- Canada’s economy is back on track partly thanks to revisions

- Revisions brought the BoC’s Q3 forecast back onside

- 2021H2 growth is tracking rather favourably

- Spare capacity is on track to be eliminated in 2022H1…

- ...supporting a Q2/Q3 rate hike

- How the BoC may play it in the December statement

CDN GDP, m/m % change, September, SA:

Actual: 0.1

Scotia: 0.0

Consensus: 0.0

Prior: 0.6 (revised up from 0.4)

October ‘flash’ guidance (m/m SA): 0.8%

CDN GDP, q/q %, Q3, SAAR:

Actual: 5.4

Scotia: 2.5

Consensus: 3.0

Prior: -3.2 (revised down from -1.1)

Overall positive revisions to Canadian GDP saved the Bank of Canada’s forecast bacon—and everyone else’s for that matter. That’s important to note in terms of what it says by way of slack estimates in the economy compared to what the BoC was likely tracking before this morning. Canada is inches from a full recovery in GDP now with October only about ½% behind pre-pandemic GDP levels (chart 1).

Despite the stronger than expected results, the Canadian dollar depreciated after the release. That was probably much more driven by Fed Chair Powell’s hawkish pivot during Congressional testimony that consumed most of the attention as he now leans toward ending purchases ‘months’ earlier than previously guided. The market moves are also more driven by Omicron influences upon broader risk appetite. Canada’s shorter-term rates are a touch higher but that too is lagging the US move higher.

The Bank of Canada’s 5.5% growth forecast for Q3 in the October MPR only nailed it because of big revisions that created a weaker jumping off point by the end of June combined with stronger than previously understood estimates for July and August. Q2 GDP now registers a -3.2% q/q contraction versus –1.1% previously and –1.1% is what the BoC had gone with in its October MPR. July GDP growth was revised up 0.4 percentage points to a gain of 0.3% from a drop of -0.1% as previously estimated, while August GDP growth was revised up two-tenths to 0.6% m/m. Suddenly, Q3 wasn’t much of a soft patch after all!

The net effect of revisions that stretched back to well before the pandemic struck plus fresh readings up to October is that the level of GDP is considerably higher than had been tracked beforehand.

How so? For starters, the sum total of revisions up to August raised the level of monthly GDP by 0.4%. Up to June, this morning’s revisions on net knocked 0.2 percentage points off of the level of GDP. Subsequent revisions to July and August were more than offsetting in order to net out to this 0.4% figure. Of course we did not assume these revisions either.

With this reset starting point, the level of GDP only kept rising at a fairly rapid net clip over September and October combined. GDP as at October is about 1.3 percentage points higher in absolute level terms than it was compared to our prior understanding of August GDP before revisions.

Q4 GDP growth is now tracking 4.3% q/q at a seasonally adjusted and annualized rate (chart 2). This is based upon monthly GDP figures using Q3 and October while assuming November and December come in flat in order to focus upon the effects of what we know so far. Flooding in British Columbia is likely to knock this back at least somewhat.

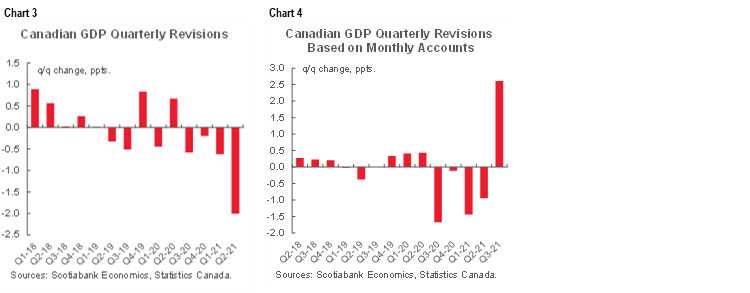

So where we find ourselves on revisions is summed up in charts 3 and 4. Chart 3 shows revisions to quarterly GDP growth up to 2021Q2 using expenditure-based GDP which is what the BoC forecasts. On net, those revisions took GDP levels down 0.2 ppts. That chart stops before Q3 because obviously we don’t have revisions to that measure of Q3 GDP yet after having only gotten the first estimate today. Chart 4 shows revisions to quarterly GDP based upon the monthly income/industry based figures which allows us to extend revision tracking through Q3 in order to show the positive upward revision to the monthly accounts behind the first estimate for Q3 growth using expenditure accounts that we got this morning. This helps to inform how the negative revisions up to Q2 were more than offset by upward revisions thereafter.

