- The BoC hiked 25bps as widely expected

- Forecasts lean toward possible further tightening...

- ...and against later easing...

- ...as the Bank attempts to apply stealth forward guidance...

- ...that should be treated with great skepticism

The Bank of Canada hiked its overnight rate by 25bps as widely expected by domestic economists and mostly priced in advance by markets. The bias leaned toward the hawkish end of the spectrum.

The way they did so was to produce forecasts that suggest a continued bias toward further tightening in heavily data dependent fashion while suggesting little to no prospect for rate cuts along the way. After all, why cut rates when growth is resilient forever and inflation is zipping along years into the future. I will explain what I think is the motive to doing so and why you the reader shouldn’t take it too seriously versus doing your own homework.

For now, I would tentatively pencil in a further hike at the September or October meeting especially if data surprises higher, but each decision is being communicated as data dependent and there is a lot of data over the next eight weeks until the September decision that could affect the call. That starts with next week’s CPI that I’ve estimated to be up 0.3% m/m SA.

The market reaction was dominated by US CPI as market participants seemingly assumed that what applies to the US must be portable to Canada. I guess they’ll never learn, given the idiosyncratic nature of many of the developments in Canada these days. The Canada two-year yield is down 14bps on the day in a mild 2s10s bull steepener while CAD appreciated primarily due to broad USD softness post-CPI but is underperforming other major crosses.

Please see the attached statement comparison. The Monetary Policy Report is available here and the Governor’s opening statement to begin the press conference is here.

FADE THE LONGER-DATED GUIDANCE

The BoC issued a set of forecasts straight out through to 2025 that deserves a place on the fiction shelves at your favourite bookstore or the virtual equivalent. How so? Why?

They say there will be no recession. Maybe, but don’t expect them to say anything but. Even during the press conference, Governor Macklem said “there is a path back to price stability with no recession” and that a soft landing remains possible.

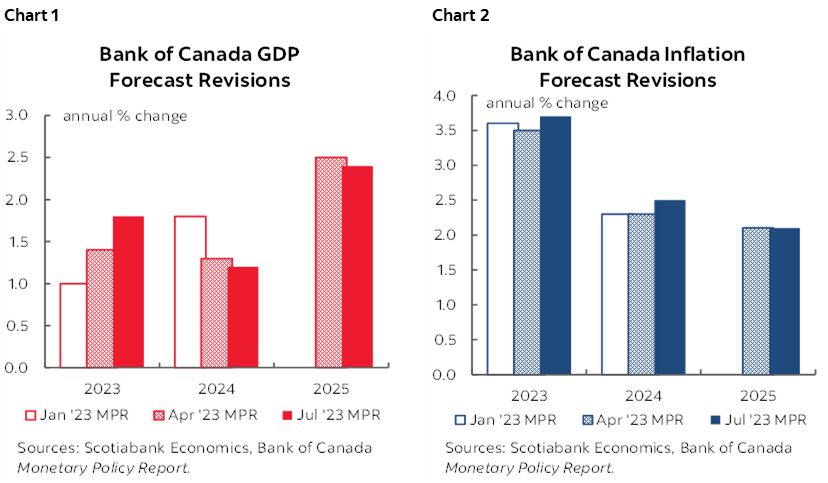

Indeed, on a Q4/Q4 basis, growth is projected to run at 1.8% this year, 1.5% next year and to then accelerate to 2.5% in 2025. CPI is forecast to rise by 2.9%, 2.2% and 2.1% on the same Q4/Q4 basis. Annual GDP forecasts are shown in chart 1 relative to the prior round. Annual CPI inflation forecasts are shown in chart 2.

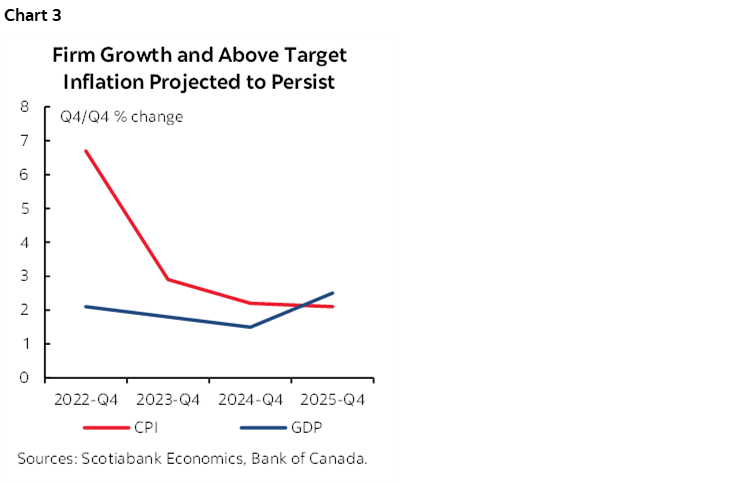

Growth is forecast at 1.5% q/q SAAR in each of 2023Q2 and Q3 implying sustained ok momentum through summer into the Fall this year. Chart 3 shows the soft landing.

