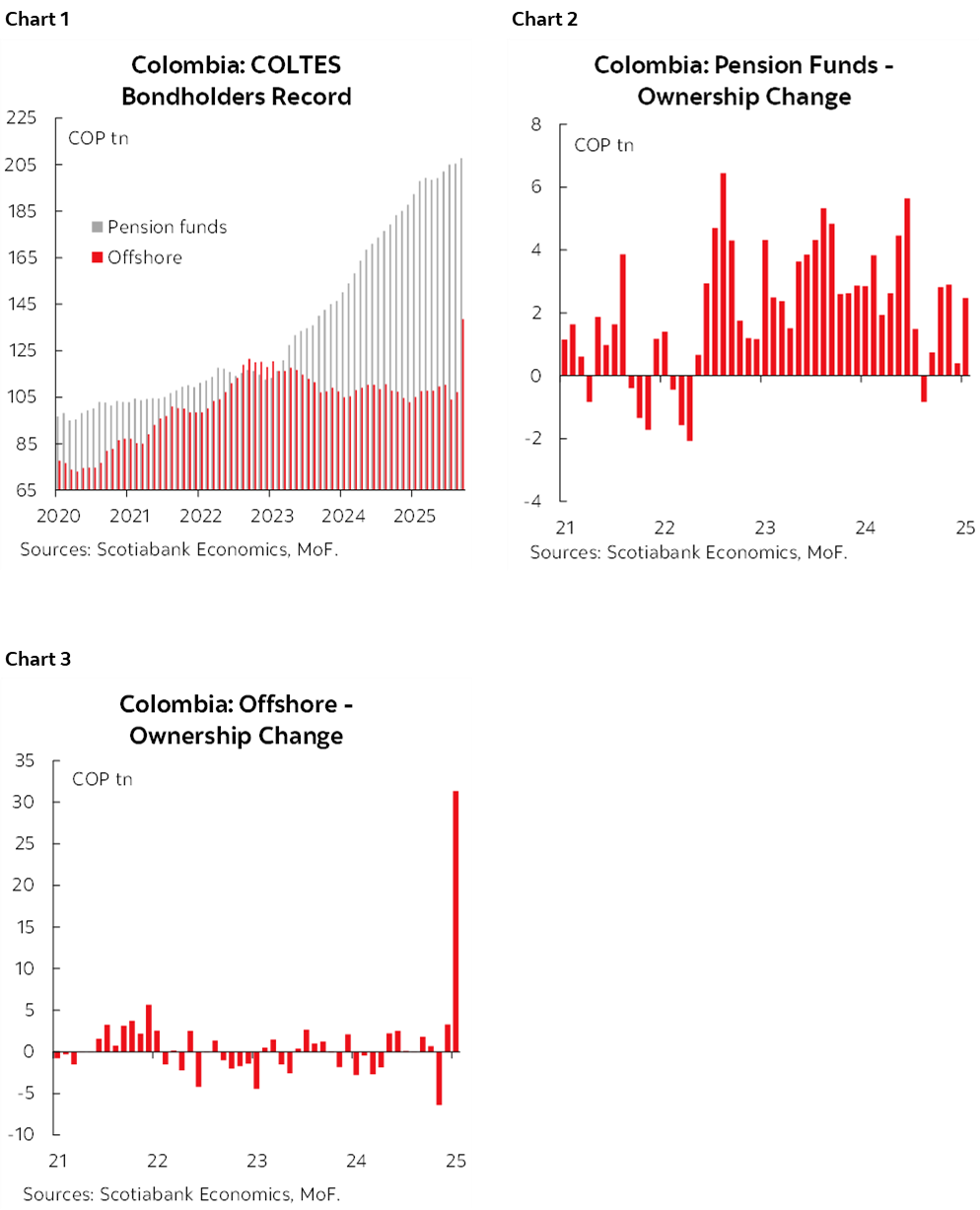

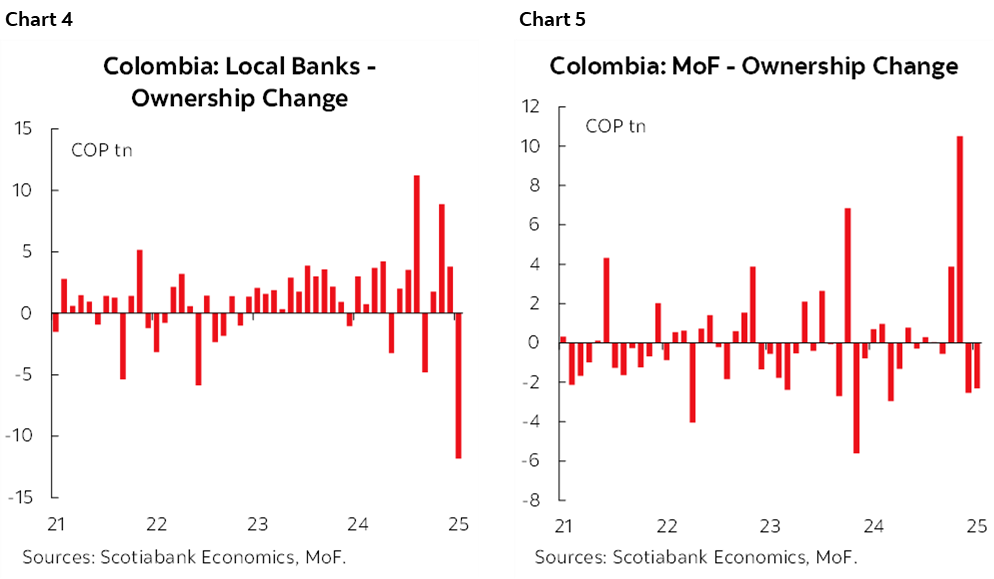

- Colombia: September COLTES Holders Report—offshore portfolios reflected structuring of the TRS with Treasury, while local banks were the largest sellers during the period

- Mexico: Inflation rises, meets expectations; small registered jobs gain

COLOMBIA: SEPTEMBER COLTES HOLDERS REPORT—OFFSHORE PORTFOLIOS REFLECTED STRUCTURING OF THE TRS WITH TREASURY, WHILE LOCAL BANKS WERE THE LARGEST SELLERS DURING THE PERIOD

In September, markets continued to react to the nation’s debt strategy, with the structuring of the Total Return Swap (TRS) taking center stage. During the month, the government carried out a new liability management operation (LMO) on UVR-denominated debt—the sixth so far this year. This operation reduced the outstanding volume of COLTES UVR maturing in 2027, 2029, 2033, and 2035, exchanging them for COLTES UVR 2031 and 2062. Up to this operation, LMOs have collectively led to a COP 8 tn reduction in the country’s nominal debt outstanding (excluding Treasury portfolio operations). In terms of price action, the COLTES pesos curve appreciated 13 bps in a mixed movement that specifically benefitted the belly and the long end of the curve.

