- Chile: Fuel price increases were not fully captured in April—stronger increases in transportation services are likely in May

- Peru: Economic expectations internalize the local and international environment, as expected

CHILE: FUEL PRICE INCREASES WERE NOT FULLY CAPTURED IN APRIL—STRONGER INCREASES IN TRANSPORTATION SERVICES ARE LIKELY IN MAY

April CPI came in at 1.3% m/m (4.0% y/y), below survey expectations (FTS: 1.6%), market consensus (1.5%), and our forecast (1.7%). Around 75% of the monthly print was explained solely by higher gasoline and diesel prices (0.98 ppts contribution), alongside additional upside from increases in liquefied gas and piped gas prices. While we observed indirect effects across some goods and services (e.g., higher bread prices, interurban bus fares, rents), there were significant declines in airfares (domestic and international). These declines likely reflect the INE’s price collection methodology rather than a genuine price compression by the industry. Given that we have identified price increases in these services, we see upside risks to May inflation, driven by indirect effects not yet captured and indexation channels, particularly affecting services inflation.

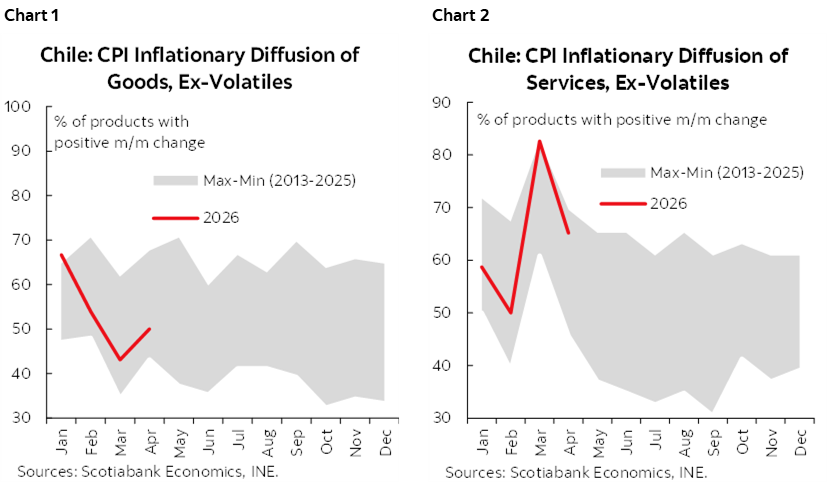

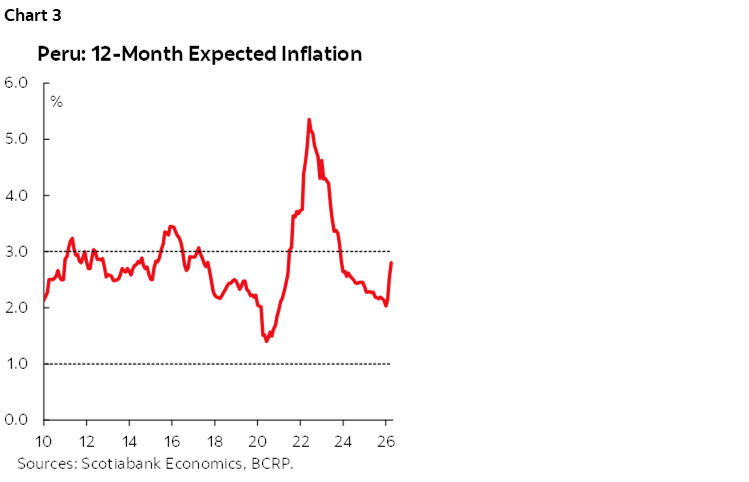

April CPI did not yet exhibit broad-based increases in goods, and only limited pass-through into services. Inflation diffusion, both for headline and CPI excluding volatile items, remained at the lower end of its historical range, largely explained by the low share of goods showing price increases—mostly concentrated in food (charts 1 and 2). This raises concerns about potential lagged pass-through into May, especially as core inflation ex-volatile remains contained (+0.5% m/m) despite the significant oil price shock.

The 2.3% cumulative inflation over the last two months is likely to trigger indexation effects in the coming months. Approximately 30% of the CPI basket consists of items whose pricing depends on past inflation (regulated and indexed components), including rents, financial expenses, and insurance. These categories have so far not shown significant adjustments despite the March–April CPI accumulation, but increases are highly likely in the near term. Absent a meaningful decline in domestic fuel prices, headline inflation could approach 5% y/y by mid-year.