Why did they do this? We can’t reject the slim possibility that they may prove to be right, but I think the motives here go much further. One reality is that the political cost to forecasting recession is high in Canada and the cost to being a central bank forecasting a recession in Canada is even higher.

Before I get to what I really think is the motive, it’s also feasible that this is truly what they believe will happen and in no small part based upon how growth and inflation have surpassed their expectations for some time now. If so, then err on the side of continued upside risk. Signals that growth will pick up by 2025 in response to possible future easing once they can implement less restrictive policy as inflation perhaps durably comes around toward target.

But I have a strong suspicion that what they are attempting to do goes much deeper here. Throughout this year they have been in a contest with markets that have been itching to price rate cuts and that was one contributing factor behind the Spring housing rebound and renewed hikes. In a desire to avoid a repeat, the BoC is trying to invoke stealth forward guidance through its forecast numbers. They can’t use explicit forward that proved to be a disaster for the BoC when Macklem promised Canadians that they wouldn’t even be thinking about rate hikes until about now, yet here we are with about 500bps into them. Nobody would believe such explicit forward guidance again in a fool me once shame on you, fool me twice shame on me sense.

So the BoC is trying to do so through their forecasts signed off by Governing Council. How so and why? The BoC knows that its direct influence upon the rates curve rapidly peters out beyond the near-dated measures. They have QT tools that can try to influence longer-dated bonds but that’s a much, much less powerful alternative to the policy rate. Yet the BoC is frustrated that market participants have been pushing it toward pricing rate cuts earlier than the control freaks at 234 Wellington Street in Ottawa would like.

To understand why they don’t want this requires acknowledging that the 5-year portion of the GoC rates curve is the most important benchmark for the Canadian housing market and with it much of the overall interest-sensitive landscape in Canada. So they’re trying to exert their influence further up the curve by producing a set of forecasts that pushes back against any tendency to more dearly price those bonds because it would mean lower fixed mortgage rates given the ballpark 70% of outstanding mortgages that are fixed rate and overwhelmingly in fivers. It would mean more fuel thrown onto the housing fires in the country alongside stronger consumption. That, in turn, would make it more difficult to control inflation back to target.

Fade it. Fade it in that one needs to do one’s own homework without taking their forecasts as gospel. The reality is that the BoC can’t really forecast and certainly not that far out. Not growth, not inflation, not the price of Skittles in Brandon, Manitoba.

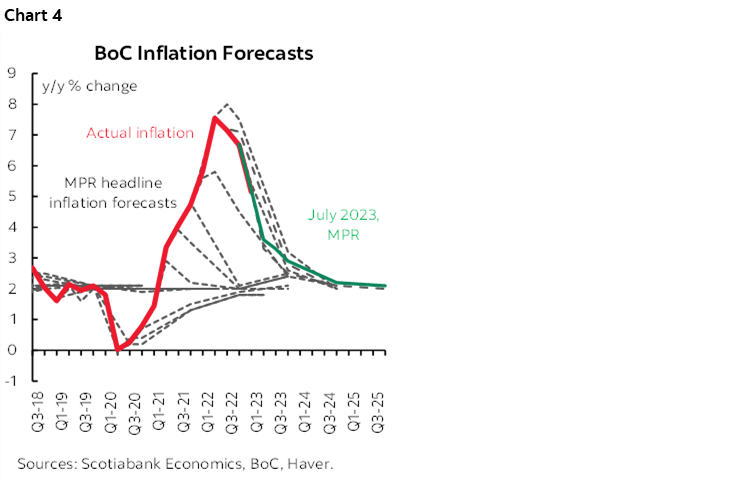

Enter one of my favourite charts that I’ve been using for many years. I call it the Medusa chart (chart 4). You may not turn to stone if you look at it for too long, but you may very well lose your lunch. The thick red line plots actual y/y CPI inflation over the years and each of the dashed lines (aka Medusa’s flailing locks) show inflation forecasts by the BoC in every Monetary Policy Report. They routinely miss the turns as well as undershoot and overshoot inflation forecasts.

If I’m right, then this stealth guidance tool means that should markets resume testing the BoC before it is ready, then markets may court the risk that the hammer gets pulled out again with another policy rate hike to prove the point. Right now they are not doing so, with markets pricing maybe a quarter-point of easing over the next year and maybe 100bps over the next two.

OTHER GUIDANCE

What follows is a gathering of key remarks during the press conference.

The Policy Rate Bias

Governor Macklem indicated that the BoC is prepared to raise its policy rate again if needed and that they will assess their policy stance meeting-by-meeting. They have to say this because the minute they signal confidence they are done is the minute they invite another pile-on into the front-end.

The Governor’s opening remarks said they discussed whether to pause now and assess more data up to the next meeting but decided that the cost to delay exceeded the benefit. He didn’t elaborate on this, but one possibility is that they feel the pressures are great enough to require more action now. Another is the possibility they feared that markets would treat it as a sign of wavering and being done with the next step being to resurrect rate cut pricing they judge as premature.

