- Mexico: Headline inflation shows mixed dynamics as PPI points to cooling upstream pressures

- Peru: Strong start—transport infrastructure investment accelerates in Q1-26

MEXICO: HEADLINE INFLATION SHOWS MIXED DYNAMICS AS PPI POINTS TO COOLING UPSTREAM PRESSURES

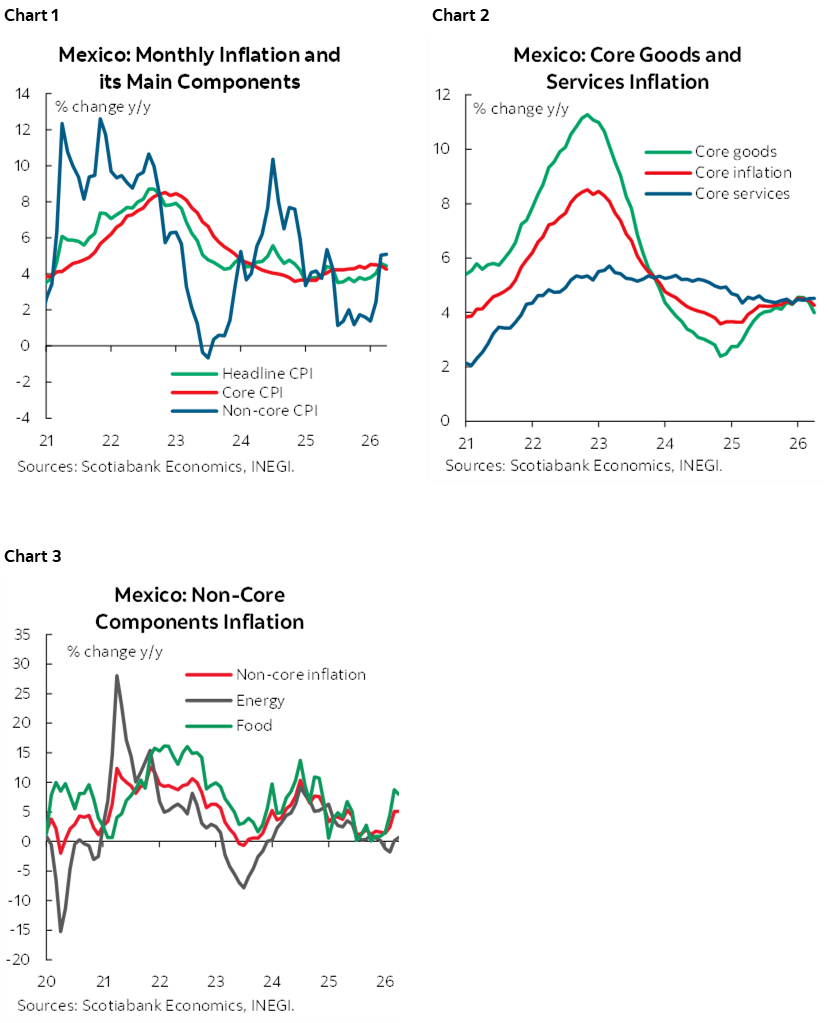

In April, headline inflation was revised downward, declining from 4.59% to 4.45%, and it remained below the consensus forecast of 4.54% (chart 1). Core inflation eased from 4.45% to 4.26%, in line with the consensus expectation. Within its components, goods inflation fell from 4.38% to 3.99%, while services continued to show pressures, reaching 4.52% from 4.51% previously (chart 2). Meanwhile, non-core inflation remained elevated, (chart 3) increasing to 5.08% from 5.05%, driven by a sharp rise in agricultural prices (7.98%), particularly fruits and vegetables (21.43%). Among the items with the greatest upward impact —ranked by incidence— tomatoes remained prominent with a monthly increase of 19.25%, followed by serrano chili peppers at 36.27% and owner-occupied housing at 0.31%. In contrast, electricity, green tomatoes, and chicken recorded price declines during the month. On a sequential monthly basis, headline inflation rose 0.20%, core inflation increased 0.31%, and non-core inflation declined by 0.18%.

The National Producer Price Index slowed its pace in April, declining from an annual increase of 2.77% to 2.56%. By sector, a notable contraction of -3.94% was observed in primary activities, while services slightly moderated their growth, from 4.00% to 3.98%.

