- Mexico: Economic activity weakens in July; Retail and wholesale trade show mixed signals amid uncertainty

- Colombia: July’s imports reach highest level since September 2022 as trade deficit keeps widening

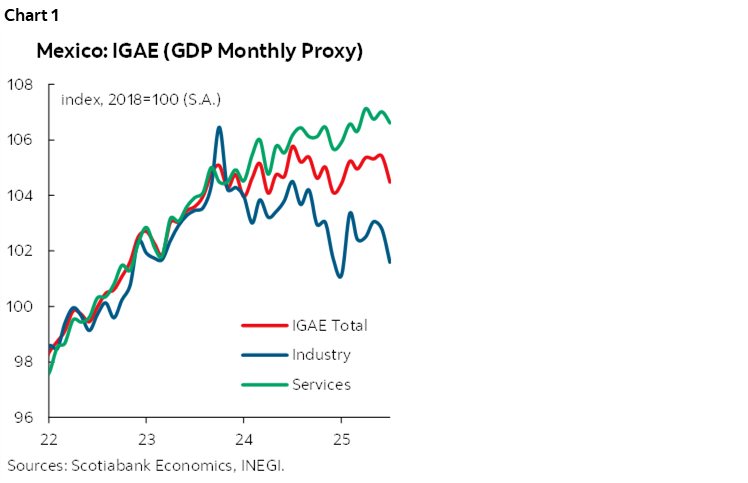

MEXICO: ECONOMIC ACTIVITY WEAKENS IN JULY

In July, the GDP monthly proxy, the Global Indicator of Economic Activity (IGAE) fell -1.1% year-over-year, down from the previous 1.4% y/y (chart 1). By sector, primary activities saw the sharpest decline, dropping -12.3% from 4.6% previously, due to a collapse in agriculture. Industrial activities contracted for the fourth consecutive month, now at -2.7% from -0.4%, with widespread declines, notably in construction (-3.5%) and manufacturing (-1.9%). Meanwhile, services moderated from 2.1% to 0.4% real annual growth, with a 4.3% increase in retail trade contrasting with a -6.6% drop in wholesale trade. Other sectors, such as professional and business support services, continued to show strong dynamism, growing 12.1% and 18.1%, respectively.

Year-to-date, economic activity has grown just 0.1% in real terms, signaling persistent weakness. On a seasonally adjusted monthly basis, the IGAE fell -0.9% m/m (vs. 0.1% previously) after three months of gains. Primary activities declined -3.0% month-over-month, industrial activities -1.2%, and services -0.4%. Looking ahead, we expect services to continue moderating in line with stagnation in formal employment, which is weighing on household consumption. However, manufacturing could pick up pace in the second half of the year, supported by reduced international uncertainty, while construction may maintain some momentum driven by a recent boost in residential building. Nonetheless, we believe domestic uncertainty will continue to skew economic prospects to the downside.

