- Colombia: BanRep Survey—Inflation expectations rise again; rate cut expectations vanish for the rest of 2025

- Peru: 3.4% GDP growth in July, another stable month

COLOMBIA: BANREP SURVEY—INFLATION EXPECTATIONS RISE AGAIN; RATE CUT EXPECTATIONS VANISH FOR THE REST OF 2025

BanRep published its September survey of economists’ expectations (table 1). Inflation expectations rose again, despite the recent CPI print aligning with market consensus. Expectations for December 2025 inflation surpassed the 5% mark, while projections for December 2026 now sit at the ceiling of BanRep’s target range (defined between 2% and 4%). Both are significant shifts, likely driven by growing concerns over persistently sticky inflation, potentially linked to indexation effects from the anticipated minimum wage increase in 2026.

At Scotiabank, our expected inflation path for 2025 is biased to the upside compared to the economist consensus. We project year-end inflation at 5.19%, while for December 2026, our forecast is 3.89%. This projection assumes a minimum wage increase of approximately 7.5%, with indexation similar to what was observed in 2025. However, if the minimum wage increase reaches double digits, our projection would shift toward maintaining inflation above 4.5% by the end of 2026.

Regarding monetary policy, analysts do not expect interest rate cuts for the remainder of 2025. Following the July meeting, the board opted to keep rates steady at 9.25% in a split decision: four members voted for stability, two favoured a 50bps cut, and one supported a 25bps cut. In September, we anticipate continued division among board members. Economic activity remains resilient, in a context of still high inflation and inflation expectations. A potential tailwind for rate cuts could come from international markets, driven by expectations of Fed easing. However, we believe these external factors will not be sufficient to offset domestic concerns regarding the inflation convergence path and structural fiscal risks.

Looking ahead to the medium-term path, the economist consensus anticipates a resumption of the easing cycle in March 2026—in line with our expectations. However, while the consensus sees the policy rate ending 2026 at 8.00%, our current projection is 7.50%, with an upside risk if the minimum wage shock materializes.

The exchange rate outlook continued falling. For December 2025, analysts estimate an exchange rate of 4,056 pesos, 58 pesos lower than the previous survey. By 2026, the forecast is 4,061 pesos, 51 pesos lower than the previous projection. Scotiabank Colpatria’s projection for 2025 is 4,249 pesos, and for 2026, 4,200 pesos.

Key points from the survey:

- Short-term inflation expectations. For September, the consensus estimate is 0.24% m/m, implying annual inflation of 5.10% y/y, stable vs the current level. The higher expectation is 0.38% and the lowest is 0.09%. Scotiabank Colpatria Economics’ projection is 0.28% m/m and 5.13% y/y. Core inflation, excluding food, projected by analysts is 0.22% m/m.

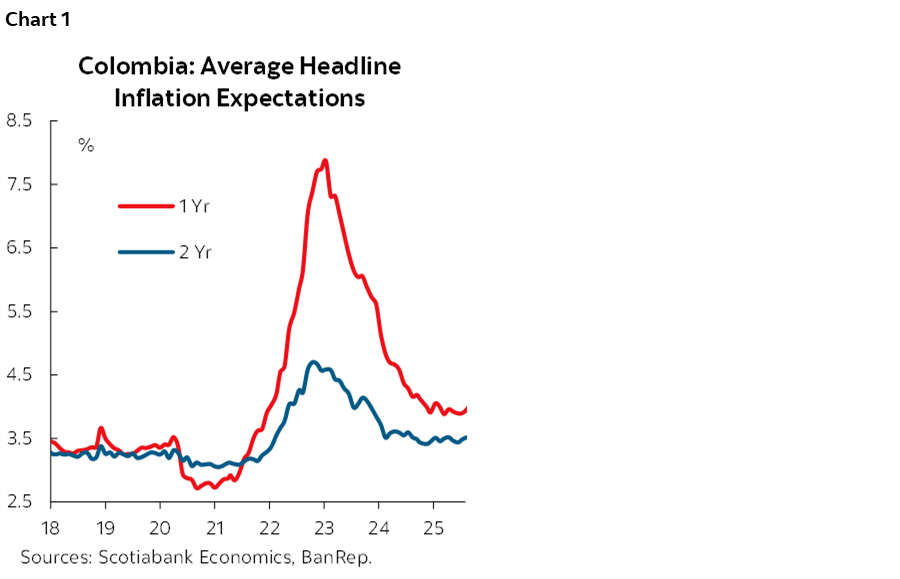

- Medium-term inflation expectations. Inflation expectations for December 2025 increased 9bps to 5.03% (table 1 again). Expectations for the 1-year horizon slightly increased by 11bps to 4.08%, and expectations for the 2-year horizon increased by 2bps to 3.54% (chart 1). Scotiabank Colpatria’s expectations are above the market consensus; however, our bias is primarily explained by low food and regulated prices statistical bases.

