- Peru: Infrastructure on track—concessions and works for taxes hit record levels

- Mexico: First GDP estimate surprises to the upside: The first GDP estimate for 2025 stands at 0.5% annually, above consensus expectations

- Chile: Seasonal improvement in employment, although labour‑market slack persists

PERU: INFRASTRUCTURE ON TRACK—CONCESSIONS AND WORKS FOR TAXES HIT RECORD LEVELS

Infrastructure investment in 2025 exceeded our expectations, considering both recognized investments in concessioned transport infrastructure and projects executed under the Works for Taxes (OxI) mechanism.

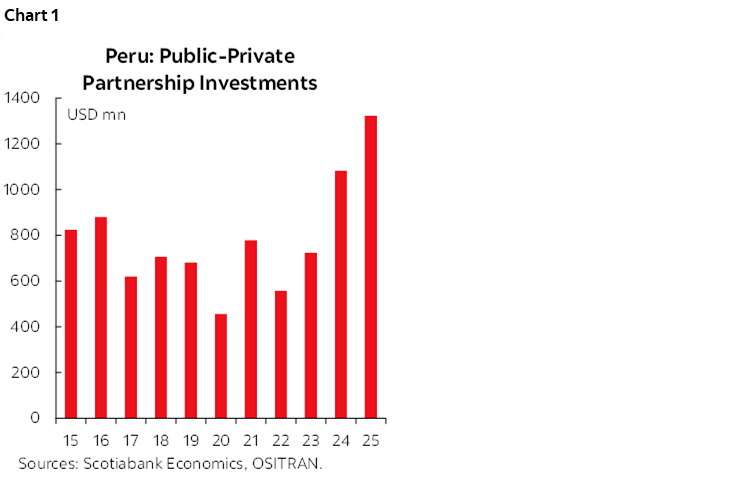

Infrastructure investment continues to show solid development potential, supported by the remaining investment pipeline across 34 transport concession projects awarded in previous years and supervised by the Supervisory Agency for Investment in Public Transport Infrastructure (Ositran) (chart 1). As of end-2025, roughly US$8 billion remain to be executed over the coming years—equivalent to 36% of the committed investment (US$22 billion). Additional momentum is expected from preliminary works in projects awarded by Proinversión between 2023 and 2025, totaling close to US$15 billion, including the Lima Outer Loop Road, Longitudinal de la Sierra–Section 4, and the San Juan de Marcona Port, among others. By July 2026, Proinversión aims to award approximately US$5.3 billion in new infrastructure projects.

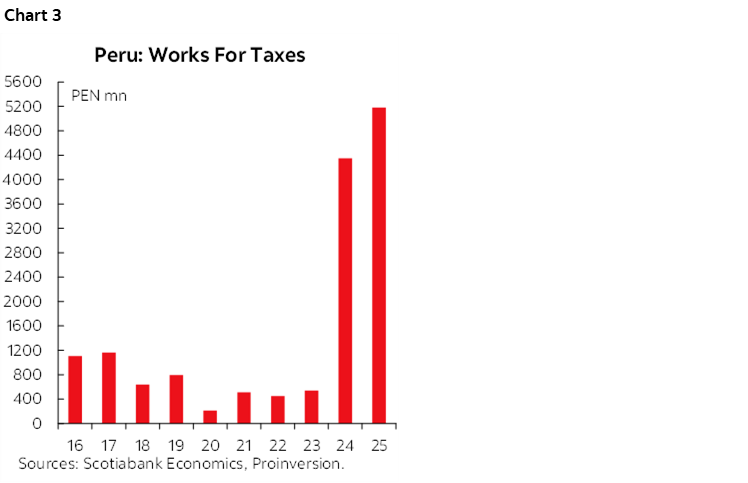

On the Works for Taxes front, we expect continued project awards in the coming months, following a record-breaking S/5.182 billion (US$1.45 billion) awarded in 2025—the highest level since the mechanism was created. For 2026, the award target stands at S/3 billion, although regional and local elections scheduled for October could delay new project decisions.

Over the medium term, the execution outlook remains favourable, supported by progress in prioritized addenda—worth US$15.8 billion—across railway, port, airport, road, and health infrastructure projects. Of this total, Proinversión expects to drive the signing of at least eight addenda valued at roughly US$8.429 billion in 2026. On the private side, we anticipate the start of works for the Port of Chancay-second stage in 2027, involving an estimated US$2.5 billion investment.