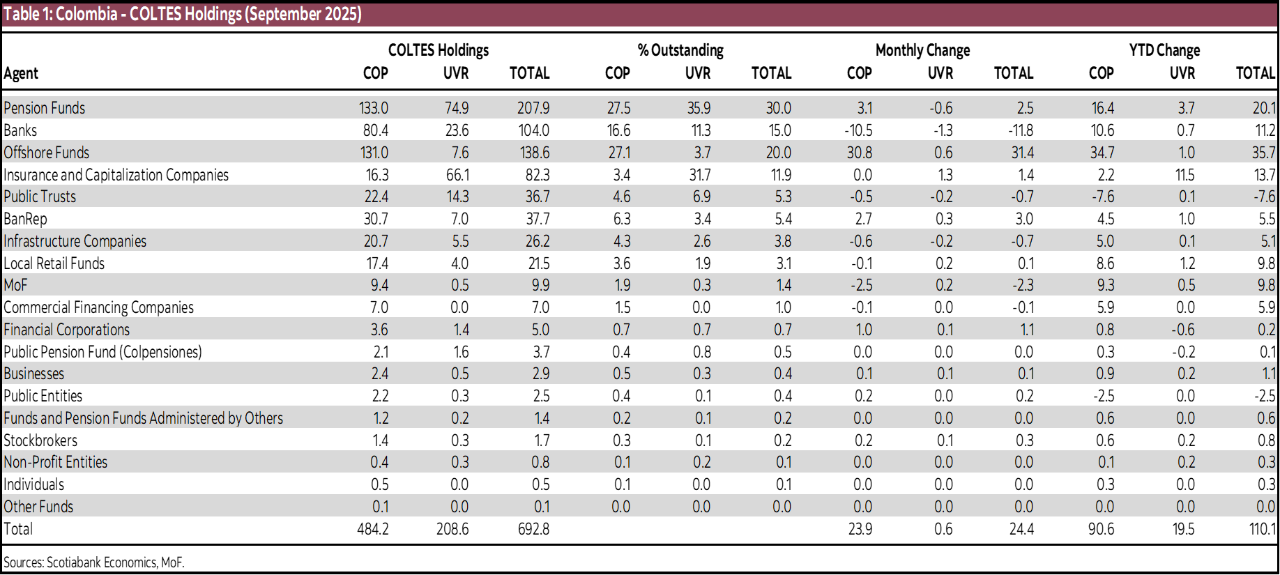

Offshore investors emerged as some of the largest buyers of COLTES during the period (charts 1 and 3), driven by the execution of the TRS, in which six international banks received COLTES. Our estimates indicate that, without this operation, offshore investors would have been net sellers of COLTES in spot transactions by COP 2.4 tn during September. The central bank became the second-largest buyer of COLTES, responding to the economy’s liquidity needs amid significant operations by the Treasury (table 1).

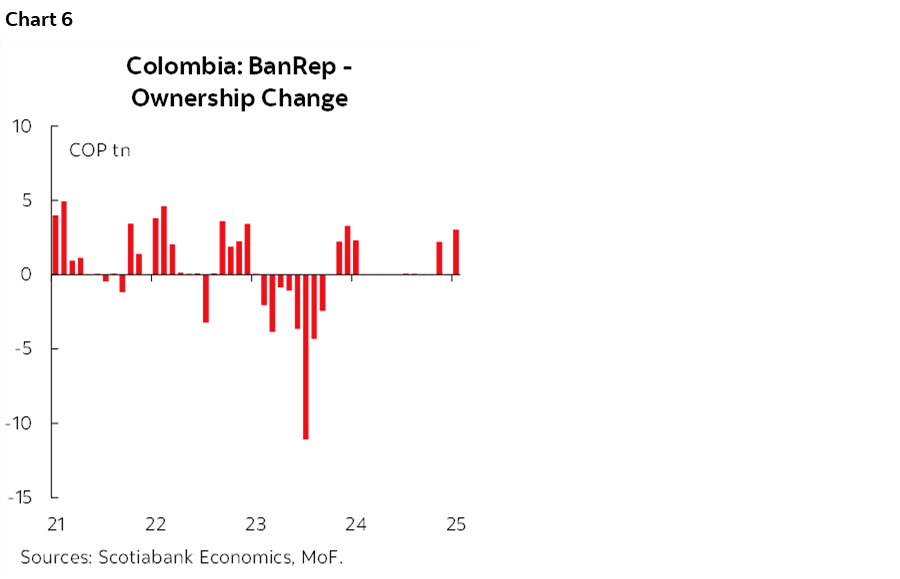

On the other hand, local banks were among the largest sellers of COLTES during the period (chart 4), influenced by the liquidation of holdings by offshore investors through non-delivery forward (NDF) operations. This was followed by the Ministry of Finance (chart 5), whose COLTES sales may have been related to the delivery of these assets for the TRS structuring, offset by purchases executed in the secondary market.