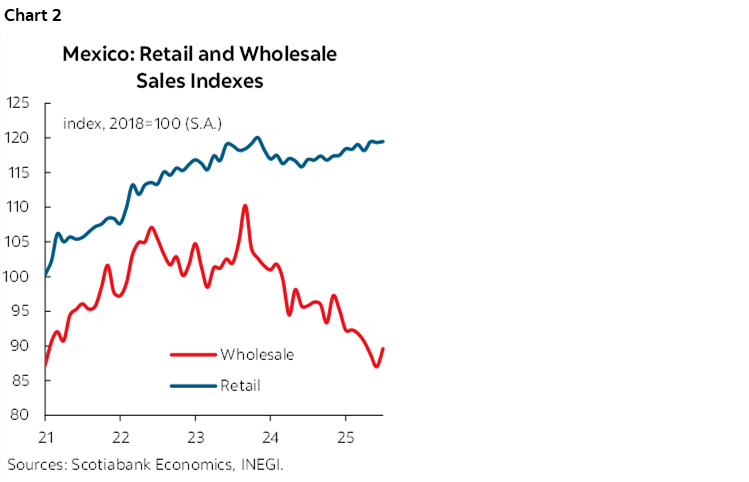

RETAIL AND WHOLESALE TRADE SHOW MIXED SIGNALS AMID UNCERTAINTY

In July, retail sales rose 0.1% month-over-month, surprising to the upside against market expectations of no change (chart 2). The previous month’s figure was revised upward from -0.4% to -0.1%. However, employment and wages in retail trade fell 0.3%. On an annual basis, revenues grew 2.2%, above the 1.6% expected but below the previous 3.2%. Within the sector, only two of its nine subcomponents—groceries and food, and textiles—posted declines. Notably, vehicle and auto parts sales rose 3.4%. Real wages increased 6.8% year-over-year, although employment fell 0.2%.

Meanwhile, in July 2025, real revenues of wholesale trade companies rose 3.0% month-over-month (seasonally adjusted), although employment and average real wages declined 0.2%. On an annual basis, revenues fell -6.5%, continuing the downward trend observed since February 2024. Within the sector, truck and parts sales dropped -11.5% year-over-year, and raw materials -8.5%, while groceries and food were the only categories to avoid negative territory, though they remained flat (0.0%). Wages fell -0.1%, but employment grew 0.7%. Looking ahead, retail trade may continue to grow moderately, in line with softening consumption, while wholesale trade remains affected by weak investment and high domestic uncertainty.

—Rodolfo Mitchell & Miguel Saldaña

COLOMBIA: JULY’S IMPORTS REACH HIGHEST LEVEL SINCE SEPTEMBER 2022 AS TRADE DEFICIT KEEPS WIDENING

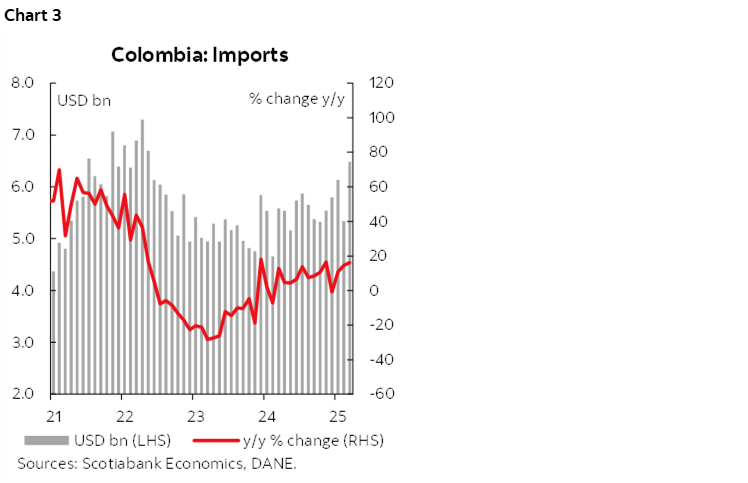

On Monday, September 22nd, DANE published import data for July 2025. Imports reached US$6.48 billion CIF (chart 3), increasing by 16.2% year-over-year and reaching their highest level since September 2022. On a monthly basis, imports grew by 21.5% compared to the previous month. In absolute terms, consumption-related imports remained close to historical highs, posting a 30.1% year-over-year increase, driven especially by durable goods. Imports of raw materials expanded by 22.1% y/y, while imports of capital goods contracted by 3.5% y/y.

Monday’s import figures reflect the nature of Colombia’s economic recovery. Stronger household consumption is driving imports of durable goods. In contrast, investment-related imports show a more moderate trend; imports of raw materials for the industrial sector are the most resilient, although still ~7% below historical highs in absolute terms. The contraction in capital goods imports was mainly due to lower purchases of transport equipment and industrial machinery.

