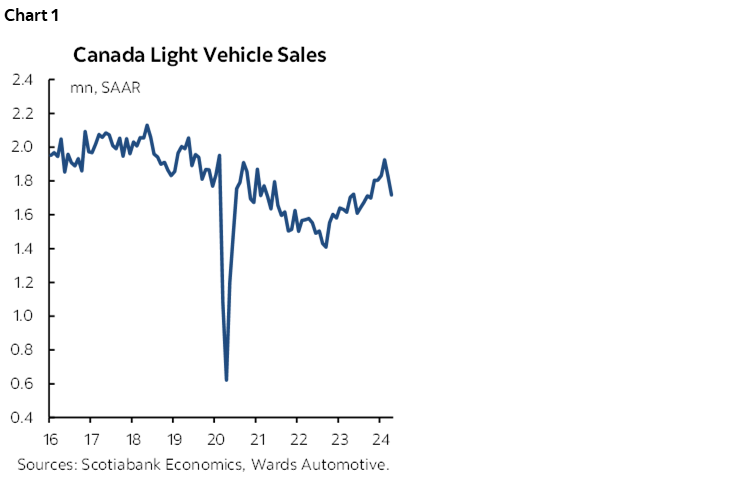

CANADA: SLOWDOWN FOLLOWING UPWARD REVISIONS TO Q1

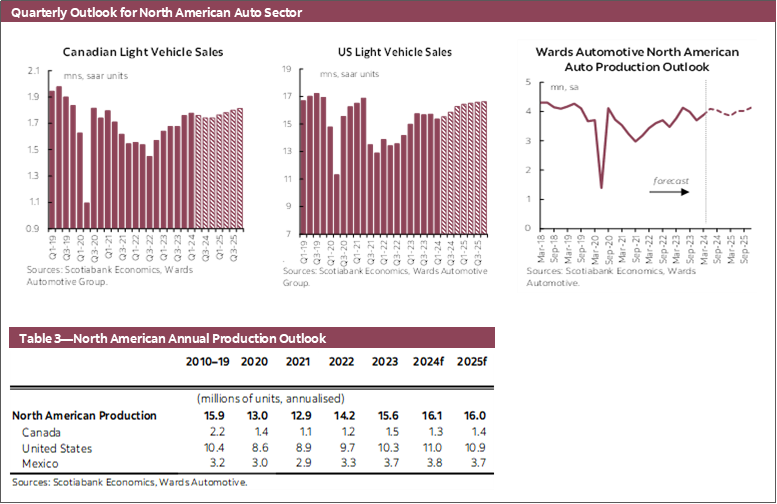

Canadian auto sales slowed for a second consecutive month to 1.72 mn units at a seasonally adjusted annualized rate (-5.8% m/m SA) in April according to Wards Automotive (chart 1). A considerable portion of the slowdown is attributable to the upward revision of non-seasonally adjusted sales for January through March that were revised upwards by 4.5% to 6.6% each. The updated figures suggest that auto sales averaged 1.86 mn (SAAR) in Q1 as opposed to the previously reported 1.78 mn (SAAR) units. While Canadian auto sales had a strong start to the year and are up 10.6% year-to-date (NSA) compared to 2023 they slowed considerably in April, up 1.2% from the same month last year, which is down from the 12% to 19% y/y for each of the five prior months. The average auto loan rate eased to 8.1% by the end of February, slightly down from 8.3% in November 2023. However, remaining at or above 8% for the seventh consecutive month as interest rates weigh on demand. At their April policy rate meeting, the Bank of Canada (BoC) held the overnight rate at 5.0% and acknowledged that recent data has been encouraging but they need to see further progress before they can begin rate cuts. Our view is that the BoC will begin easing their policy rate in Q3, with their policy rate ending 2024 at 4.25% and further easing beyond. Our outlook for Canadian auto sales is 1.75 mn units in 2024, and expect sales to increase to 1.79 mn in 2025 as interest rate headwinds ease.

