- Chile: June CPI at 0% m/m surprises expectations and raises concerns over cost pressures

- Peru: Greater business optimism and more favourable macroeconomic expectations in June

CHILE: JUNE CPI AT 0% M/M SURPRISES EXPECTATIONS AND RAISES CONCERNS OVER COST PRESSURES

- Second-round and indexation effects re-emerge amid lingering cost pressures

June CPI came in at 0.0% m/m (4.3% y/y), surprising the market consensus, the Central Bank’s baseline scenario, and our own forecast (-0.2% m/m). The print revealed clear signs of second-round effects and mounting cost pressures that prevented goods prices from declining by magnitudes similar to those observed in previous years during the June Cyber sales season. We had expected second-round effects to become more evident starting in July; however, margin compression and firms’ growing perception of higher costs appear to have accelerated the process.

At Scotiabank, we have maintained our 2026 year-end inflation forecast at 4.5%, despite the decline in market inflation expectations observed in recent weeks. This CPI release reinforces our view, which remains well above market-implied inflation, consensus forecasts, and the Central Bank’s baseline scenario. The recent depreciation of the Chilean peso only adds further upside risk to our baseline outlook.

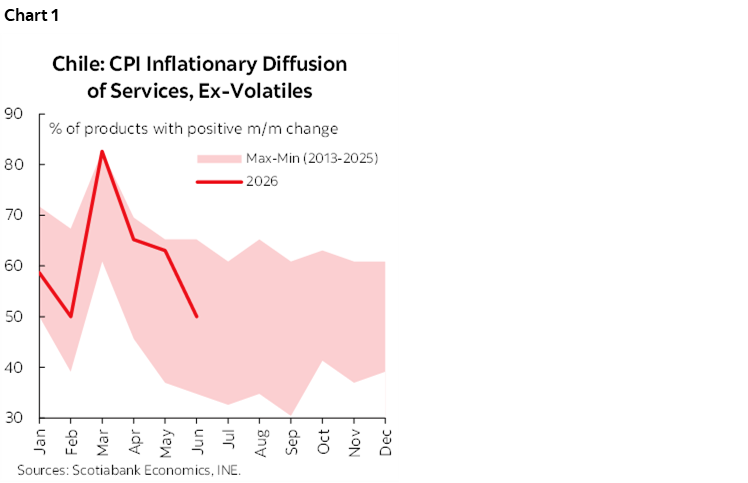

Headline CPI inflation breadth reached 43.1%, broadly in line with its historical average and consistent with what would typically be expected in a June reading affected by Cyber-related discounts. Nevertheless, the disinflationary impact from Cyber sales was notably smaller than in previous years. The main upside surprise came from the volatile components, particularly food prices. Although services inflation breadth returned to more normal levels (chart 1), several high-weight service categories posted price increases, suggesting the emergence of second-round effects associated with higher costs and reduced profit margins.

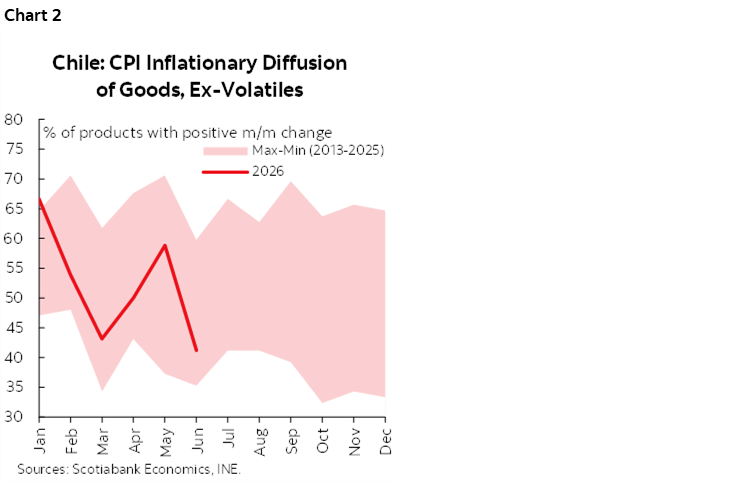

Core goods CPI excluding volatile items registered no monthly change, in a month when price declines are usually observed (chart 2). The impact of June Cyber sales has become more evident since 2023, generating uninterrupted declines in non-volatile goods prices during June, with the exception of this year. Likewise, inflation breadth among ex-volatile goods exceeded the levels observed in previous years, indicating that the weaker-than-expected price declines were not limited to a few specific products. Instead, the phenomenon was broad-based and is likely linked to rising cost pressures, a dynamic that had already been signaled by firms in the May Survey of Price Determinants and Expectations (EDEP) and the May Business Perceptions Report.

