CANADA: MULTIPLE HEADWINDS CONTINUE TO WEIGH ON SALES

Canadian auto sales fell 2.2% (sa) in July to the pace of 1.57 mn seasonally adjusted annualized units according to Wards Automotive. This second consecutive seasonally adjusted monthly decline brought the annualized sales rate below 1.6 mn SAAR units for the first time this year and to the slowest pace since October 2022 of 1.52 mn SAAR sales. The average price for a new vehicle in Canada rose above $66 k in June according to AutoTrader’s price index, up more than 20% and 40% from the same period in 2022 and 2021 respectively. This large percentage increase in vehicle prices greatly outpaces the average hourly wage gains for permanent employees over the same period even as labour markets prove remarkably resilient. In addition to these elevated prices, the average new car loan rate has been above 7% since October 2022 through May 2023, which is further weighing on consumers buying power and sentiment. With the Bank of Canada forecasted to hold the Overnight rate unchanged at 5.00% through the remainder of this year, and not begin cutting rates until Q2 2024, financing costs are likely to remain elevated in the near term. High prices and financing costs, along with still limited supply continue to weigh on new vehicle sales in the near term. Our outlook for Canadian vehicle sales is 1.67 mn units in 2023 and expect sales to pick up to 1.75 mn in 2024 as inventory and rate pressures ease, underpinned by growing pent up demand against an aging vehicle stock and rapid population growth.

UNITED STATES: IMPROVING SUPPLY MITIGATED BY ELEVATED FINANCING RATES

US auto sales held steady in July at 15.7 mn SAAR units, up 0.5% (sa) from the month prior. New vehicle sales are continuing their general trend recovery but year-to-date sales remain -8.7% (nsa) compared to the first seven months of 2019. Supply-side factors are improving as North American light vehicle production averaged 17.1 mn SAAR units in Q2 2023, the highest quarterly pace since Q2 2019. However, even with production back at a pre-pandemic pace it will take time for inventories to build back up from their currently low levels to fully ease supply-side pressures. Meanwhile, the US Federal Reserve hiked the upper bound of the Fed Funds rate to 5.50% at their monetary policy rate meeting in July. As these policy rates get priced into market rates, the average new car loan rate increased for the 11th consecutive month, reaching 7.47% in July, the highest level since May 2009 in the aftermath of the Global Financial Crisis. We do not forecast policy rate cuts to begin until Q2 2024, which is likely to keep financing costs elevated in the near term. A resilient labour market is supporting employment and wage gains, with nearly 8.5 mn job openings from the June JOLTS data implying there are 1.4 job openings per unemployed, above the average ratio of 1.1 in 2019. We forecast that US vehicle sales will be 15.5 mn units in 2023 amid supply and inventory constraints and improve to 16.6 mn units in 2024.

