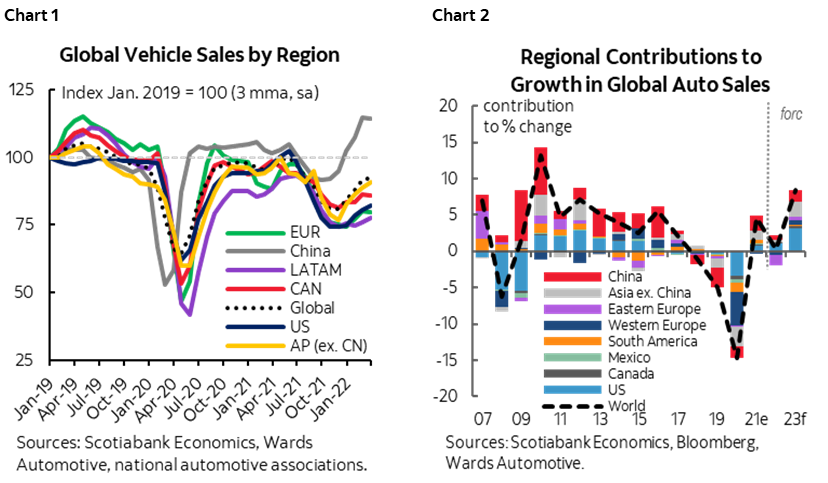

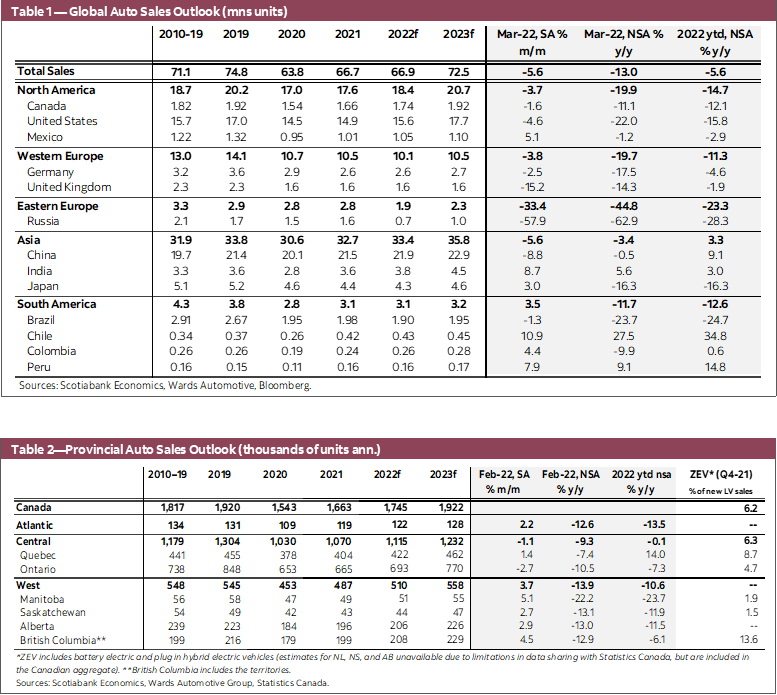

- Global auto sales fell by -5.6% m/m (sa) in March as new risks emerged, compounding new supply challenges (chart 1). Sales activity slid to a depressed level at 66.1 mn saar units—well below the 75.5 mn saar units in March 2021.

- Sales recovery in North America and Europe has been sluggish, as Russia’s invasion of Ukraine further clouded the outlook.

- Strong momentum in Asia Pacific markets led global recovery since last fall, as they rapidly recouped losses from the global shortage of semiconductors by February 2022. Recent lockdowns in China brought the country’s auto sales down by -8.8% m/m (sa) in March, dampening regional demand and production.

