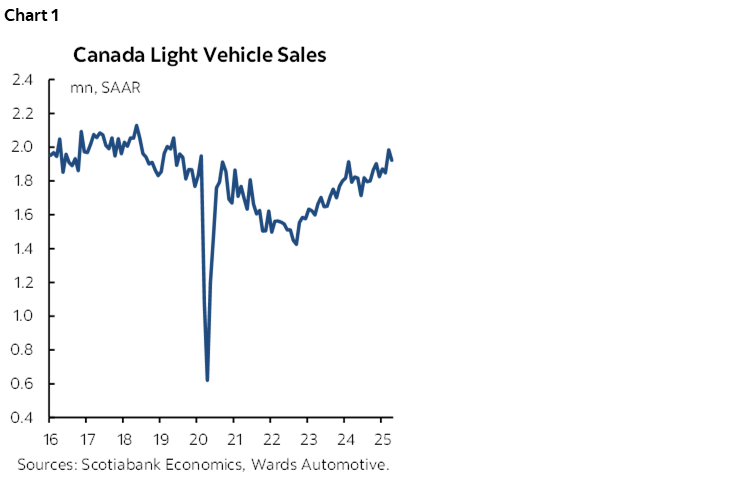

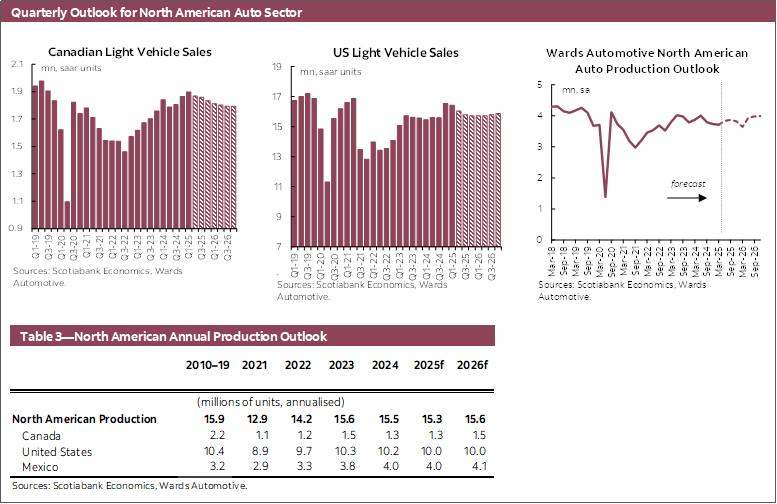

CANADA: SPRING SALES REMAIN ELEVATED BUT FACE DOWNSIDE RISKS

Canadian auto sales slowed by -3.2% month-over-month to 1.92 mn units at a seasonally adjusted annualized rate (SAAR) in April according to Wards Automotive (chart 1).

Seasonally adjusted sales surged 7.3% m/m to 1.98 mn (SAAR) in March before pulling back to 1.92 mn (SAAR) in April as demand was likely pulled forward with consumers potentially front-running any US-Canada tariff effects. While new vehicle sales may be elevated in the near term, the sales rate will likely slow in the coming months after front-running effects and risk possibly declining further should the impact of tariffs start to strengthen such as through distortions to supply from changes to production plans, higher prices as tariff costs get passed through to consumers, or weighing on economic activity and labour markets through increased uncertainty and direct tariff headwinds. On April 15th, the Canadian Department of Finance announced measures to support Canadian businesses and entities impacted by tariffs which includes a performance-based remission framework for automakers subject to conditions such as continuing to manufacture vehicles in Canada.

The Bank of Canada held the policy rate at 2.75%, the midpoint of their estimated neutral range, on April 16th after having cut the policy rate each meeting since June 2024 from a peak 5%. The future path for interest rates is largely uncertain as the BoC assesses incoming data and developments and their implications to maintaining inflation near 2%, noting that monetary policy cannot offset the impacts of a trade war and that they will support economic growth while ensuring that inflation remains well controlled. Our latest forecast expects the Bank of Canada to hold the policy rate unchanged through 2025 and could see the policy rate decline over time against weakening growth and partial retaliation, versus holding or hiking should upside risks to inflation warrant tightening.

Our outlook for Canadian light vehicle sales of 1.86 mn in 2025 and 1.80 in 2026 faces large uncertainty, notably in the outer years to reflect developments and pressures that the tariffs will have on the automotive sector and overall economic activity.

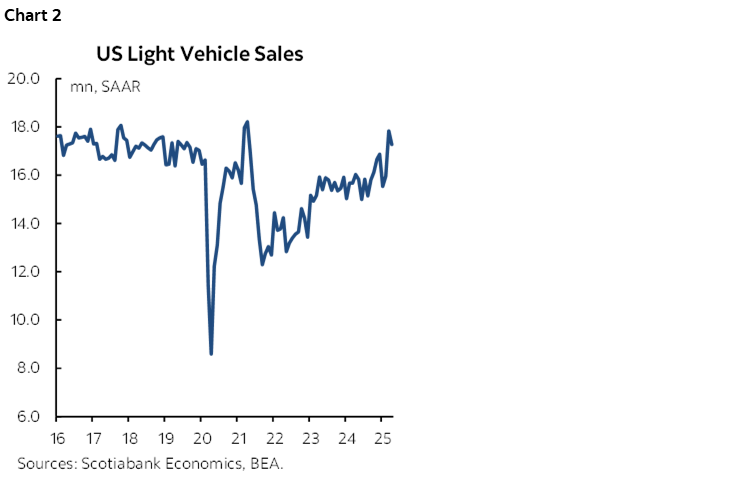

UNITED STATES: SALES REMAIN ELEVATED AMID FRONT-RUNNING TARIFF RISKS

US auto sales in April fell by -3.1% month-over-month in seasonally adjusted terms to 17.3 mn units at an annualized rate (chart 2). While auto sales slowed in April, US consumers continue to front-run tariff effects with the three-month moving average (3mma) increasing to 17.0 mn (SAAR) in April, the highest three-month sales rate since May 2021, and up from 16.5 mn (SAAR) in Q4 last year.