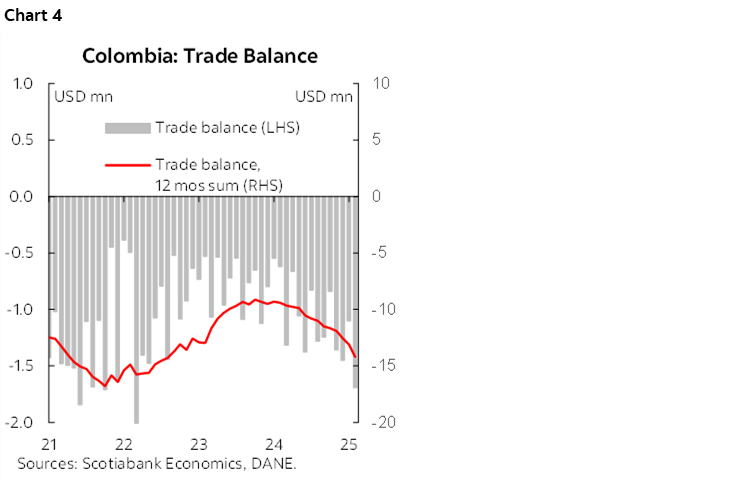

The trade deficit stood at US$1.69 billion, widening by 173% compared to July 2024 (US$617.9 million) (chart 4). In July, exports (FOB) contracted by 4.1% y/y, mainly due to a 17.6% y/y decline in traditional exports, especially coal (-39.6% y/y). In contrast, imports (FOB) expanded by 16.9% y/y. The 12-month accumulated trade deficit reached its widest level since early 2023 (US$14.2 billion, chart 4). Despite this, the current account deficit remains low, supported by increasing remittance inflows.

All in all, external sector data shows that the economic recovery is driving higher imports. However, as remittance inflows remain strong, the wider trade deficit does not translate into structural pressures in the FX market. We recently revised our estimate of the structural macro level for the USDCOP to 4,100 pesos, reflecting expectations of upcoming Fed rate cuts.

Highlights

- Consumer imports remain at high levels. In July, consumption-related imports expanded by 30.1% y/y, in which imports of durable goods lead the increase (+32.8% y/y), while non-durable goods imports expanded by 27.7% y/y. The most dynamic segments are imports of vehicles (+31.1% y/y) and pharmaceutical products (+26.4% y/y).

- Imports of raw materials increased 22.1% y/y. Mainly due to imports for the industrial sector (+24.6% y/y), especially for pharmaceutical and chemical industries (+17.3% y/y) and food industries (+55.1% y/y).

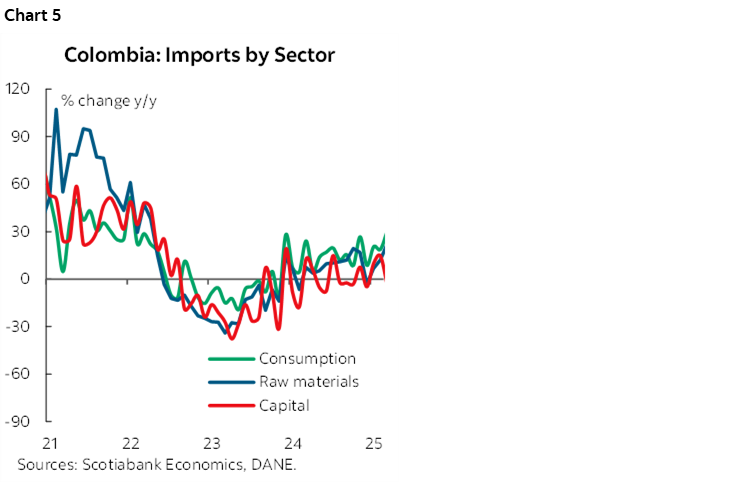

- Imports of capital good contracted 3.5 y/y. Imports of constructions material increased 13.9% y/y. In the industrial sector the dynamic negative with a reduction of 3% y/y, mainly due to lower machinery purchases (23.8% y/y) (chart 5).

—Jackeline Piraján & Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.