Key takeaways:

- Changes in offshore portfolios reflected the TRS operation. Offshore investors increased their holdings by COP 31.4 tn during the period, due to the delivery of COLTES to six international banks for the structuring of the TRS with the Treasury (COP 21.6 tn in short-term debt called TCOs, and COP 12 tn in COLTES). Our estimates suggest that, in the absence of this operation, offshore accounts would have recorded net sales of over COP 2.4 tn in spot transactions. Year-to-date, they have reported net purchases totaling COP 20.1 tn. Offshore funds have reemerged as the second-largest holders of COLTES, now accounting for 20% of the total outstanding. In September, we also observed position liquidations among some agents who prefer to operate through NDFs.

- BanRep was the second-largest buyer of COLTES during the period (chart 6). Purchases of peso-denominated COLTES totaled COP 2.7 tn, while UVR-denominated COLTES amounted to COP 300 bn. In total, BanRep recorded net purchases of COP 3.0 tn in September—a level not seen since August 2024. These operations were carried out to meet the economy’s increased liquidity needs, likely in response to the operations executed by Treasury, and to help align the overnight IBR with the monetary policy rate.

- Local banks were the largest sellers of COLTES during the period. Sales of peso-denominated COLTES totaled COP 10.5 tn, while UVR-denominated COLTES sales amounted to COP 1.3 tn. In total, banks recorded sales of COP 11.8 tn in September—levels not seen since 2012, when debt holder records began. Their portfolios now total COP 104 tn, representing 15% of the total outstanding. We attribute this portfolio reduction especially to a reduction in rollover of NDFs in COLTES by offshore investors, since the credit market is not picking up substantially to motivate a replacement in bank’s assets.

- The Ministry of Finance reported the second-largest sales. During September, the MoF sold COP 2.3 tn from its portfolio, which totaled COP 9.9 tn for the month. This behaviour reflects the delivery of these assets to the six international banks for the structuring of the TRS, offset by the possible continuation of COLTES purchases executed in the secondary market.

- Total COLTES outstanding increased by COP 24.4 tn in September. The share of nominal bonds represents 69.9% of the total outstanding. Year-to-date through September, total COLTES outstanding has risen by COP 110 tn. In terms of composition, COP 7.58 tn of the monthly increase was driven by auctions (TCOs and long-term COLTES), although this was lower than the previous month due to the postponement of some auctions to allow for external debt issuance.

