- Peru: Cement sales maintain positive momentum, strengthening construction sector outlook

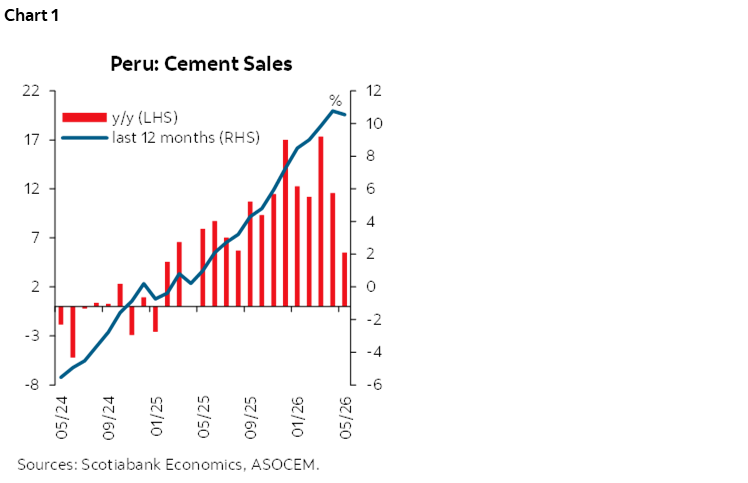

Cement sales reached nearly 1.2 million tons in May, up close to 8% year-on-year, according to INEI (Intituto Nacional de Estadistica e Informática). As a result, May posted the highest monthly volume since October 2025. In terms of annual growth, cement demand has maintained a sustained expansion trend since January 2025. Although May’s growth remained in single digits, it is important to note the base effect as May 2025 recorded one of the strongest growth rates of 2025 (chart 1).

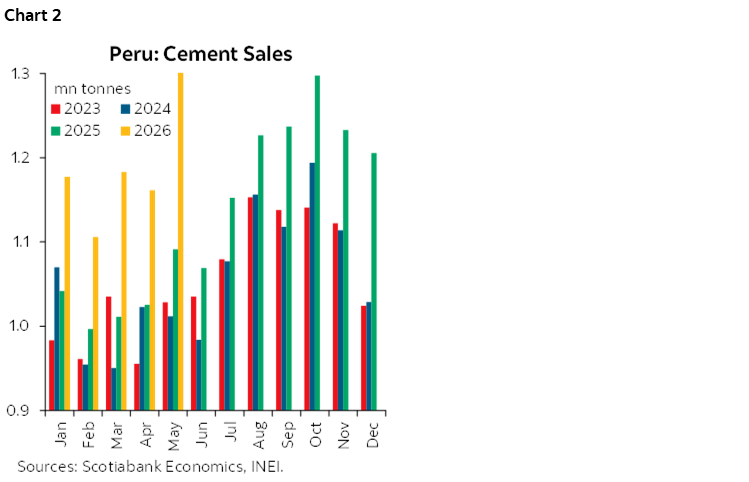

From a qualitative standpoint, May’s performance was another positive signal for the sector, particularly considering that the first round of the presidential elections introduced the possibility of changes in the country’s economic policy framework. While this development could have weighed more heavily on construction activity and cement demand, the impact proved limited, as cement dispatches reached their highest level of the year (chart 2).

Several factors supported cement demand in May. First, the self-construction segment remained resilient, supported by continued growth in formal private-sector employment, which expanded by 5% year-on-year in April, adding approximately 234,000 jobs. Second, the formal housing market continued to perform well, with new mortgage lending by the banking system increasing 6.4% year-on-year in April. Third, cement prices remained broadly stable, particularly in Lima, where the average retail price increased only marginally from PEN 30.4 per bag to PEN 31.1 per bag, according to INEI. Nonetheless, overall growth was partially offset by a 7% decline in public investment in May, mainly due to lower spending by the national government, partly offset by stronger execution by regional and local governments.

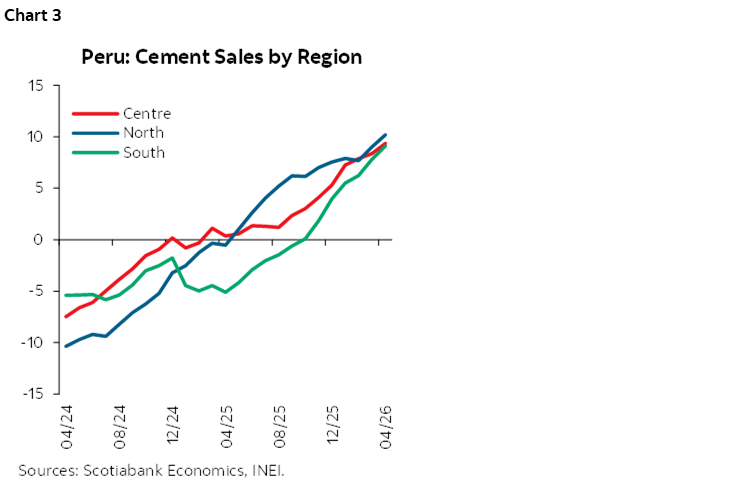

Through May, cement sales reached 5.6 million tons, 14% above year-ago levels. The drivers behind this expansion were broadly the same as those supporting April’s results. By region, cumulative cement sales through May showed the strongest growth in southern Peru (+15%), supported by mining-related investment activity, followed by the northern region (+13%), where self-construction remains particularly dynamic, and the central region (+12%), benefiting from ongoing real estate development and transportation infrastructure projects (chart 3).

2026 OUTLOOK

Based on cumulative results through May, we expect cement sales to expand at a pace broadly consistent with our 9.4% growth forecast for the overall construction sector in 2026.

This outlook is supported by three main factors. First, self-construction activity is expected to remain solid, underpinned by favourable formal employment trends and improving household income. Second, demand for higher-value residential properties—particularly in Lima—should remain strong, supported by mortgage rates that remain below the levels observed in previous years. Third, significant cement demand is expected from large-scale infrastructure projects, both through concession-based schemes and, to a lesser extent, projects executed under Peru’s Works for Taxes framework.

However, several risks could moderate cement demand. Public investment growth is expected to decelerate, particularly at the national government level, as the country transitions to a new administration in July. In addition, adverse weather conditions associated with a potential El Niño event, particularly during Q4-26, remain a key downside risk, as severe weather can delay construction activity and weaken household spending capacity.

Finally, the outlook also depends on maintaining relative geopolitical stability in the Strait of Hormuz. A renewed escalation of military tensions could trigger renewed volatility in global oil prices, increasing inflationary pressures on food and energy—especially fuel costs—and potentially constraining spending on labour and building materials within the self-construction segment.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.