- Mexico: Trade balance posts a USD 2.43 billion surplus in December

- Peru: After two years of non-compliance Peru meets fiscal deficit target

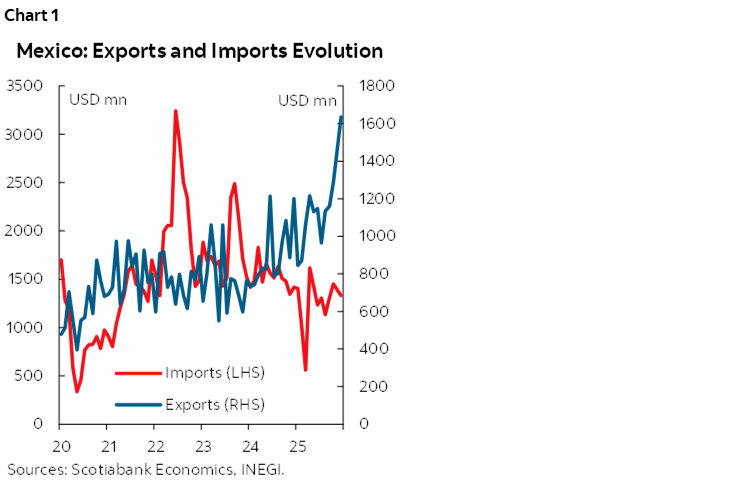

MEXICO: TRADE BALANCE POSTS A USD 2.43 BILLION SURPLUS IN DECEMBER

In December, the trade balance posted a surplus of 2.429 billion dollars, with significant annual increases in both exports and imports. In particular, exports accelerated from 7.9% to 17.2% year-over-year during December, driven by a strong rebound in manufacturing, although showing stagnation in automotive exports (0.8%) and continued sharp deterioration in oil exports (-33%). On the other hand, imports also rebounded, rising to 16.7% from 5.2% previously, led by consumer goods imports (25.3%), followed by intermediate goods (17.3%), while capital goods again recorded a decline (-0.6%). As a result, cumulative annual exports rose 7.6%, while imports increased by only 4.4%. Looking ahead, we believe that 2026 could begin with lower levels of trade, affected by international uncertainty and the imposition of tariffs in both Mexico and the United States.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

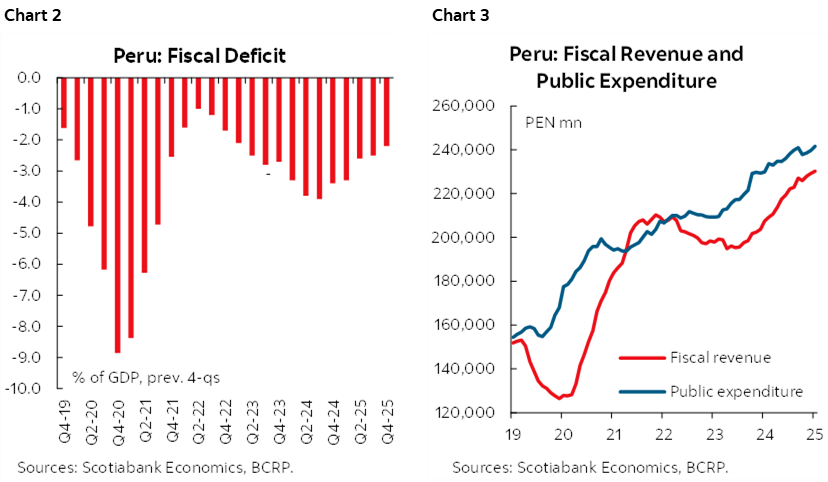

PERU: AFTER TWO YEARS OF NON-COMPLIANCE PERU MEETS FISCAL DEFICIT TARGET

The fiscal deficit reached an amount equivalent to 2.2% of GDP at the close of 2025, according to figures from the Central Reserve Bank (BCR). This figure not only shows a significant improvement compared to the 3.4% of GDP deficit recorded in 2024, but also that the government has met the official target for the first time since 2022.

The fiscal deficit target for 2026 is even more demanding (1.8% of GDP), in line with the objective of achieving the medium-term fiscal rule (1.0% of GDP from 2028 onward). Our projection is a fiscal deficit of 2.0% of GDP, lower than the 2.2% of 2025, but still above the official target. However, there are factors that could boost tax revenues above projections, such as consistently high prices for metals like copper and gold, and domestic demand growing faster than usual in an election year. Furthermore, the growth in public spending could moderate if the learning curve for the new national government authorities is relatively slow—the new government takes office at the end of July. If these assumptions hold true, and assuming no new capital injections into Petroperú, it is possible that the fiscal deficit target will be met again.

Evolution in 2025.

The reduction in the fiscal deficit was due to increased tax revenues and, to a lesser extent, to the slowdown in public spending.

Tax revenues totaled S/ 179.7 billion (+12.4%) in 2025, driven by higher collections from Income Tax, taxes linked to domestic demand—such as Value Added Tax (VAT)—and extraordinary income from the collection of tax debts from previous years.

Income Tax revenues (+20.2%) were boosted by higher collections from mining companies due to increased profits resulting from high mineral prices, particularly copper and gold. To a lesser extent, higher advance payments from companies in the financial services, transportation, and food and beverage industries also contributed.

Revenues from domestic VAT (+8.1%) benefited from the dynamism of domestic demand—which we estimated had closed 2025 with growth of around 5%—reflected particularly in higher tax payments from the commerce and services sectors. Additionally, since January 2025, the application of the General Sales Tax (VAT) to digital services—such as streaming—has been recorded, with a collection of S/ 678 million during 2025.

On the other hand, non-financial spending by the general government reached S/ 241.6 billions (+5.1%) during 2025. This positive trend was supported by both increased current spending and public investment.

Current spending (+6.8%) increased due to higher salaries, especially for workers under the various labour regimes in the public sector, as well as in the education, health, defense, and interior sectors. It also highlighted the increased acquisition of goods and services, particularly higher payments to workers hired under the Administrative Services Contract (CAS) and service provision regimes at all three levels of government. Furthermore, there was a greater increase in the acquisition of cleaning, security, and surveillance services.

Public investment (+7.8%) reached a record S/ 59.1 billions, highlighting the execution of local governments (+17.4%), particularly in sectors such as transport, sanitation, health and public order, unlike the national government (+0.6%), which moderated its pace of execution especially in works under the responsibility of the National Infrastructure Authority (ANIN).

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.