- Peru: BCRP holds reference rate unchanged and sends a reassuring message on inflation

- Mexico: Industrial activity shows mixed signals; Formal employment rebounds in June; Heavy vehicles improve, but year-to-date balance remains weak

PERU: BCRP HOLDS REFERENCE RATE UNCHANGED AND SENDS A REASSURING MESSAGE ON INFLATION

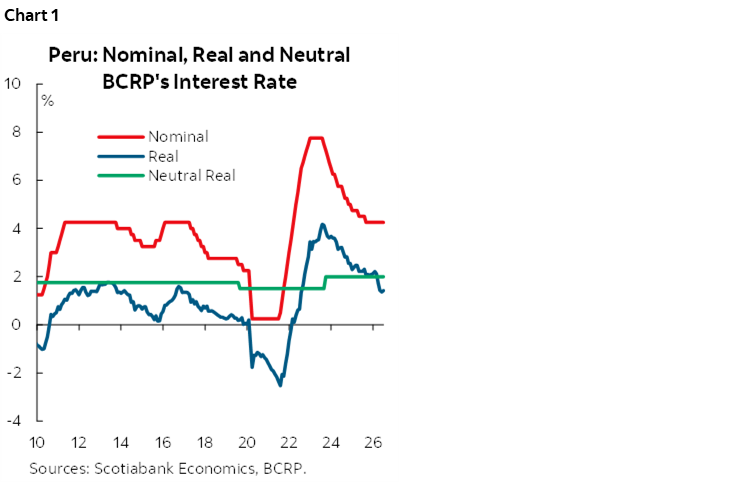

The Board of the Central Reserve Bank of Peru (BCRP) decided to keep its policy interest rate unchanged at 4.25% in July, marking the tenth consecutive month without adjustments (chart 1). This decision was in line with our expectations and with market consensus, as reflected in the Bloomberg median.

The most notable aspect of the statement is that annual headline inflation—currently at 4.0%—remains above the target range of 1%–3%, mainly due to the increase in fuel prices and their indirect effects in March and April. The BCRP also noted that, although annual core inflation stands at 4.5%, it sits at 1.6% year-on-year excluding the transportation component, remaining below the 2% midpoint of the target range since April of last year. This suggests that the recent increase in inflation has a specific and transitory origin and, for now, is not being reflected in the component that excludes the most volatile items.

In addition, the statement highlights the following points:

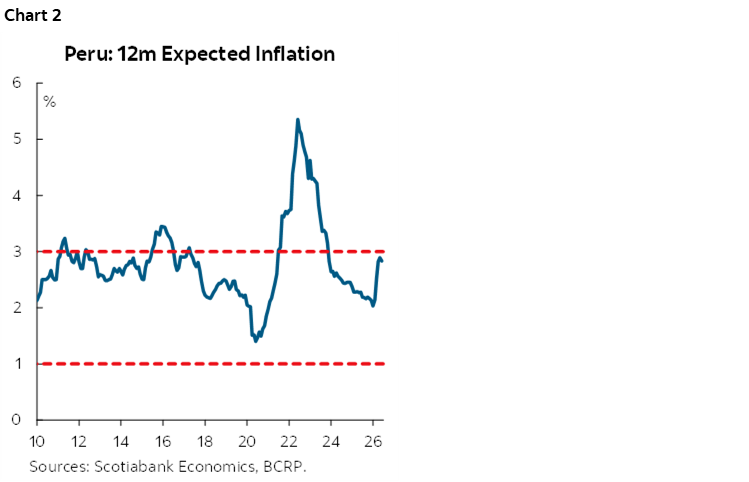

- Inflation: Monthly headline and core inflation in June stood at 0.23% and 0.08%, respectively, both consistent with the target range when annualized. The BCRP expects annual headline and core inflation to return to the target range over the projection horizon, 2026–2027. Meanwhile, 12-month inflation expectations declined from 2.9% in May to 2.8% in June (chart 2).

- Economic expectations: Leading indicators of economic activity for June continue to show solid performance. Regarding the BCRP’s survey, most current situation indicators improved, while expectations indicators posted a significant increase, with all of them standing in optimistic territory.

- International environment: Global risks have moderated recently, supported by the easing of geopolitical tensions in the Middle East and the relative normalization of supply conditions in the hydrocarbon market, which has led to a downward correction in international oil prices. However, uncertainty related to geopolitical tensions remains.

Looking ahead, our baseline scenario assumed that international oil prices would begin to moderate in June, as they indeed did. Under this assumption, we had projected inflation to decline to 3.2% by the end of 2026, still above the target range of 1%–3%. However, El Niño is adding renewed inflationary pressures, leading us to revise our 2026 inflation forecast upward to 3.7%. Inflation is expected to remain above 4.0% between January and February 2027, although the probability of it returning to the target range in March 2027 remains high, largely due to base effects.

