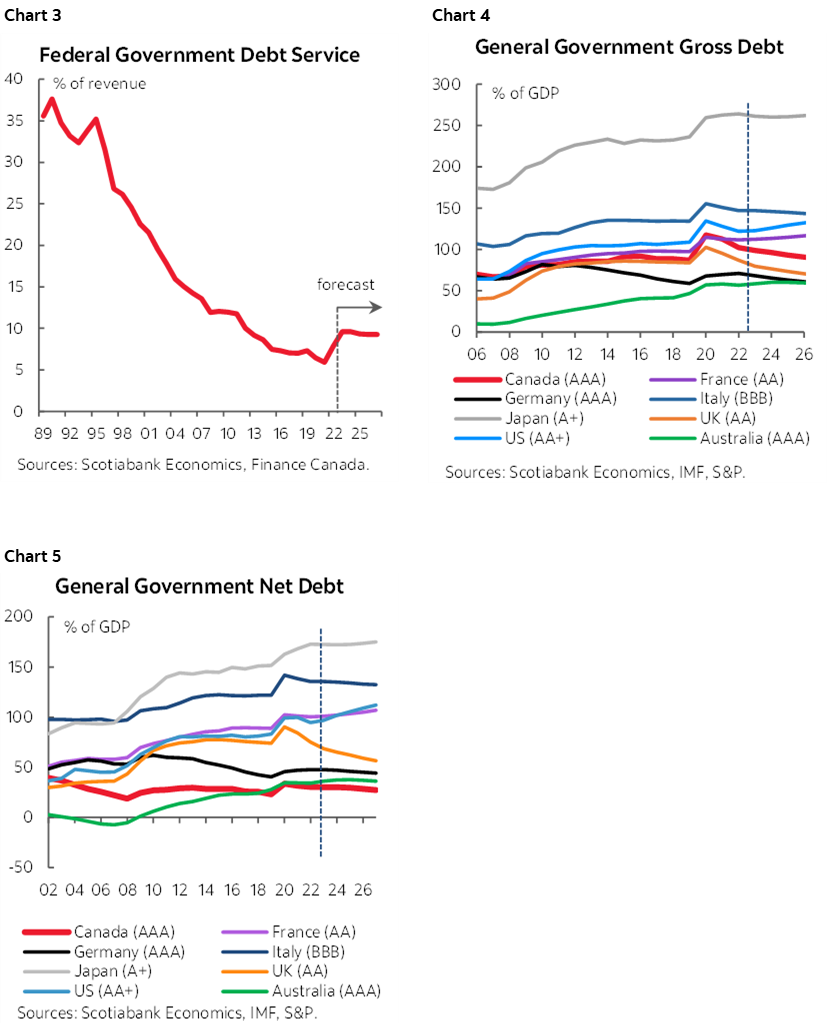

This budget will be digested in a volatile market environment where exogenous factors are mostly carrying the day. Market uncertainty is underpinning demand for all risk-free securities even if relative rate paths and reserve currency status are driving differences within the global asset class. Earlier efforts to term out federal debt reduce some exposure to interest rate risk, but interest rate uncertainty over the medium term should caution against complacency despite relatively low debt servicing costs (chart 3). Nevertheless, Canada’s relative debt advantage should still be intact when the dust settles. Today’s budget, along with broad-based improvements in most provincial fiscal outlooks in recent weeks, should underpin a continued consolidation of general government finances—a claim few peers can make—when the IMF updates its comparative data next month (charts 4 & 5).

Canada has stepped up to the plate on the green transition, now it has to hit a homerun. Implementation is key and the feds have their work cut out for them against a complex policy, regulatory and constitutional landscape. Meanwhile, other longer term policy challenges are mostly punted to another day (and another mandate). Notions of fiscal restraint are mostly farcical with a patchwork approach to revenue-raising measures to support ever-growing expenses, while the government breaches its own soft anchor in a baseline scenario as growth moderates no longer preserving this escape clause for a more serious deterioration in the outlook. The government needs to shift from fiscal restraint to fiscal reform if it wants to keep hitting homeruns even as the economy slows.

BOX 1: BUDGET WINNERS

A “clean economy” is the budget’s centrepiece. Signature initiatives are a new 30% refundable tax credit for green manufacturing investments in machinery and equipment ($4.3 bn) along with a 15% refundable investment tax credit for clean electricity ($6.3 bn) that both taxable and non-taxable entities (including Crown- and publicly-owned entities) would be eligible. These are broadly calibrated to similar measures under the US Inflation Reduction Act both in terms of the maximum level of the credit, along with labour and apprenticeship conditions though focus on investment versus production incentivise. These investments reflect an important follow-through to last Fall’s acknowledgement of Canada’s abysmal productivity, supressed in part by a lagging investment landscape. It should dually address competitiveness concerns—a long with earlier-announced investment tax incentives—while boosting growth potential over the long run.

Healthcare investments are largely contained to earlier-announced measures, but with inflationary costing. The $198 bn for provinces over ten years announced in earlier February works out to $22.2 bn in incremental funding through FY28. The budget also announces a new dental care plan, as expected, expanding coverage from children to all uninsured Canadians with household incomes below $90k. The costs has more than doubled—from an earlier-provisioned $5.9 bn over five years to $13 bn (and $4.4 bn on-going—to be administered by a third-party benefits administrator. This adds a fairly substantial structural cost to federal finances with minimal consideration of trade-offs, including NDP’s pharma care pitch that doesn’t make the budget cut again. Overall, healthcare investments in this budget should stem some of the bleed from Canada’s patchwork healthcare systems, but are unlikely to tackle root causes (though cross-country data will be a start). Structural adjustments to long term healthcare funding sustainability are punted down the road (and potentially exacerbated as provinces start rolling out tax cuts).

The budget also delivers additional affordability measures as expected. A new “grocery rebate” will provide $2.5 bn in FY23 delivered through the existing GST rebate program which is income-tested but otherwise unconditional. It would work out to about $467 per low-income household with children. There is another $814 k in near-term relief for students with a 40% increase in grants and interest-rate relief. Housing measures are folded into the affordability chapter, with $4 bn towards Indigenous housing, but otherwise no major new measures announced. While not minimizing the cost of living pressures facing many Canadians, the budget fails to move on more enduring support, for example, supporting greater supply of social housing in light of elevated shelter costs that are likely to remain unaffordable for vulnerable Canadians even after general price appreciation subsides.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.