Within industrial activities, these remained unchanged at 2.22%, with increases of 4.15% in construction and only 0.31% in manufacturing, albeit with significant disparities. Particularly noteworthy were the strong gains in basic metal industries (22.24%), alongside declines in computer equipment manufacturing (-8.47%) and machinery and equipment manufacturing (-7.57%).

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

PERU: STRONG START—TRANSPORT INFRASTRUCTURE INVESTMENT ACCELERATES IN Q1-26

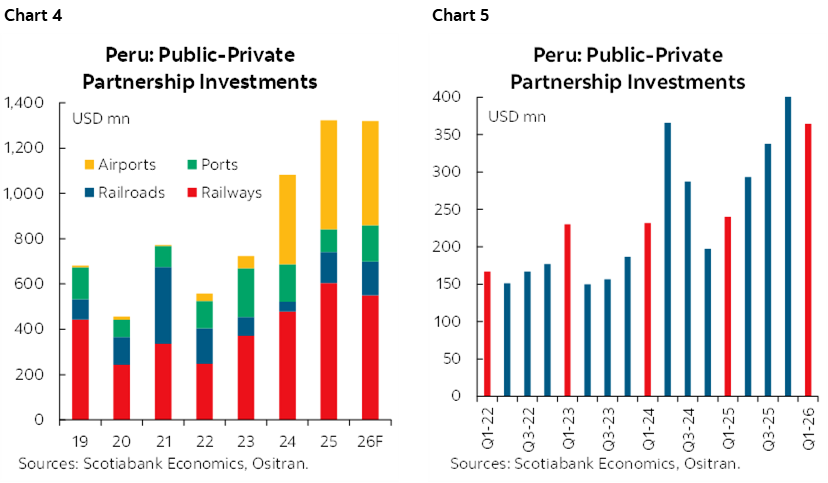

As of the end of the first quarter of 2026 (Q1-26), recognized investment in concessioned transport infrastructure reached US$364 million, up 52% year-over-year compared to Q1-25, according to the Transport Infrastructure Investment Supervisory Agency (Ositrán). Investment recognized in February alone amounted to US$166 million, the highest level since December 2025. Both results came slightly above expectations.

Looking ahead, we expect investment across concessioned projects to remain dynamic in the coming months. For full-year 2026, we maintain our forecast of US$1.3 billion in recognized investment, marking the third consecutive year in which investment exceeds the US$1 billion threshold. That said, upside risks remain, given several investment announcements that could be incorporated into our baseline projection.

By segment, we expect total investment to be led by rail infrastructure, with execution projected at slightly above US$550 million in 2026—primarily driven by the Lima Metro Line 2 project—broadly in line with the average of the past three years. This would be followed by airport infrastructure, with investment expected to exceed US$460 million, based on Ositrán data. Port infrastructure would contribute slightly more than US$160 million, while road infrastructure investment is projected to surpass US$130 million, close to the average observed over the past four years.

Investment in Q1-26

As noted above, total recognized investment in transport infrastructure reached US$364 million in Q1-26, marking the strongest start to a year in recent periods (see charts 4–5). Execution was mainly driven by investments in projects such as the expansion of Jorge Chávez International Airport (US$192 million), Lima Metro Line 2 (US$126 million), the IIRSA Norte highway project (US$11.2 million), and Road Network No. 6 (US$8.1 million).

Key Projects

Within the rail infrastructure segment, the most prominent project remains Lima Metro Line 2, which has reached a physical progress of over 80% across the full alignment—including Line 2 and the Line 4 branch, totaling 35 km. Of the 27 km of tunnels planned for Line 2, more than 25 km have already been completed. Progress has also accelerated in recent months on the Line 4 section (8 km), where the tunnel boring machine has reached 53% completion. Investment has been directed toward the procurement of electromechanical equipment, station materials, tunnel lining segments, superstructure works for sections 1B and 2, installation of systems, and civil works at ventilation shafts and stations. In the airport segment, investments were primarily recognized in works at Jorge Chávez International Airport, as well as in the acquisition of equipment for the second group of regional airports (close to US$1 million). In ports, investment included complementary works for liquid bulk handling at the North Terminal of Callao (approximately US$4 million), with additional works expected in the coming months (corresponding to Stage 3A and expanded access for general cargo). Further investment was also recorded at the Port of Salaverry, where bulk storage capacity expansion is expected to be completed by end-2026. Finally, investment in concessioned roads included works on Road Network No. 6 (grade separations), IIRSA Norte (sections 1 and 3), the Autopista del Sol (works in Lambayeque), and IIRSA Sur – Section 4, including tunnel works and a bypass road.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.