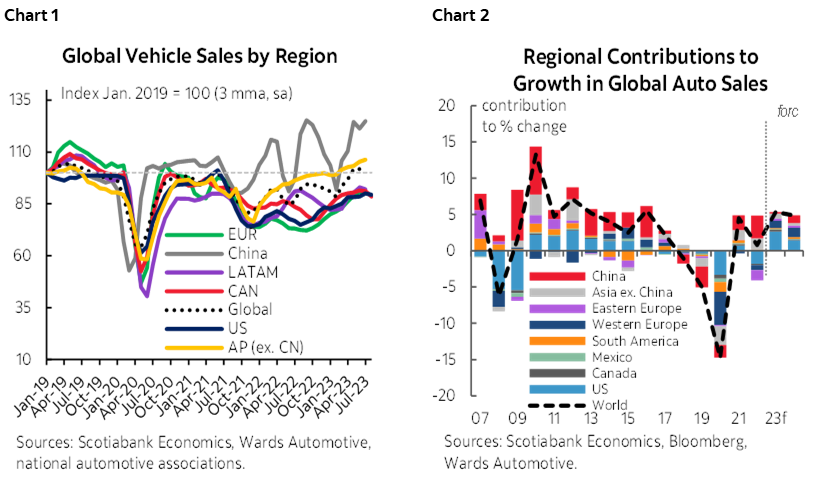

GLOBAL AUTO SALES: UNEVEN GROWTH THROUGH 2023H1

Global auto sales have wrapped up Q2 2023, registering positive seasonally adjusted sales growth across Latin America, Asia Pacific, and Europe at the regional level (chart 1). Sales through the first half of 2023 have been the strongest in Europe in percentage terms, increasing 18% ytd (nsa) compared to the first half of 2022. Though this is largely attributable to the fact that sales are still nearly 25% below 2019 levels and have the most ground to make up amongst the four regions covered. Asia Pacific auto sales are up 9.6% ytd (nsa) compared to 2022 and exceed 2019 sales by 7.9% ytd (nsa). A large portion of the recovery in vehicle sales is attributable to both China and India, the largest AP markets not including Japan, which are up 11% and 21% ytd (nsa) compared to 2019 sales respectively. Meanwhile, Japanese auto sales are -11% ytd (nsa) below 2019 levels. The recovery in Latin American auto sales has been uneven, up 1.3% ytd (nsa) compared to 2022 but nearly 20% below 2019 sales at the regional level. While sales have reached pre-pandemic numbers in Argentina and Peru, and are -2% in Mexico, sales in remain 25% below 2019 levels for Brazil and Colombia, and 15% below 2019 levels for Chile. Our global auto sales outlook forecasts vehicle sales increasing 5.3% in 2023 and 4.9% in 2024 (chart 2).

ELECTRIC VEHICLE SALES IN CANADA: LOWER BEV SALES PARTIALLY OFFSET BY PHEV SALES IN 2023Q1

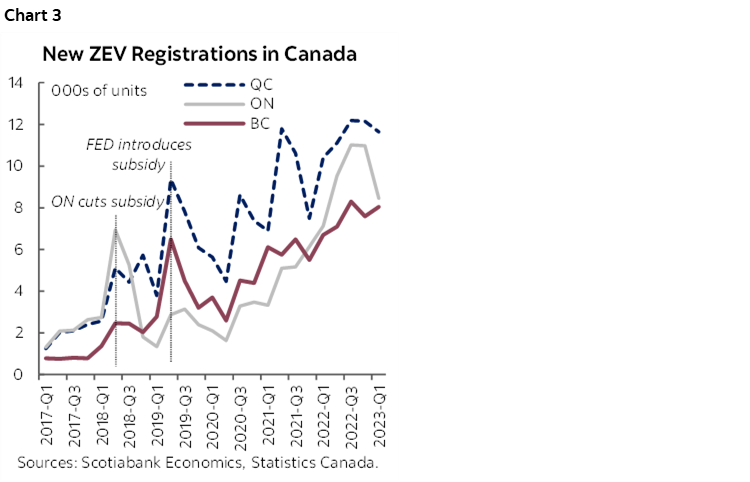

Momentum in Canadian electric vehicle (EV) sales slowed in the first quarter of 2023, accounting for 8.6% of all vehicles sales. With EV sales down from 9.6% the previous quarter and slightly above the 8.2% of all new motor vehicle registrations in 2022, there is still a long road ahead to meet Canada’s interim ZEV sales target of 20% by 2026 and 100% target by 2035. The lower share of EV sales in Q1 was the result of a 14.3% q/q decline in battery EVs which was partially offset by a 19.7% q/q increase in plug-in hybrid EV sales. Ontario, the largest province by vehicle sales, saw a nearly 30% decline in battery EVs which resulted in ZEV sales accounting for only 5.9% of all new motor vehicle sales in Q1 2023, down from 8.1% in Q4 2022. In Quebec, a 19.8% q/q increase in plug-in hybrid EVs along with a 7.8% q/q decline in total vehicles resulted in the share of ZEVs increasing to 14.5% in Q1 2023, up from 13.9% the previous quarter. BC’s new vehicle registrations for battery electric and plug-in hybrid electric were up 2.6% q/q and 23.4% respectively, though were offset by higher total sales resulting in the share of new ZEVs falling to 17.9% from 18.6% in Q4 (chart 3). Canada’s iZEV Incentive Program caps incentive eligibility for passenger cars with an MSRP up to $65 k, and up to $70 k MSRP for light trucks and similar sized vehicles. As the average price of a new vehicle surpassed $66 k in June based on AutoTrader’s price index, rising vehicle prices will limit which vehicles are eligible for the incentives and likely poses medium term headwind towards meeting Canada’s 100% ZEV sales target by 2035. Meanwhile, still limited inventory and high costs of financing pose as short-term headwinds in an environment of pent-up demand.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.