—Ricardo Avila

MEXICO: INDUSTRIAL ACTIVITY SHOWS MIXED SIGNALS

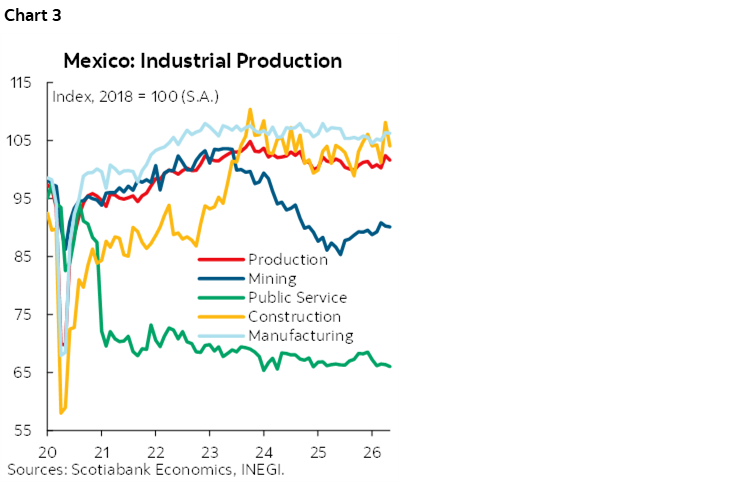

In May, the Monthly Indicator of Industrial Activity (IMAI) posted a 0.7% annual decline using original figures (chart 3). By component, annual performance showed mixed signals. Mining grew by 3.9%, supported by mining-related services, which expanded by 51.3%, while the rest of its components also remained in positive territory. Meanwhile, construction declined by 0.3%, although civil engineering works stood out with a 15.9% increase. Public utilities and manufacturing also posted declines of 0.9% and 1.5%, respectively, with manufacturing showing broad-based contractions across several branches. On a seasonally adjusted monthly basis, industrial activity fell by 0.8%, while mining declined by 0.1%, public utilities by 0.5%, construction by 3.7%, and manufacturing by 0.1%.

FORMAL EMPLOYMENT REBOUNDS IN JUNE

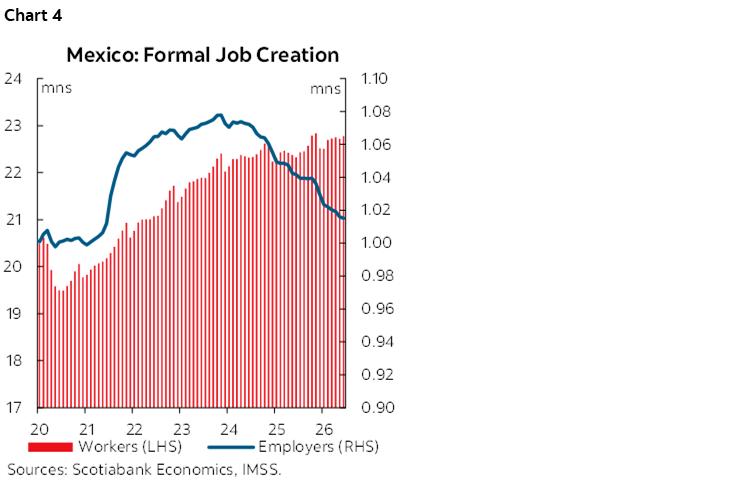

In June, jobs affiliated with social security increased by 61,023, following a previous decline of 29,922 positions (chart 4). As a result, total formal employment reached 22,779,704 jobs, equivalent to a 2.0% annual increase and marking the strongest momentum since July 2024. Meanwhile, the base contribution salary stood at MXN 669, representing a 6.4% nominal annual increase. On the other hand, the total number of employers continued to decline, with a monthly decrease of 899 registrations, bringing the total to 1,015,100 and implying an annual contraction of 2.5%.

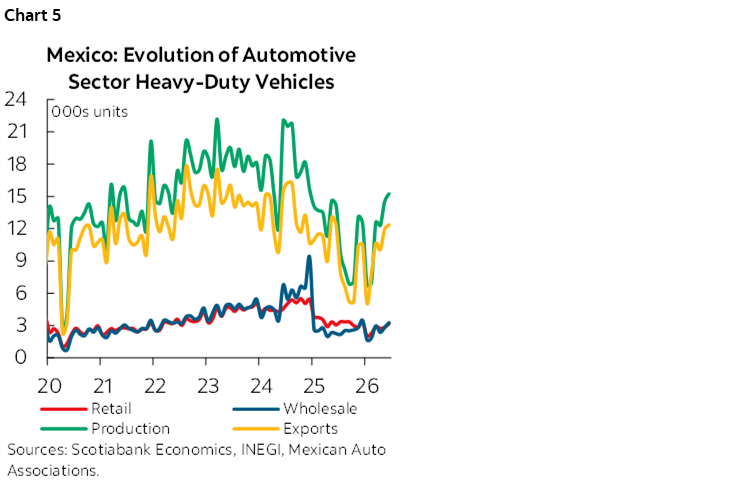

HEAVY VEHICLES IMPROVE, BUT YEAR-TO-DATE BALANCE REMAINS WEAK

In June, the heavy vehicles sector improved compared with previous months, posting positive annual growth across all components for the first time in several months (chart 5). Retail sales totaled 3,194 units, growing by 3.9% year 730 over year, while wholesale sales reached 3,278 units and surged by 45.5%. On the production side, 15,262 units were manufactured and 12, were exported, implying annual increases of 7.6% and 3.2%, respectively. However, the year-to-date balance remains weak: retail sales totaled 16,072 units, equivalent to a 21.8% decline; production reached 70,876 units, down 12.9%; and exports stood at 58,260 units, down 14.5%. The exception was wholesale sales, which accumulated 14,979 units and maintained a 3.0% increase.

Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.