—Jackeline Piraján & Valentina Guio

MEXICO: INFLATION RISES, MEETS EXPECTATIONS; SMALL REGISTERED JOBS GAIN

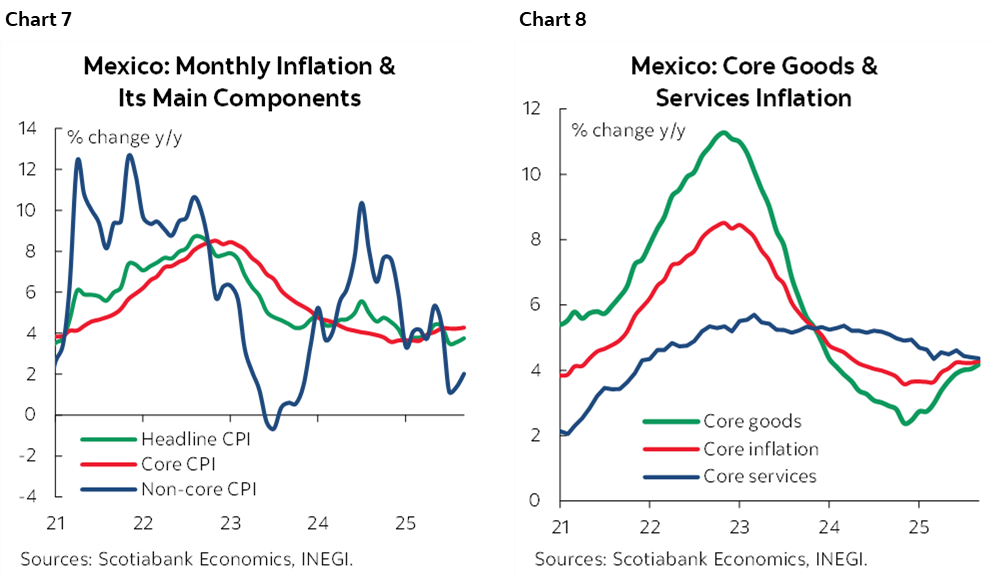

In September 2025, headline inflation rose 0.23% m/m, below the 0.26% expected by analysts, but higher than the 0.06% recorded in August. This placed annual inflation at 3.76%, slightly below the 3.78% forecast, but above the 3.57% from the previous month (chart 7). Core inflation, which excludes volatile items, increased 0.33% monthly and 4.28% annually (chart 8), in line with market expectations and reflecting an acceleration compared to August. This was driven by price increases in goods (4.19% y/y) and services (4.36%). In contrast, the non-core component fell -0.10% monthly, due to declines in agricultural and energy products, with an annual variation of 2.02%. Among the items with the greatest upward impact were housing, primary education, and food services; while eggs, avocados, and professional services contributed to the downward pressure.

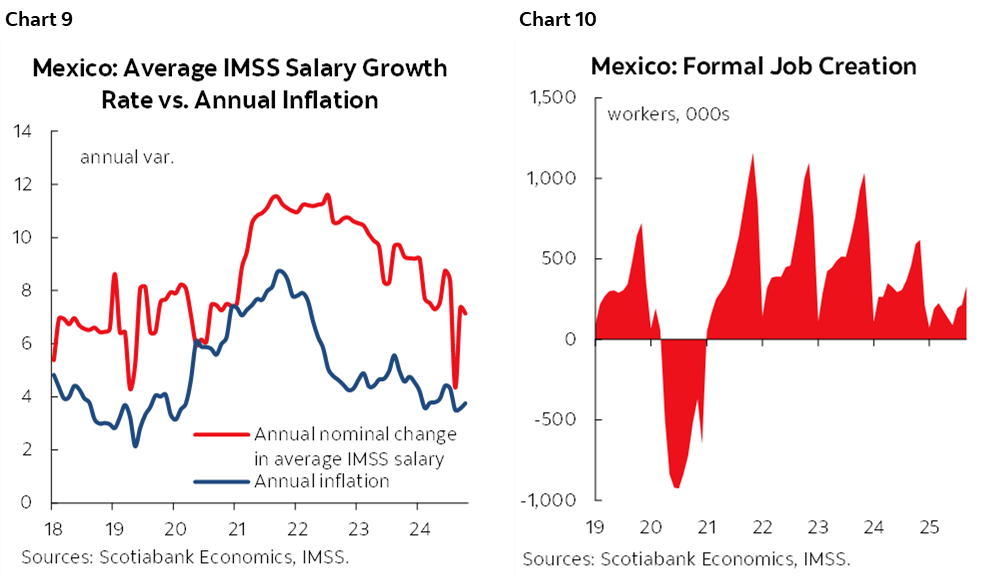

According to the Mexican Social Security Institute (IMSS), 22,571,682 jobs were registered with social security in September. Excluding recent affiliations of app-based workers, the IMSS reported a monthly increase of 116,765 jobs, while the 12-month total showed a net gain of 90,879 jobs, equivalent to an annual growth of 0.4%. On the other hand, the total number of employers during the period was 1,039,227, meaning 25,318 employers were lost over the past year, representing an annual decline of 2.4% and marking 15 consecutive months of contraction. While monthly formal job creation is a positive sign, the modest annual growth and continued loss of employers can reflect structural weaknesses in business formation. Lastly, the average base salary for social security contributions reached $623.10 MXN, reflecting a nominal annual increase of 7.1% (charts 9 and 10).

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.