The statement itself dropped the prior remark that they did not feel the policy stance was sufficiently restrictive, but Governor Macklem stated this in the press conference instead and so I don’t think that was meaningful.

When asked during the press conference to comment on the terminal rate, Macklem said “We're going to be taking each decision one at a time. We see that monetary policy is working. It works with a lag. The full effects have not fed through. Those underlying inflationary pressures are stronger than we expected. With the increase, we see inflation hovering around 3% over the next year and then coming down toward 2% later in 2025. A number of things have to happen for inflation to come back to target. It's clearly too early to be talking about interest rate cuts.”

Household Finances

There were a lot of questions about whether the BoC sympathizes with pressured households and I thought Macklem and Rogers handled them well with sensitivity while making it clear they are focused upon doing their job to control inflation. I think folks need to understand that while there are indeed many pressured households, the BoC is focused upon the broad macro evidence and that the entire point of the exercise of tightening monetary policy is to cause some damage to contain inflation and so far that really isn’t happening enough.

Wages

The Governor was asked whether slower wage increases suggest they are closer to the goal of a cooler labour market. He replied saying that they are anticipating a slow down that should see the labour force better balanced and after some time wage growth will diminish and that it will take time. He could have also referenced unit labour costs that indicate compensation has been rising while productivity has been tumbling for some time.

Immigration’s Effects

Macklem was asked whether he sees higher immigration as being more inflationary or disinflationary in the short run. He answered that on net it is roughly neutral but it affects different parts of the economy differently. He said immigration is adding to labour supply and easing some of the labour shortages and could ease the cost structures of companies. On the other hand, he said, these new entrants are new consumers and so they add to demand. It's hard to know exactly what the net effect is but the main message is that it is adding to both demand and supply but if you are already in excess demand then it is supporting persistence of excess demand. In my opinion, immigration is more of a demand impulse effect than a supply side effect on inflation but I can see the Governor’s reticence to say as much even if absent any supporting evidence for his stance. US studies show that the immigrant wage elasticity effect after controlling for other influences upon wages is roughly zero, yet new arrivals immediately add to consumption and housing.

Nonsense About Mortgage Interest and CPI

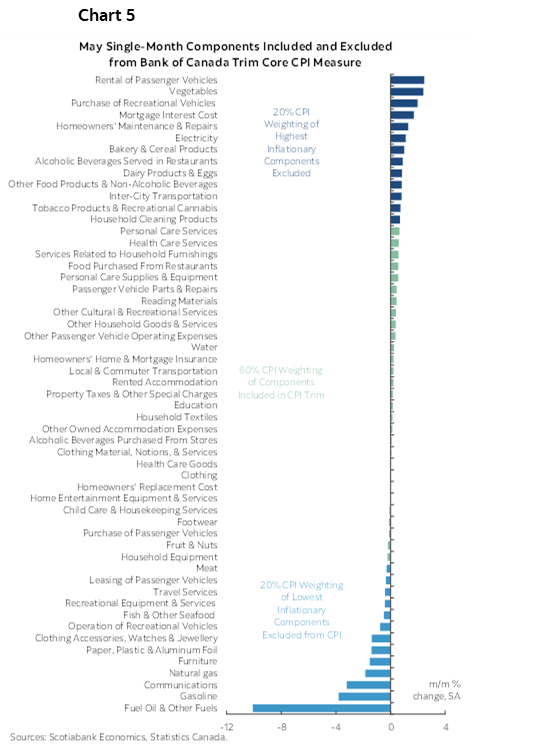

At several points in the presser the Governor was asked whether he understood that raising the policy rate is putting upward pressure upon mortgage interest costs that are included in CPI and why he doesn’t get that after removing this component they are on target. I’ve said it multiple times now, but this is just bad economics. Macklem’s answer was correct but incomplete in that he said that about half the basket is up by over 5% y/y which indicates high breadth and that we can’t cherry pick removal of some hot components like mortgage interest or some components that are a drag like year-over-year gasoline price changes and instead have to look at the breadth of the gains in totality. He could have also simply said mortgage interest is not even a factor in its central tendency measures of inflation. Trimmed mean excludes mortgage interest in the upper 20% of the distribution of prices (chart 5, next page) and weighted median uses the weighted 50th percentile price which is not mortgage interest.

Macklem was asked about the potential upside surprises to inflation that he seems to be so worried about. His answer was a good one in that he said “There are always going to be surprises but if you don't get inflation back to 2% and then you get an upside surprise then you are back to 4. The surprises should most of the time be within 1–3%. If inflation is fluctuating within that range then Canadians don't need to worry about fluctuations in their cost of living so they can invest and save and spend with confidence. It's not that there are some specific upside risks but the point is to get inflation back to 2% so you have to worry less about those.”

Nobody asked—and the Governor didn’t offer anything—about whether rate hikes continue to be needed because Canadian governments are overspending. Of course they are, with probably around a percentage point or more of the rate hikes to date being driven by fiscal stimulus. In the past, Macklem has avoided locking horns with the Feds but most BoC observers probably know the answer to the question.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.