Fuel prices declined less than expected in June. Just as previous increases had been partially limited by margin compression among distributors, the latest declines appear to have been softened by a recovery in margins. Indeed, wholesale fuel price reductions announced by ENAP had pointed to larger declines in gasoline and diesel prices than those ultimately reported by the statistics agency (with gasoline prices falling 2.5%), accounting for part of the upside surprise in headline inflation.

Second-round, indirect, and indexation effects are becoming increasingly visible. Until now, these effects had been relatively limited and difficult to identify given the magnitude of the fuel price shock. However, the June CPI clearly shows stronger indexation effects in categories such as Financial Services (+0.8%) and Insurance (+4.2%), indirect effects in Domestic Package Tours (+19.4%) and Domestic Air Transport (+9.5%), and second-round effects in Food Purchased at Restaurants (+0.6%) and Alcoholic Beverages Purchased at Restaurants and Hotels (+1.0%). At Scotiabank, we expect additional pass-through awaits in several key goods and services categories, including rents, condominium fees, bread, domestic services, and healthcare services, among others.

Looking ahead, July CPI is likely to reflect higher electricity tariffs, a rebound in ex-volatile goods prices following the Cyber sales period, and further declines in fuel prices. Regarding the latter, we expect additional reductions in line with ENAP’s upcoming announcement, which we estimate could imply gasoline price declines of around CLP 100 per litre and diesel price declines of roughly CLP 150 per litre. As has occurred previously, these decreases may continue to be partially offset by distributors’ commercial pricing strategies. At this stage, we are working with a July CPI forecast in the 0.1% to 0.3% m/m range.

As for monetary policy implications, we continue to believe that the Central Bank could introduce the possibility of a rate cut at the September monetary policy meeting in response to weak economic activity, particularly in private consumption and employment. However, we do not expect an actual rate cut to materialize before there is clear evidence that second-round inflation effects are dissipating and that the Chilean peso is appreciating.