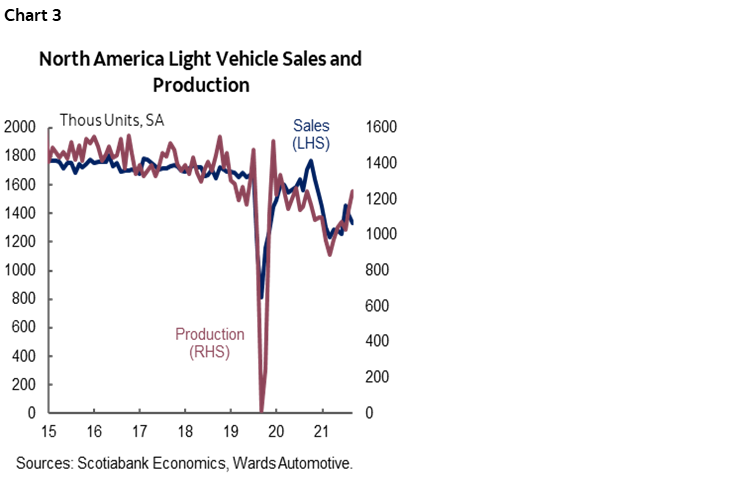

- Having revised down sales outlook in Europe last month, we maintain our global auto sales outlook (chart 2), but expect recent developments to bring more downside risks, including on Chinese sales.

- Pent-up demand and still-strong economic fundamentals should support auto sales in Canada and the US, though central banks’ pivot towards more aggressive policy tightening may take some steam out of sales, particularly the longer inventory shortages persist.

- Automakers and analysts further scaled back production forecasts for 2022 as headwinds mount. We expect limited inventory to persist and continue masking fundamental demand, while underpinning price pressures on new and used vehicles in Canada and the US over the foreseeable future.

NEW RISKS START TO MATERIALIZE

Global auto sales posted a -5.6% m/m (sa) decline in March, ending the five-month streak of slow recovery. Impacts of the Russian invasion of Ukraine are showing up in auto sales around the world—particularly pronounced in Russia (-57.9% y/y) and neighbouring markets—compounding already-strained supply chains in global auto production. Meanwhile, the new wave of COVID-19 lockdowns in China pulled down its auto sales by -8.8% m/m sa. Negative economic shocks could impose more downside risks to demand in Europe and China.

Albeit less affected by the direct shock, mild monthly contractions were observed in most large markets around the world. UK sales fell by -15.2% m/m (sa), followed by a -4.6% m/m (sa) decline in the US and -2.5% m/m (sa) in Germany (chart 1). Expectations of higher interest rates, along with weaker sentiment, may have curbed sales to a degree, but lack of supply still seems to be the constraining factor in North American markets, at least. J.D. Power, LMC Automotive and Cox Automotive all expect US sales to pull back again in April due to limited inventory in dealerships.

On top of pre-existing challenges, large-scale production disruptions further dampen production outlook. As anticipated in our last report, persistent geopolitical tension in Eastern Europe is likely to aggravate supply challenges and production costs. Chinese auto production has been hit by a series of factory closures since mid-March prompted by COVID-19 lockdowns. LMC Automotive estimates 8 mn units of production shortfalls in 2022—slightly improved from 2021—with most regions recouping some losses from the year prior except for Europe and China.

We maintain last month’s downward revision in the European auto sales outlook, but expect recent developments to increase downside risks, including on Chinese sales. Scotiabank Economics’ latest Economic Outlook on China (see here) discussed weakening consumer spending owing to the strict COVID-19 measures and rising unemployment, but highlighted the possibility for strong policy responses to follow. We will be monitoring closely developments in this market. Our outlook for Canadian and US auto sales had already incorporated a weak first quarter owing to limited inventory—and results met our expectations with sales in both markets standing at lacklustre levels of 1.6 mn units saar and 14 mn units saar, respectively, and consequently maintain our 2022 outlook for these markets (1.75 mn and 15.5 mn units, respectively) for now as we monitor developments. We continue to expect the US to drive global sales gains in 2022 and 2023, with the caveat that there is still plenty of further downside that could transpire.