Concessioned Transport Infrastructure

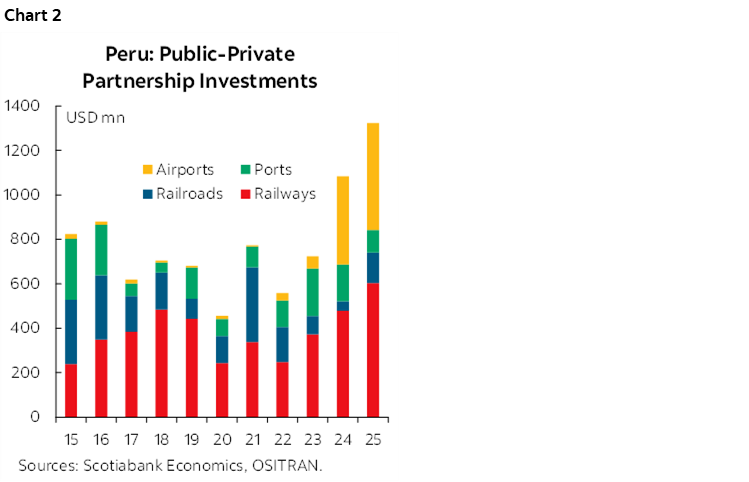

In 2025, Ositran recognized US$1.322 billion in transport infrastructure investments—the highest annual level on record. Execution was driven mainly by major projects such as Lima Metro – Line 2 (US$604 million)—the highest investment recorded in recent years—the expansion of Lima Airport 2nd Landing Strip (US$462 million), Callao Port–North Pier (US$78 million), Road Network No. 6 (US$53 million), the First Group of Regional Airports (US$19 million), and the San Martín–Pisco Port (US$10 million) (chart 2).

Works for Taxes

This project execution mechanism has gained considerable traction over the past two years (chart 3). In 2025, Proinversión reported OxI project awards totaling S/5.182 billion, up 21% from the previous year and marking the highest amount since the mechanism was created in 2009.

The largest awarded projects in 2025 included a sanitation project in Lima (Pucusana) for S/291 million, improvements to citizen security services in Chiclayo for S/163 million, and a transport project in Cusco worth S/132 million. This investment mechanism is expected to remain active in the coming months, supported by the S/353 million already awarded in 2026 as of January 19th, according to Proinversión.

Prioritized Addenda

According to Proinversión, the government plans to continue pushing forward the signing of fifteen prioritized project addenda aimed at unlocking approximately US$15.8 billion in new investments. As mentioned earlier, at least eight addenda worth around US$8.429 billion are expected to be signed in 2026 alone.

A recent milestone was the approval of Addendum No. 5 for the Matarani Port Terminal, enabling an additional US$700 million in new works on top of the US$291 million previously committed (Ositran reference investment). Other major addenda under evaluation include:

- Lima Metro Line 1 (US$3.231 billion),

- Callao Port–North Pier (US$1.3 billion),

- Torre Trecca (US$1.153 billion),

- Callao Port–South Pier (US$1.0 billion),

- Road Network No. 5 (US$1.0 billion).

These represent some of the most relevant upcoming expansions in Peru’s infrastructure pipeline.

Concession Projects Awarded in 2025

By the end of 2025, around US$3.6 billion in public-private partnership (PPP) projects had been awarded. The most notable was the concession contract for the Longitudinal de la Sierra–Section 4, signed in October, involving an estimated US$1.582 billion investment.

Also included was the awarding of the Ancón Industrial Park (US$1.261 billion) at year-end under the “Projects in Assets” modality, to be developed in five stages. Additionally, four electric transmission projects—part of Group 3 of the 2023–2032 Transmission Plan—were awarded in September, with a combined investment of US$323 million.

In July, the operation and maintenance concession for the new Villa El Salvador Emergency Hospital (Lima) was awarded, involving US$284 million. Two sanitation projects were also awarded: the wastewater treatment plants (WWTPs) in Chincha (January) and Puerto Maldonado (December), with investments of around US$130 million and US$150 million, respectively.

—Carlos Asmat

MEXICO: FIRST GDP ESTIMATE SURPRISES TO THE UPSIDE—THE FIRST GDP ESTIMATE FOR 2025 STANDS AT 0.5% ANNUALLY, ABOVE CONSENSUS EXPECTATIONS