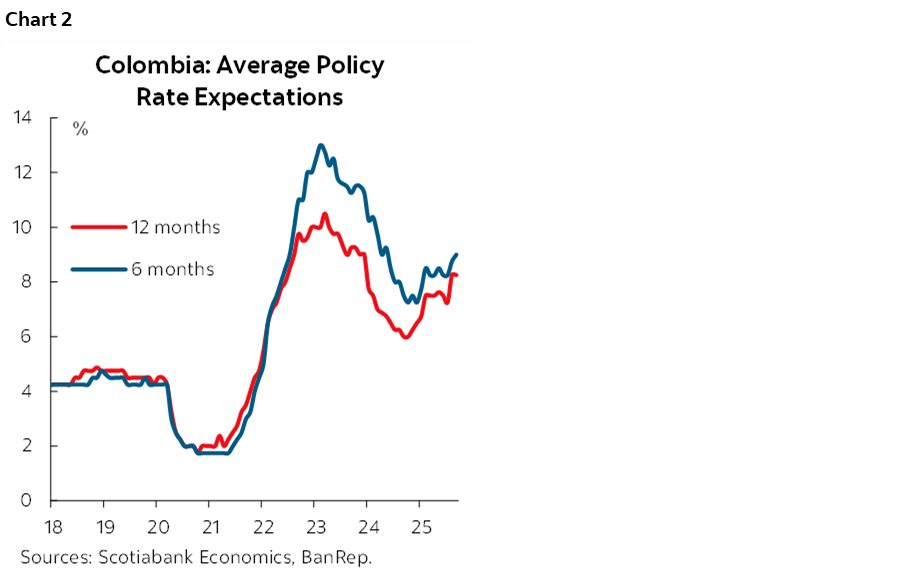

- Monetary policy rate. The median expectation is for stability in the September meeting at 9.25%. Cuts are expected to be resumed in March 2026 (chart 2).

—Jackeline Piraján & Valentina Guio

PERU: 3.4% GDP GROWTH IN JULY, ANOTHER STABLE MONTH

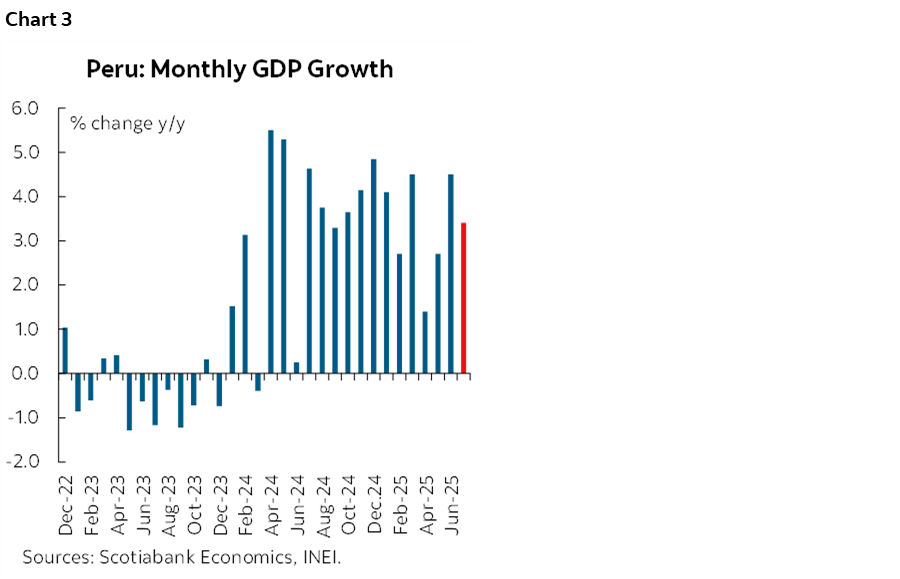

Peru’s GDP growth of 3.4% YoY in July sets it on course for our forecast of 3.1% growth for the year. Growth in month-on-month terms was a robust 0.9% (chart 3).

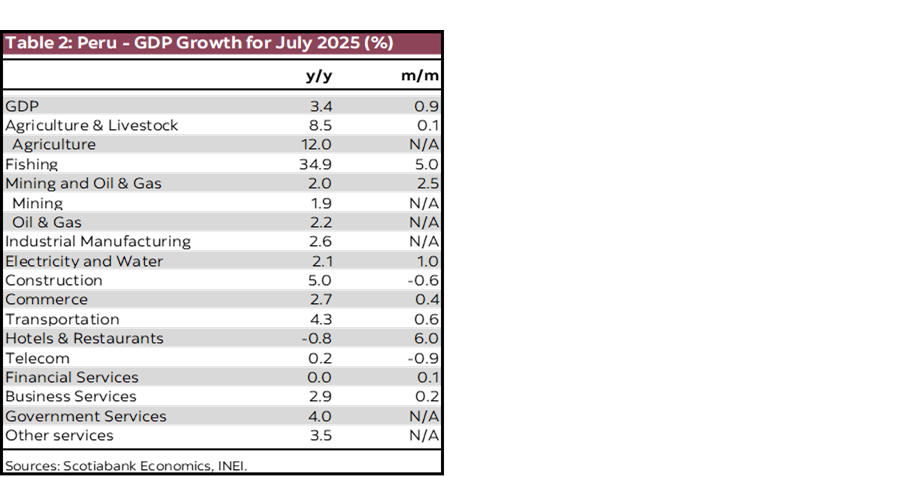

Much of the growth was linked to resource/export sectors. Fishing led, up nearly 35%, YoY, although, due to its low weight in the offseason, it actually contributed less than 0.1pp to growth.

More significantly, agriculture rose a hefty 12%, YoY, contributing a half percentage point to growth. Agriculture growth has been volatile in monthly terms this year, as the sector is still adjusting to the seasonal displacements caused by the 2023 El Niño weather disruptions. Growth in the year-to-date is a much more reasonable 3.6%.

Demand related sectors were mixed, and just a bit disappointing. The key industrial manufacturing GDP rose only 2.6%, YoY, and continues to underperform the economy. Commerce, hospitality, telecom, financial services and business services all were weakish (table 2).

Two domestic demand sectors stood out, transportation, up 4.3%, YoY, and, more importantly, construction, which rose 5.0%, YoY. Both of these sectors have become important drivers of the economy this year among non-resource sectors. Construction growth in particular has become broader, with residential homes contributing increasingly, in addition to infrastructure investment.

GDP growth to date is trending at 3.3%, but should decline mildly due to base comparisons going forward. Leading indicators for August suggest a growth rate of 3.0%, as the base comparison factor begins to manifest itself (table 3).

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.