—Aníbal Alarcón

PERU: ECONOMIC EXPECTATIONS INTERNALIZE THE LOCAL AND INTERNATIONAL ENVIRONMENT, AS EXPECTED

The Central Reserve Bank of Peru has published its Macroeconomic Expectations Report, based on surveys of economic agents from the financial system, economic analysts, and non-financial corporations. We observe that expectations are increasingly internalizing the effects of the conflict in the Middle East and, domestically, political and electoral uncertainty. The largest adjustments are observed in financial variables, while business expectations have deteriorated, although they remain within expansionary territory.

Regarding economic activity, the expected GDP growth rate for 2026 remains unchanged, within a range of 2.9% to 3.1%, slightly below our projection of 3.2%.

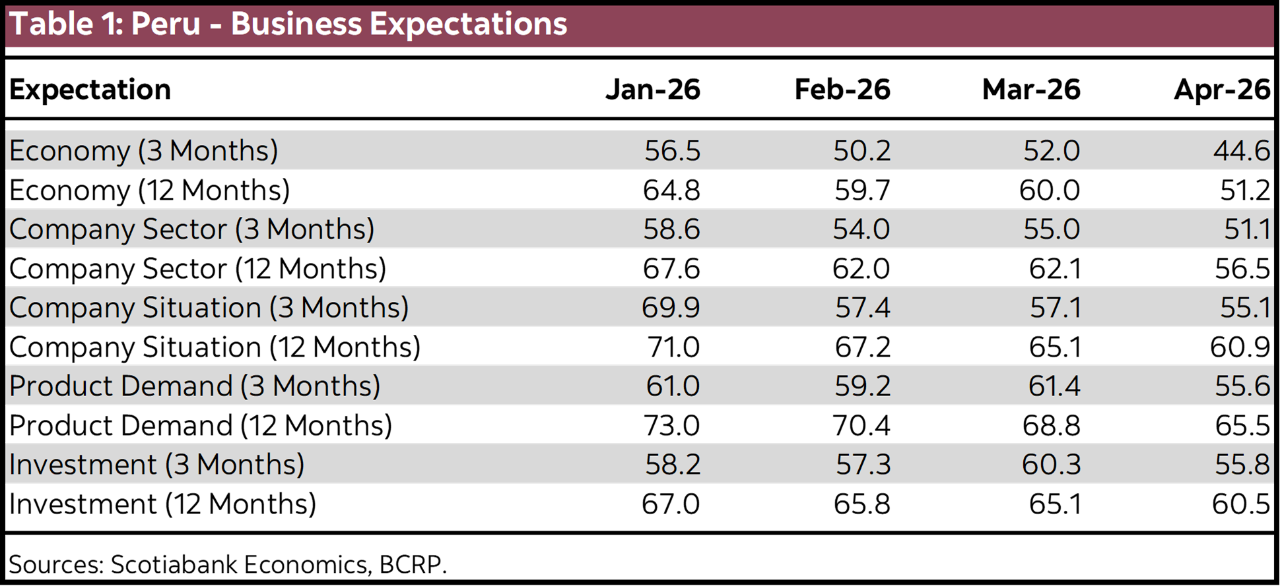

Twelve-month inflation expectations have increased again, rising from 2.5% in March to 2.8% in April, remaining within the target range (1.0%-3.0%) (chart 3). Inflation expectations for 2026 have also risen, widening to a range between 2.5% and 3.2%—compared to a range of 2.3% to 2.8% in March—while expectations for 2027 have increased to 2.5%, up from 2.2%–2.3% in March. We project inflation to close this year at 3.2% and to decline to 2.0% by 2027, under the assumption that international oil prices begin to ease next month. Otherwise, inflationary pressures would likely remain elevated.

Exchange rate expectations have also increased for the end of this year, reaching a range of PEN 3.43 to PEN 3.50 per US dollar, compared to a March range of PEN 3.38 to PEN 3.45. We are maintaining our forecast of PEN 3.35 per US dollar, under a scenario in which the new government preserves an investment-friendly stance.

Finally, business expectations—measured across 12 indicators—and assessments of current conditions—based on six indicators—have deteriorated in most components (table 1). This outcome is consistent with prevailing local and international conditions; nevertheless, indicators continue to remain within optimistic territory.

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.