—Aníbal Alarcón

PERU: GREATER BUSINESS OPTIMISM AND MORE FAVOURABLE MACROECONOMIC EXPECTATIONS IN JUNE

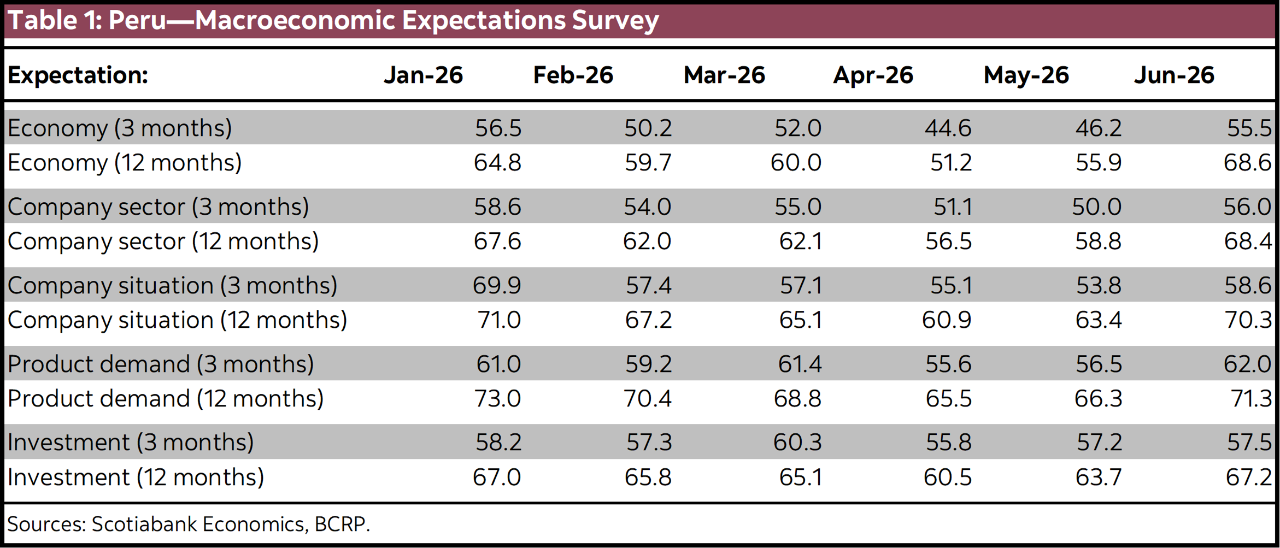

Recently, the Central Reserve Bank of Peru (BCRP) released its June Macroeconomic Expectations Survey. The results indicate an improvement in business confidence following the presidential runoff election, as well as more favourable expectations for key variables such as inflation and the exchange rate.

Since mid-June, markets had already been pricing in the outcome that the National Jury of Elections (JNE) officially confirmed on July 3rd: Keiko Fujimori’s victory in the presidential runoff. In this context, all business expectations indicators improved, reversing the deterioration observed in April and May following the first-round election results. This was largely because one of the candidates who advanced to the runoff was perceived by economic agents as posing a risk to the continuity of the current economic model.

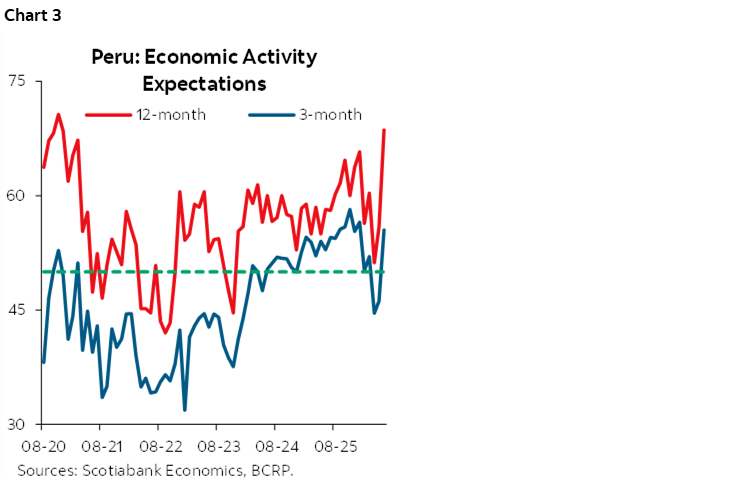

In particular, short-term economic expectations returned to pessimistic territory (below the 50-point threshold) in April—after remaining above that level for two years—but recovered and returned to optimistic territory in June (table 1). Meanwhile, 12-month economic expectations also weakened during April and May, although they remained within optimistic territory. However, they rebounded significantly in June (chart 3), reaching their highest level in five and a half years, the strongest reading since December 2020.

Likewise, the survey showed an improvement in economic agents’ expectations regarding the main macroeconomic indicators:

- 12-month inflation expectations: Declined slightly from 2.9% to 2.8%, in line with the recent decrease in international oil prices, while remaining within the central bank’s target range.

- 2026 inflation expectations: Although some dispersion remains, the expected range narrowed from 2.8%–3.5% to 2.8%–3.2%.

- 2026 economic growth expectations: Increased from a range of 3.0%–3.1% to 3.1%–3.2%. While the El Niño phenomenon could generate adverse effects on certain sectors of the economy, the strength of activities linked to domestic demand continues to support a favourable outlook for economic growth.

- Exchange rate expectations for end-2026: Declined from a range of PEN 3.46–3.50 per U.S. dollar to PEN 3.36–3.44 per U.S. dollar, consistent with stronger confidence among economic agents and a perception of lower political risk.

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.