- Peru: Yearly pension fund withdrawal strikes again!

Mandated pension fund withdrawals have become a yearly event. On Saturday, the government gave its approval to a Congressional Bill allowing for the eighth withdrawal in six years. The whole debate and approval process occurred with enormous alacrity. In hurried sessions, on September 18th Congress approved the new Law regulating private pension funds. The Executive ratified the Law two days later. The next step is for the Banking Superintendent, SBS, to provide the regulatory framework for the law’s implementation. It has 30 days to do so.

The issue of more immediate macroeconomic interest included in the law is the option for private pension fund affiliates to withdraw up to PEN 21,400 in four monthly parts. But, it was not the only change that was included. The new Pension System Modernization Law (Ley de Modernización del Sistema de Pensiones) also contemplates the following:

- The law extends the option to withdraw 95.5% of funds upon retirement to workers under 40 years.

- The law erases a provision from the previous law that would have required independent workers to begin a compulsory participation in 2028. The new law establishes that this will now be voluntary rather than compulsory.

- The law establishes that affiliates that withdraw their funds will continue to be entitled to the legal minimum pension in the future, which was not true under the previous law.

The new law was always a possibility, but until recently appeared to be relegated to the back burner of Congressional priorities, so much so that until fairly recently there was hope that the issue would not be brought up at all. Instead, the issue was introduced and debated swiftly and the government turned from opposing to favouring the withdrawal practically from one day to another.

Estimates regarding how much funds will be withdrawn run from PEN 26bn to PEN 32bn. In the previous withdrawal in 2024, about PEN 27bn were withdrawn. Assets Under Management (AUM) today total PEN 118bn, just marginally above where it was before last year’s withdrawal, so it seems fair to work under the assumption that a similar PEN 27bn may be withdrawn this time.

Initial impact of the withdrawal

Depending on how long the SBS takes in providing a framework, the most likely date for the first monthly payment to take place would be early November. This should also be the largest payment, as some individual funds will be depleted quickly.

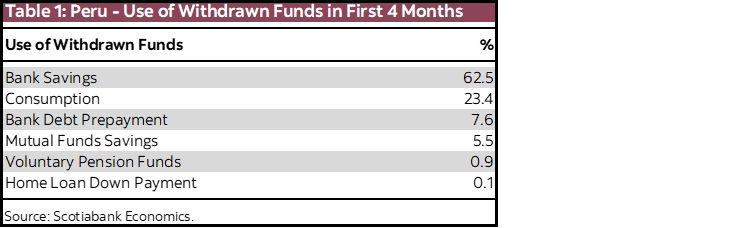

There are four generic ways in which withdrawals have been used in the past: to draw down bank debt, to complement consumption, to augment savings, and to use as a down payment on a home. Based on the withdrawal that took place in 2024, we have estimated how the 2025 funds may be distributed by households in the initial four months following the first withdrawal (table 1).

Nearly two-thirds of savings go into bank accounts in the initial four months. However, they don’t necessarily stay there afterwards. When affiliates withdraw, they receive the funds in a bank savings account. Much of the funds received are maintained in these savings accounts until their owners are ready to dispose of them and distribute the funds to other uses, a process which occurs over time. Typically, the decision to reduce household debt occurs promptly, and the 7.6% debt prepayment estimate is fairly accurate. However, the 23.4% of funds going into consumption is likely to be underestimated over a longer period as drawing upon withdrawn funds for consumption is likely to last for a rather prolonged time. In the meantime, the funds will appear as savings.

Consumption has always risen with withdrawals. The ~20% to be dedicated to household consumption as a first impact seems to be in line with data and consumer surveys linked to previous withdrawals. The lagged impact, as augmented savings spill into greater spending gradually over time, is much more difficult to measure, and gets mixed up with the natural impact of improved household balances (lower debt). However, even if we limit the portion of withdrawal resources used for consumption to 20%, the impact is significant, raising yearly consumption by 0.8pp and yearly GDP by 0.5pp. Given the timing, we expect most of this increase to take place in 2026, although one might expect a particularly frothy 2025 Christmas season as well.

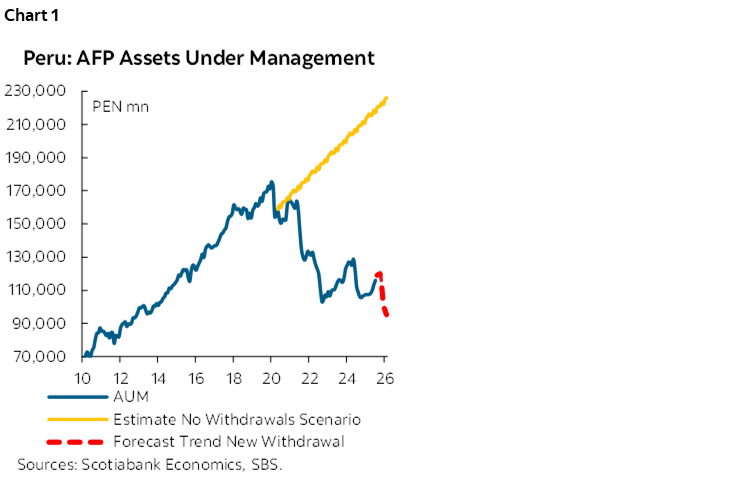

And then there’s the impact on the pension fund system itself, as well as on Peru’s asset markets. This is the eighth withdrawal since 2020, and assets under management have been decimated by these withdrawals. Chart 1 shows the evolution of assets under management before and after withdrawals, together with the possible trend that AUM would have taken, if there had been no withdrawals at all (based on the average long-term yield trend). Note that the no-withdrawal line starts lower than the AUM peak level because of COVID at the time.

The difference is enormous. The current eighth withdrawal of PEN 27bn would potentially lower total AUM to PEN 95bn once the process is over. This compares with nearly PEN 230bn in AUM had none of the eight withdrawals ever taken place. Going forward, affiliates will have to draw their pensions from a pool that is 60% lower than had there been no withdrawals. This is on average. In practice this is likely to mean that most affiliates are likely to have their personal funds largely depleted, and will need to receive the minimum PEN 600 per month pension upon retirement.

The shrinking of the private pension fund system also means that the role that private pension funds have played in local financial markets has become severely impaired, reducing the role that AFPs have had in providing liquidity and breadth to markets. Following the eighth withdrawal, it would take approximately a year and a half for AUMs to return to their pre-withdrawal level. It would take nine years for AUM to return to the level it was at prior to the first withdrawal in 2020. That’s in total AUM terms. In per capita terms, which is what matters for affiliate pensions, the time would be much longer.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.