- Colombia: Monetary Policy Preview—September’s limited room for easing

- Mexico: Mixed employment figures

COLOMBIA: MONETARY POLICY PREVIEW—SEPTEMBER’S LIMITED ROOM FOR EASING

On Tuesday, BanRep will hold its sixth monetary policy meeting of 2025. The economist consensus, and us, expect the interest rate to remain unchanged at 9.25%. This expectation is based on recent upside inflation surprises, minimum wage hike expectations, and a challenging fiscal perspective that had been one of the factors frequently cited by the Board in their caution.

In July, the Board kept the intervention rate unchanged at 9.25%, contrary to the 25 bps cut expected by analysts. The premise had been that June and July would be the only months in which BanRep would have room to resume interest rate cuts ahead of a reacceleration in inflation in the months to follow. The rate cut did not materialize due to the credit sovereign rating downgrade by Moody’s and S&P in June, rising inflation expectations, and a challenging environment marked by anticipated significant increases to the minimum wage and greater financing needs for the government.

Ahead of tomorrow’s meeting we favour rate stability given the following context. Inflation in July and August showed a rebound, rising from 4.82% y/y in June to 4.90% y/y and 5.10% y/y, respectively. Inflation expectations have increased both in the short and long-term. A recent positive market reaction may be partially driven by specific Ministry of Finance operations. And, the risks of a significant increase in the minimum wage are growing. Additionally, the fiscal situation remains under vigilance. Developments in the 2026 General Budget (presented on July 29th) highlight Congress’ refusal to approve a financing law (tax reform), and the lack of concrete announcements to reduce spending implies greater financing needs in the future, which would heighten the Board’s concerns.

Our current monetary policy forecast includes no changes to the interest rate for the remainder of the year. We expect the rate to end 2025 at 9.25%, with cuts potentially resuming in Q1-2026, targeting a rate of 7.50% by year-end 2026.

Key considerations ahead of BanRep’s decision:

- Inflation has increased more than expected in the last two readings (July and August). Annual inflation rose to 5.10% y/y in August; however, inflation excluding food dropped to 4.89% y/y. The Board has highlighted the nature of recent inflation movements, which are believed to be driven by base effects from 2024. These do not create the conditions to resume cuts in the intervention rate. In addition, the BanRep survey shows expectations of further rebounds in inflation, which is projected to end 2025 around 5% again, and remain above 4% in 2026. This would mean more than five consecutive years with inflation readings above BanRep’s target range.

- Economic activity continues to show positive signs of recovery. In July, economic activity posted a 4.3% y/y increase and a 4.2% rise in its seasonally adjusted series—significantly above analysts’ expectations. Household consumption has shown favourable signs amid historically low unemployment indicators (8.8% in July vs. a 12.1% average for Julys since 2001) and a record inflow of remittances into the country (+14% y/y between January and July). This reduces the dilemmas in monetary policy and creates a favourable environment for the Board to focus on guiding inflation toward the target range without major short-term economic sacrifices.

- The uncertainty associated with the minimum wage increase for 2026 poses a risk to inflation converging to the 3% target. Although the discussion is still several months away, the Board highlighted in its previous meeting the risk associated with salary increases significantly above year-end inflation, as has been evident in previous years. In fact, during September, President Petro talked about a significant increase in the minimum wage (close to +11% in nominal terms) as his legacy in the last year of his government.

- The progress in the discussion of the 2026 General Budget reveals a challenging outlook. The new fiscal estimates in the proposed budget suggest an increase in primary spending (COP +10 tn), driven by efforts to reduce debt interest payments by that amount in 2026. As a result, primary spending would rise by 18.2% in COP terms (from 1.4% to 2% of GDP). To finance this expenditure, the proposed increase in fiscal revenues through a tax reform (COP 26.3 tn, 1.4% of GDP) has been questioned by Congress. This has led to the possibility of either cutting the proposed spending or finding alternative sources of revenue, potentially through increased borrowing. Such measures would raise the estimated fiscal deficit and imply a heavier debt burden in the future—an issue that has been strongly emphasized by the board.

—Jackeline Piraján & Valentina Guio

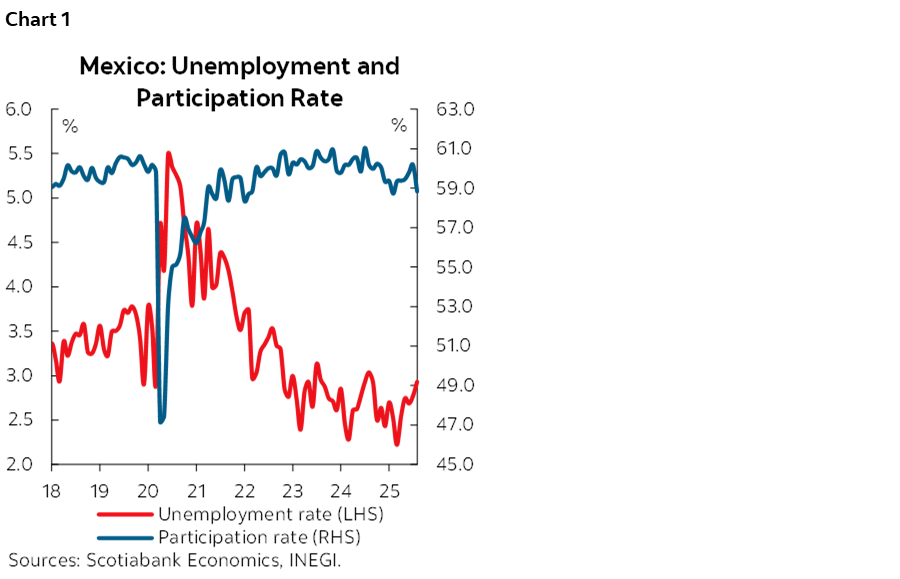

MEXICO: MIXED EMPLOYMENT FIGURES

In August 2025, Mexico’s labour market showed mixed signals. The economic participation rate fell from 60.2% last month to 58.8%, with an economically active population of 61.3 million, while the employed population totaled 59.5 million—down by 201,000 from the previous year. Although the unemployment rate slightly declined to 2.9%, from 2.8% last month and underemployment dropped to 7.1% from 7.3% in July 2025, informality remained high, affecting 54.8% of workers. Female employment rose by 41,000 y/y, while male employment fell by 242,000 y/y. The non-economically active population increased by 2.2 million y/y to 42.9 million, with 5.5 million available to work but not actively seeking jobs. By sector, services accounted for the largest share of employment (43.7%), followed by commerce and manufacturing, while agriculture, professional services, and construction saw the greatest job losses.

—Rodolfo Mitchell & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.