A SLOW AND VOLATILE RECOVERY IN NORTH AMERICA

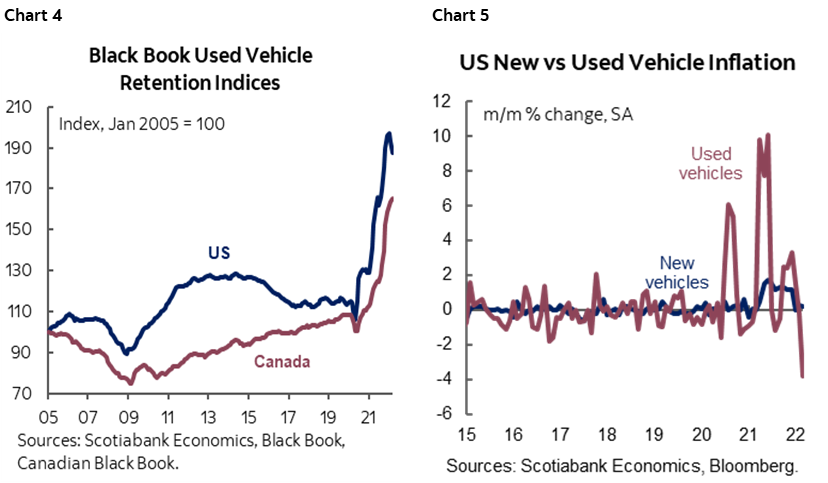

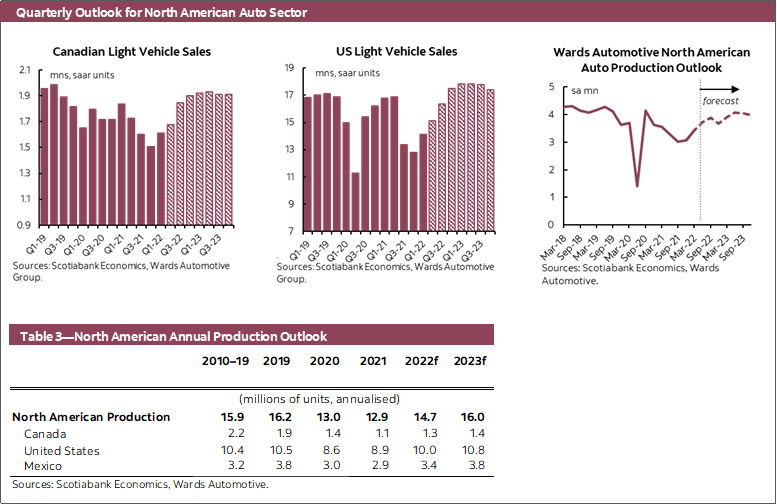

As of the first quarter, North American production is still tracking a slow recovery, while bracing for more volatility ahead. Despite the January pullback, North American auto output was up +10.4% q/q (sa) since Q4, reflecting a solid recovery in supply chains against strong economic activity. That said, emerging uncertainties pertaining to the Russia-Ukraine conflict and Chinese lockdowns add downside risk to the North American auto production recovery, which is not expected to fully recover till at least next year.

Pent-up demand continues to build up in North American markets as limited inventory constrains otherwise still-solid demand. Domestic production moved in lock-step with sales since last September (chart 3). And since the share of domestic auto production remained relatively stable at around 78% of new vehicle purchases, the current speed of recovery is not enough to absorb the pent-up demand accumulated during 2021. In the US, inventory level seems to have bottomed, but is still hovering below half of the level trending in spring 2021. With strong headwinds putting both domestic and foreign production under high pressure, we continue to believe that supply will remain tight for both new and used vehicles.

More aggressive policy tightening by central banks in Canada and the US could curb some consumption, but excess demand pressure should continue with tight labour markets, rising wages, and solid household balance sheets. Though March CPI inflation surprised on the upside (8.5% y/y in the US, and 6.7% y/y in Canada), there has not been significant weakening in consumer confidence. The Conference Board US Consumer Confidence Index ticked down only slightly in April, and spending expectations remained stable. Canadian consumers anticipate higher consumption on a 12-month horizon, as indicated by the first quarter Canadian Survey of Consumer Expectations (CSCE), though stale readings warrant some caution. The weekly Bloomberg Nanos Canadian Confidence Index saw marginal improvement in April, hovering above the long-term average.