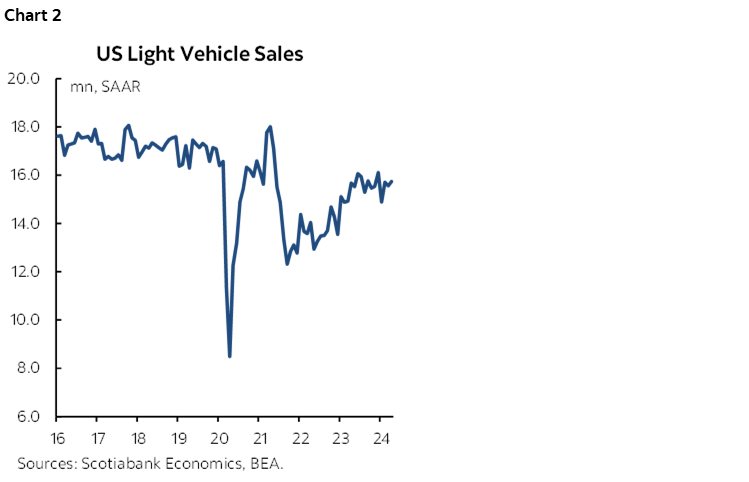

UNITED STATES: STEADY SALES AS SUPPLY AND DEMAND REBALANCE

US auto sales increased 1.1% m/m to 15.7 mn (SAAR) units in April (chart 2). Light vehicle sales in the US have fluctuated from month-to-month, with slight easing from Q2-2023, but generally held steady since the second half of last year. The six month moving average has fluctuated between 15.5 mn and 15.7 mn (SAAR) for ten consecutive months now. This period of consistency in the automotive sector is allowing supply and demand to rebalance. North American light vehicle production continues to support the recovery in supply-side factors, averaging 15.7 mn (SAAR) units in Q1, up 5.8% from the Q4 seasonally adjusted pace when production was reduced owing to labour strikes in the fall. US light vehicle inventories continue to build up from pandemic lows. In seasonally adjusted terms, inventories have increased in 24 of the past 26 months, but they are still less than 70% of pre-pandemic levels. The average 48-month new car loan rate has fluctuated around 7.85% for the three months ending in April, as interest rates weigh on economic activity. Persistence in monthly measures of core inflation have pushed back on expectations for the Federal Reserve to ease their policy rate in the face of still strong economic activity and labour markets. We expect the Federal Reserve to continue holding their policy rate at 5.50%, with rate cuts beginning in Q3 and only 50 basis points of cuts this year and further cuts in 2025. Our outlook for US auto sales is 15.7 mn units in 2024 as elevated interest rates and still recovering inventories pose headwinds to demand and supply, increasing to 16.5 mn units in 2025 as these headwinds ease.

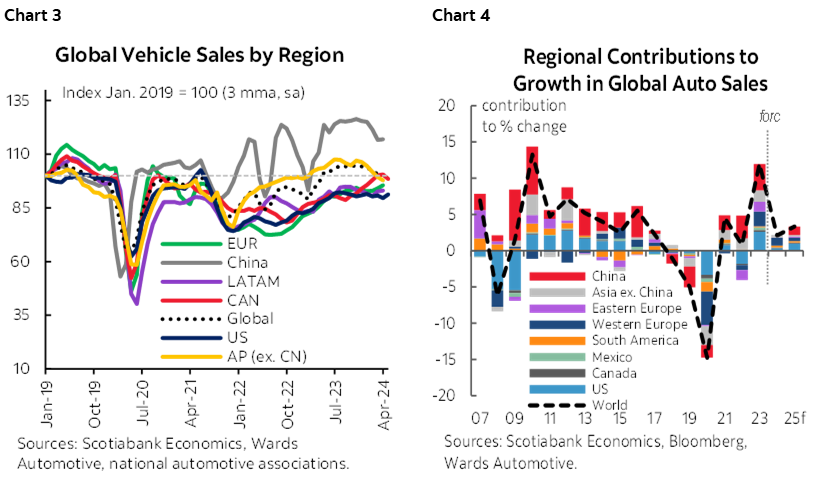

GLOBAL AUTO SALES: MIXED MOMENTUM IN Q1 TO START 2024

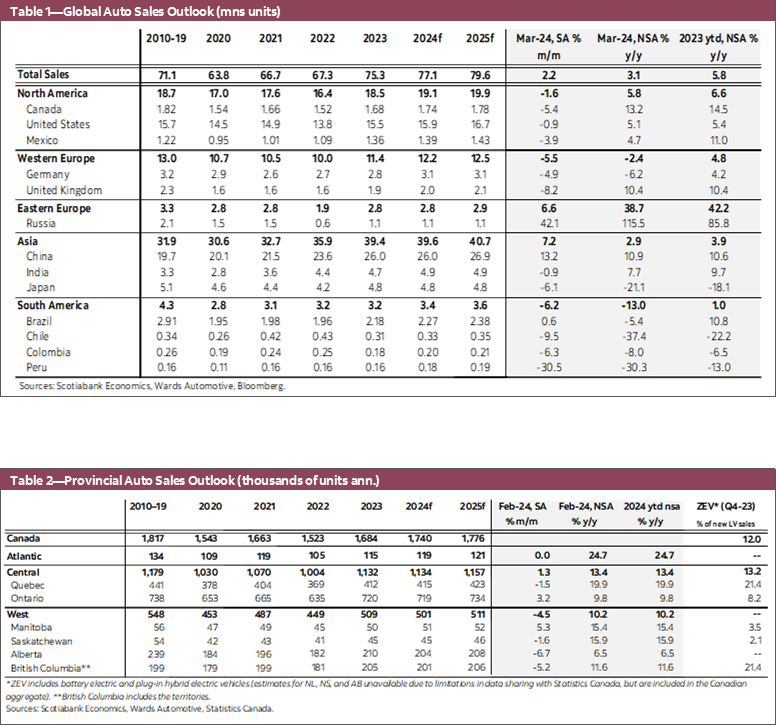

Global auto sales increased 2.0% m/m in March, marking back-to-back increases after having slowed the three prior months, as increased sales in Asia Pacific and eastern Europe were partially offset by slower sales elsewhere (chart 3). This small rebound coming off of declining levels towards the end of 2023 has led global auto sales to fall 3.0% q/q in Q1, with differences at the regional level. In the Asia Pacific region, Q1 auto sales fell 6.4% q/q as Chinese auto sales, which make up two-thirds of the region’s market share, slowed 6.5% q/q. Vehicle sales in four of the five other Asia Pacific countries covered all fell in Q1, increasing only in India (5.8% q/q) to start the year. In Western Europe, auto sales through Q1 increased 2.9% q/q with mixed details as sales increased in eight of the 15 countries covered. Of the major markets in the region, Q1 auto sales increased in Spain (13.7% q/q), Germany (4.1%), the UK (3.0%), were relatively unchanged in Italy (0.9%), and fell in France (-1.0%). And in eastern Europe, Q1 auto sales increased 3.1% q/q, up in the four countries covered and 2.7% in Russia. In Latin America, Q1 auto sales for the region were mostly higher, up 1.6% q/q, increasing in four of the six countries covered. Similar to the US, Mexico vehicle sales have come down slightly from their recent peak in mid-2023, having slowed 1.8% in Q1 to start the year. Our outlook for global auto sales forecasts an increase of 2.1% in 2024 and 3.3% in 2025 as elevated interest rates weigh on consumer spending and activity (chart 4).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.