- Peru: Domestic demand sectors signal strong September growth; Direct lending extends uptrend in September

DOMESTIC DEMAND SECTORS SIGNAL STRONG SEPTEMBER GROWTH

Domestic demand-related sectors remain a key engine of economic activity in the short term, and September has once again confirmed this positive trend. Encouragingly, indicators such as domestic cement and new vehicle sales have not only maintained their momentum but have exceeded our expectations.

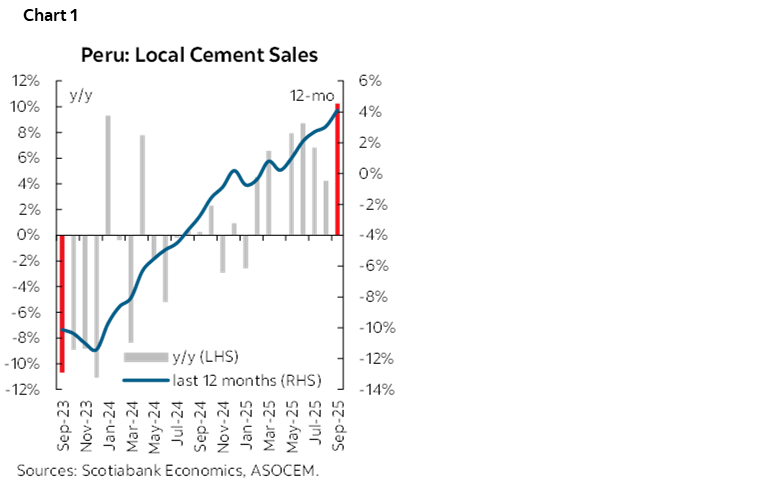

CEMENT SALES

In September, domestic cement consumption reached 1.17 million metric tons—the highest monthly volume since September 2022—representing a 10% increase, YoY, according to ASOCEM, the private sector cement producers’ association. With this result, cumulative cement sales for the year have grown by 5.2%, supporting our forecast projection of around 4% growth for 2025 (chart 1).

Cement sales have shown consistent growth in recent months, and we anticipate this upward trajectory will continue through the remainder of 2025 and into the Q126. This outlook is supported by the recent measure to allow for pension funds withdrawals, which are expected to be partially directed toward consumption—particularly in housing improvements and new construction. Cement demand growth is further reinforced by public investment initiatives and major infrastructure projects under concession.

Overall, the outlook remains constructive, with domestic demand continuing to provide a solid foundation for economic activity and investment.

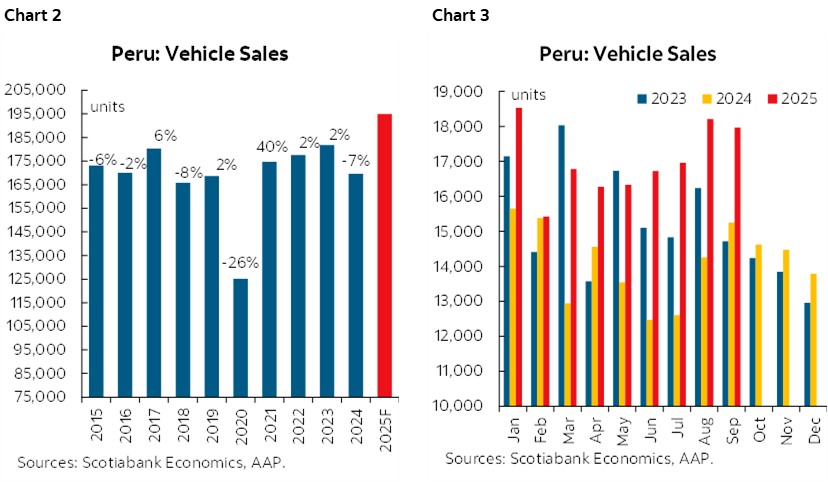

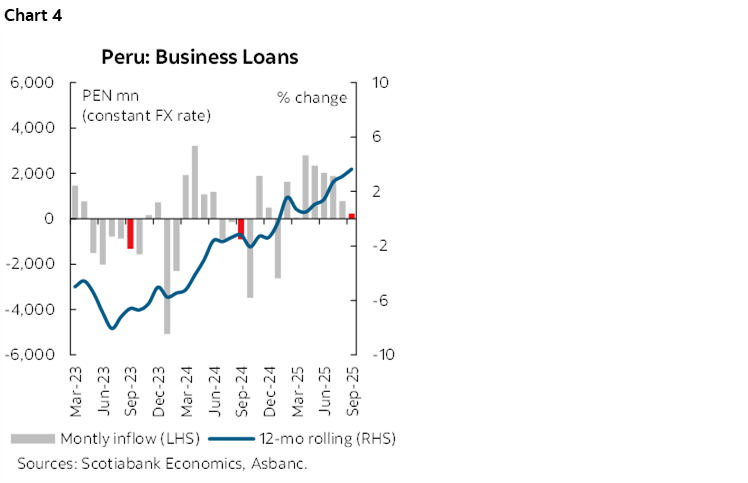

NEW VEHICLE SALES

The new vehicle sector has continued to show impressive momentum in recent months, and we expect this strength to carry through into Q4 25 (charts 2 and 3). While growth rates may moderate slightly due to the high comparison base from Q4 2024, the sector is on track to expand by approximately 17% year-over-year. If realized, this would mark the highest annual growth rate since 2021—highlighting a robust post-pandemic recovery.