At the end of April and early May, the US revised some of their policies to limit some of the potential impacts of tariffs on the domestic economy. These include removing the stacking effect on select goods that were subject to multiple tariffs such that they only face one tariff rate rather than a combined rate. The US also introduced a rebate program worth 3.75% of the MSRP on US-made vehicles sold in the US that declines to 2.75% a year later and requires a larger share of US-content in the vehicle. Additionally, the US is pausing for two years the 25% tariffs on CUSMA-compliant auto parts imports from Canada and Mexico that were expected to come into effect on May 3rd. While these adjustments provide some relief to the automotive sector compared to what was previously announced, there remains large uncertainty around future developments and potential impacts to North American automotive supply chains.

Our outlook for US auto sales of 16.0 mn in 2025 and 15.8 mn in 2026 faces large uncertainty as tariffs imposed on a large swath of goods imported to the US weigh on the economic outlook.

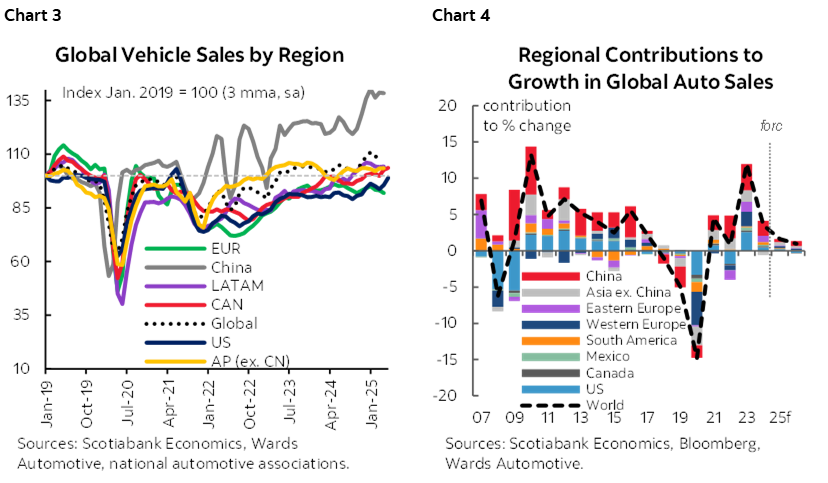

GLOBAL AUTO SALES: SOFT Q1 SALES RATE IN MOST REGIONS TO START 2025

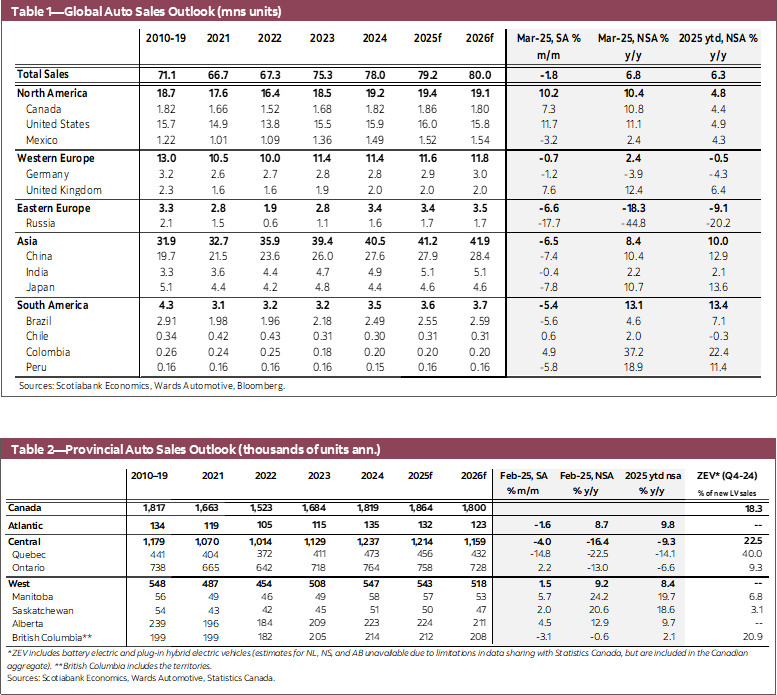

Global auto sales decreased -1.8% m/m (SA) in March, contracting in three of the past four months when adjusting for seasonality (chart 3). The slower sales rate to start the year was broad based at the regional level and resulted in Q1 automotive sales contracting by -1.3% quarter-over-quarter (SA). Auto sales in western Europe increased 0.8% q/q in Q1, as sales were mixed at the country level, increasing in five of the 15 countries covered, and have mostly trended sideways since October. Meanwhile, auto sales in eastern Europe fell by -17.1% q/q, the first quarterly seasonally adjusted contraction since Q2-2022. Asia Pacific auto sales were down by -0.9% q/q, as softening was broad based across the region, including a -1.4% q/q decline in China, the largest market in the region by volume. In Latin America, auto sales fell by -1.4% q/q, with the quarterly seasonally adjusted sales rate declining for the first time since Q4-2023. Our outlook for global vehicle sales is 1.6% in 2025 and 1.0% in 2026, with the risks potentially weighing more to the downside as tariffs pose headwinds to global growth (chart 4).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.