CAR OWNERSHIP TO REMAIN EXPENSIVE

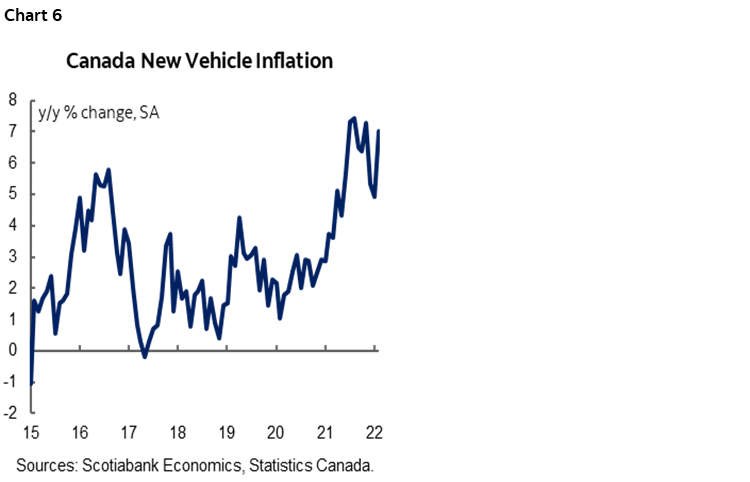

Early signs of easing in used vehicle price pressures are welcomed yet too early to call trend. Black Book’s US retention index fell in the past two months (chart 4), while consumer prices for used vehicles also recorded m/m declines during the same period (chart 5). The Canadian retention index continued to rise to a record level, yet Canadian Black Book’s weekly wholesale price tracking softened in April. This is likely temporary as headwinds in the tight new vehicle market continue to mount. Even with the decline in the past two months, US used vehicle retention index is still 33% higher than in March 2021. We expect the acceleration in used vehicle pricing to slow—possibly even modestly decline over the horizon from the extraordinary present levels—but we see a floor under pricing given limited supply and potentially even higher demand as economic conditions soften over the horizon given the traditional cyclicality of used vehicles.

New vehicle prices are still elevated. In Canada, new vehicle prices, as measured by CPI, accelerated by 1.6% m/m in March, 7% higher than in same month a year prior and still strained by supply chain disruptions (chart 6). With stronger inventory recovery south of the border, new vehicle prices stabilized in February, before picking up again in March. Even with shipping prices declining in 2022, the ongoing recovery in complex supply chains, coupled with high raw material prices and rising labour costs will likely continue to keep pressure on new vehicle prices.

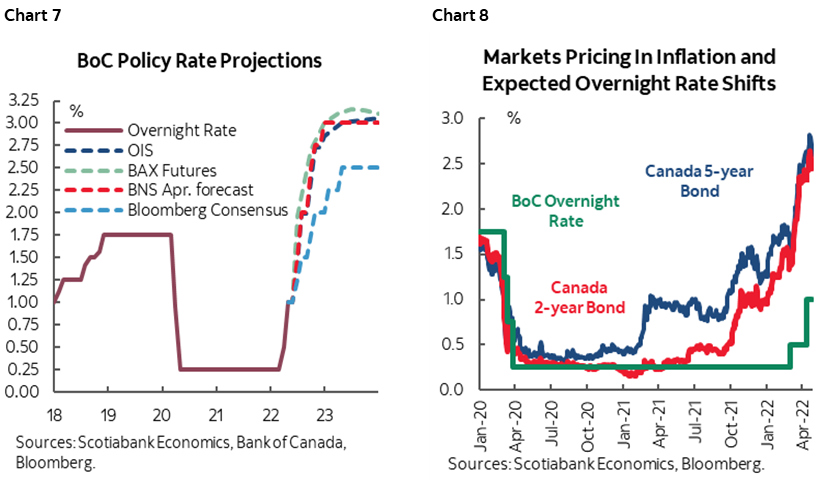

Financing costs are expected to rise further and faster as central banks consider more rate hikes. Scotiabank Economics has led consensus in calling more aggressive policy tightening, forecasting a series of hikes that would bring the overnight rate to 3.00% by 2023. The market is pricing in a similar outlook (chart 7). Canada’s Treasury yields went up further since the Bank of Canada delivered a 50 bps rate hike on April 13th, pricing in more hawkish monetary policy directions (chart 8). Rising Treasury yields continue to put upward pressure on auto loan rates, adding to car-owning households’ debt servicing burden. In the US, we also expect the Federal Reserve to make a 50 bps move at the May meeting, and follow a similar hiking path to a terminal rate of 3.00% by early-2023. (See here for details on Scotiabank Economics’ latest economic outlook including baseline assumptions.)

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.