According to data provided by Peru’s automobile association, AAP (Asociación Automotriz del Perú), vehicle sales surged by 18% in September, with heavy vehicle sales posting an exceptional 50% increase—the highest monthly growth rate since July 2021. This reflects a growing tendency among companies in mining, construction, and transportation to renew and expand their fleets. Cumulative sales through September have risen by 21%, reinforcing the sector’s strong upward trajectory.

We anticipate that total vehicle sales will reach a historic milestone this year, with volumes approaching 195,000 units—a clear sign of renewed consumer and business confidence. This strong performance is underpinned by several favourable factors: sustained growth in formal private employment, easing inflationary pressures, and a notable improvement in business sentiment, which has particularly boosted demand in the heavy vehicle segment. Additionally, the appreciation of the sol against the dollar has made imported vehicles—especially light vehicles—more affordable in local currency, further stimulating demand.

The factors behind robust cement demand growth include: the expansion of formal private employment, easing inflationary pressures, improved financing conditions—especially in the real estate sector—and relative stability in the prices of construction materials, particularly those of imported origin. Despite recent external market turbulence, including the imposition of tariffs in the U.S. on products such as steel, the impact on imported construction material prices has been limited. The appreciation of the sol against the dollar has facilitated a higher volume of imports, especially for high-value real estate developments and large-scale infrastructure works.

In summary, the automotive market is experiencing a dynamic recovery, supported by solid fundamentals and favourable macroeconomic conditions. The outlook remains bright as both consumer and corporate demand continue to drive growth.

—Carlos Asmat

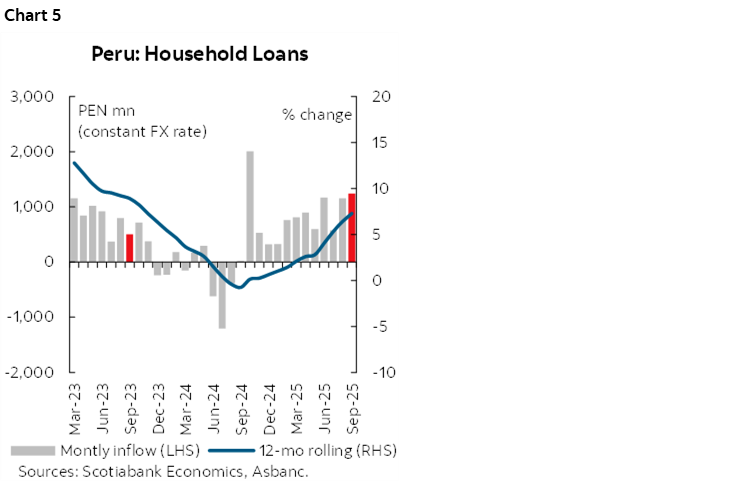

DIRECT LENDING CONTINUES ITS UPWARD TREND IN SEPTEMBER

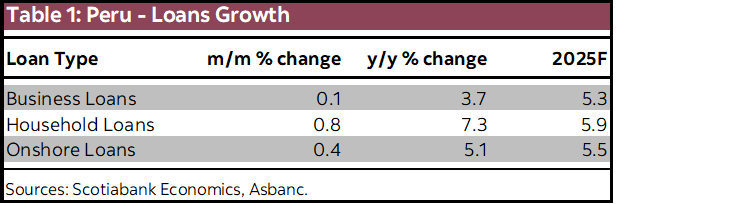

Direct lending grew by 5.1% year-on-year in September, above the 4.4% y/y recorded in August and throughout the year, reinforcing its steady growth path since January. The acceleration in direct lending is supported by the favourable performance of the local economy, mainly domestic demand that grew 6.2% in the first half of the year. Business lending increased by 3.7% y/y, marking eight consecutive months in positive territory, while household lending grew by 7.3% y/y, consolidating a strong rise since October 2024.

Business lending shows a solid recovery linked to the growth of private investment (9.0%) in 1H25 (chart 4). The monthly flow is positive compared to the same month in previous years, reflecting strong performance in corporate and large business loans, which grew by 9.5% y/y in September, and a recovery in loans to medium, small, and micro enterprises, improving from -7.8% y/y in August to -6.5% y/y in September.

On the household side, lending continues to expand, reaffirming its positive trajectory in line with the growth of private consumption (3.7%) in 1H25. Mortgage loans remain robust, with growth rates consistently above 6.0% y/y (chart 5). Consumer loans are beginning to grow at a good pace, increasing by 7.6% y/y in September. One factor that could impact the dynamics of consumer loans through short-term amortization is the disbursement of pension funds that begins in November. However, we expect consumer lending to continue to grow due to lower levels of delinquencies. The eighth withdrawal finds a lower delinquency rate of 4.4% on credit cards as of September compared to the delinquency rate of May 2024, a month before the disbursement of the seventh withdrawal, located at 6.4%.

We expect total loans to continue expanding at solid rate, growing around 5.9% by the end of the period. Business lending is projected to grow by 5.3% and household lending by 6.5% despite the impact of pension fund withdrawals (table 1).

—Grecia Fajardo

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.