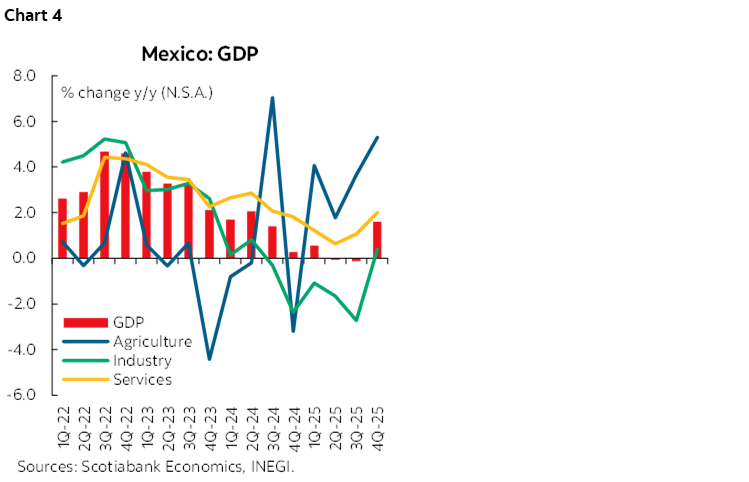

According to INEGI’s first GDP estimate, during the fourth quarter of 2025 economic activity grew by 1.6% annually in real terms, following stagnation and contractions in previous quarters (-0.1%). Internally, the increase was driven by a 5.3% expansion in primary activities. In this first estimate, secondary activities moved into positive territory at 0.4%. Meanwhile, services grew by 2.0%. Thus, in the accumulated data for 2025, GDP shows an advance of just 0.5%, slightly above consensus (0.4%), with a -1.3% decline in industry and increases of 1.2% and 3.7% in services and primary activities, respectively. Compared to the previous quarter, using seasonally adjusted series, GDP grew by 0.8%, driven by 0.9% growth in both industry and services, and a -2.7% drop in primary activities (chart 4).

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

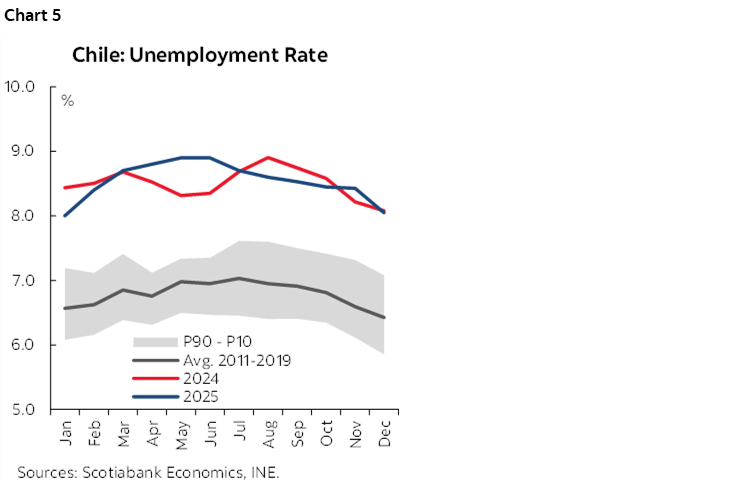

CHILE: SEASONAL IMPROVEMENT IN EMPLOYMENT, ALTHOUGH LABOUR‑MARKET SLACK PERSISTS

The unemployment rate reached 8.0% in the quarter ending in December, a figure that surprised the market on the upside (consensus: 8.3%) and represented a decline relative to the previous moving quarter (8.4%) (chart 5). The drop reflected the creation of 72k jobs versus an increase of 36k in the labour force. Although this is the second‑lowest unemployment rate of the year, the improvement is largely seasonal. In fact, the seasonally adjusted (SA) unemployment rate stood at 8.5%, still at the upper bound of the Central Bank’s NAIRU estimate (8–8.5%), signaling that labour‑market slack remains elevated.

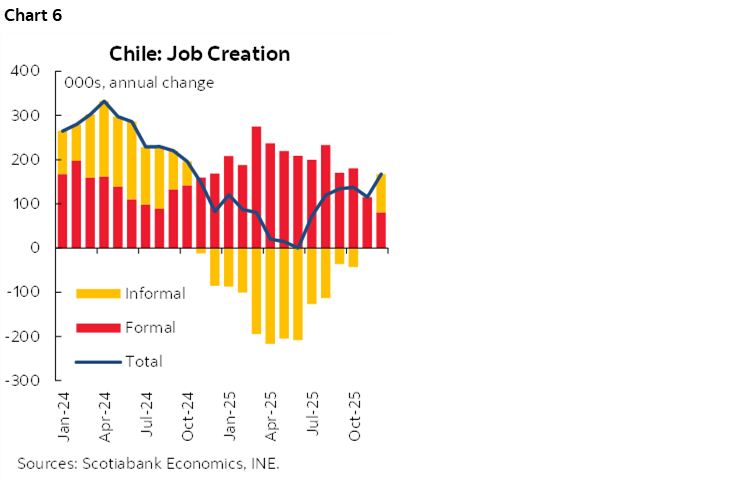

Manufacturing created 25k jobs, although this only compensates part of the losses seen in previous months. A large share of this job creation occurred in formal sectors and firms (14k), which is also consistent with stronger hiring of private‑sector employees. Similarly, employment in accommodation increased, mostly among the self‑employed, and strongly linked to seasonal demand. Although agriculture also added jobs—mostly private‑sector employees—the increase was weaker than typically observed at this time of the year.

Informal employment begins to regain share. After several quarters of year‑on‑year declines in informal employment, this category posted a meaningful increase again (+87k), while formal job creation continues to lose momentum (chart 6). By sector, informal job gains were concentrated in administrative services (+32k), health (+18k), and accommodation (+17k).

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.