WHAT DROVE GROWTH?

Chart 5 shows the composition of GDP growth during Q3 in terms of weighted contributions by category. Household consumption made the biggest contribution of 9% q/q at an annualized rate. Most of that came from services (+7.2%) that are very difficult to track in advance. Inventories dragged three percentage points off GDP growth. Imports subtracted 0.7ppts while exports added 2.4 ppts. Investment was an overall drag of 3.9 ppts mainly via housing (-3.7 ppts).

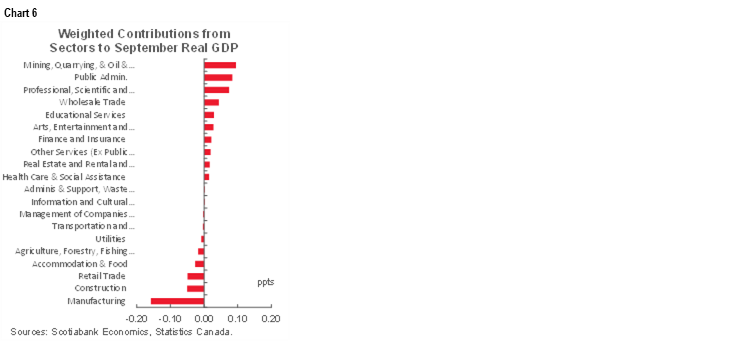

Chart 6 shows the weighted contributions to September GDP by sector. We don’t get details behind the ‘flash’ October estimate until the next report.

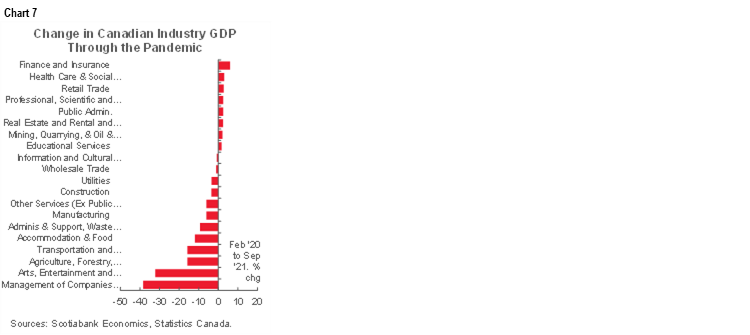

Chart 7 shows the still uneven nature of the recovery to date by sector.

HOW MIGHT THE BANK OF CANADA PLAY IT?

The level of GDP is now tracking 0.4% higher as at August than what we were previously tracking net of all the revisions. The level of GDP is now 0.9% higher as at October than it was compared to revised August. Ergo, since actual GDP levels are tracking higher, there is a little less slack in the economy than anticipated before this morning’s numbers unless potential GDP gets adjusted again.

So how do you play this if you're the BoC? You probably point to still being on track to shut spare capacity over 2022H1 which will bring the next leg of inflationary pressure as the economy then slips into excess demand. You probably look through the effects of BC’s floods that, while damaging to November–December GDP (not to mention folks' lives...), is usually recouped in subsequent months and quarters. The usual playbook is to treat natural disasters in a bygones-be-bygones sense as an intertemporal transfer of activity Q4 into Q1 on rebound effects as business resumes and money is spent on repairs/investment. The BoC would likely treat Omicron as a fresh uncertainty against a more positive evolution of risks up to this point. Overall, the December BoC statement probably plays it safe and stays on track with reinvestment plans and guidance they won’t hike until spare capacity is shut. By January, we should know a lot more about Omicron and at that point they'll issue fresh MPR forecasts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.