- Chile: Near-neutral bias in the short term; risks remain and inflation has lingered above target for too long; Private salaried job losses raise concerns about labour market recovery

- Colombia: BanRep’s rate to stay on hold amid uncertainty and increasing inflation expectations

CHILE: NEAR-NEUTRAL BIAS IN THE SHORT TERM; RISKS REMAIN AND INFLATION HAS LINGERED ABOVE TARGET FOR TOO LONG

A volatile activity outlook and mixed labour market signals call for further data accumulation before taking another step in monetary policy. This broadly reflects the scenario described in the previous statement, maintaining its bias and leaving the door open to a rate cut in December. However, as we note below, such a move is particularly conditional on the evolution of the main absorber (or amplifier) of supply shocks: the exchange rate.

Of concern is the reference to 2-year inflation expectations above 3% in the Financial Traders Survey (FTS), which is a matter of particular importance for any central bank—especially when annual inflation has remained above the 3% target for several years. In this context, at Scotiabank, we remain unconvinced about a December policy rate cut in the absence of a significant appreciation of the peso.

Is a December rate cut necessary? Yes, but conditional on a (significant) appreciation of the peso. The combination of stronger domestic momentum, a policy rate in the “neutral zone,” and inflationary risks linked to internal demand and labour costs (yet to materialize) limits the room for monetary policy adjustments without a significant decline in the exchange rate. This is occurring in a context where:

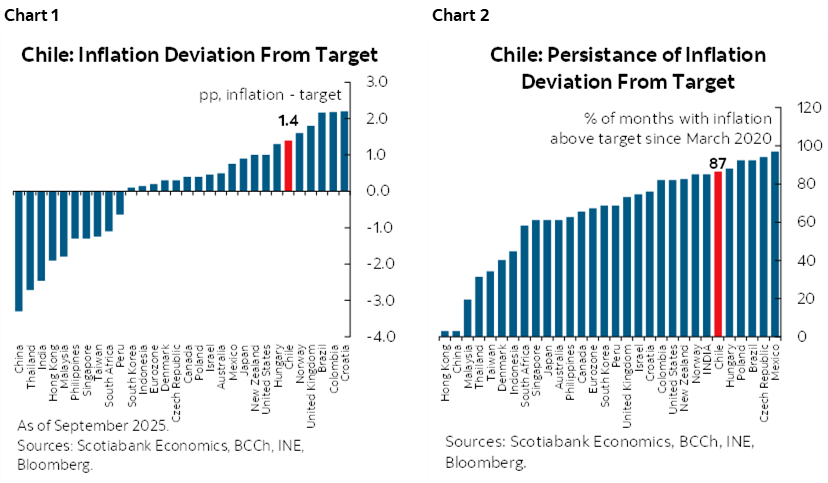

- Inflation has remained above 3% for an extended period. As shown in charts 1 and 2, Chile is among the countries where inflation is furthest from its target and has remained in that state the longest (charts 1 and 2). As one Board member recently noted, inflation has exceeded 3% for over four and a half years—marking the longest deviation from the target since the current inflation-targeting framework was implemented in the 2000s.

- The monetary policy rate is in the “neutral zone.” According to our recent estimates, Chile’s neutral interest rate lies at the upper end of the Central Bank’s estimated range (4.00–4.50%), indicating limited room for further rate cuts.

- The economy continues to grow above potential, at the margin. Preliminary September figures from our nowcast models point to non-mining GDP growth above 4.5% y/y, reaching historically high activity levels, driven by services, commerce, and industry. This will reinforce market conviction that there is little room for further rate cuts at this stage.

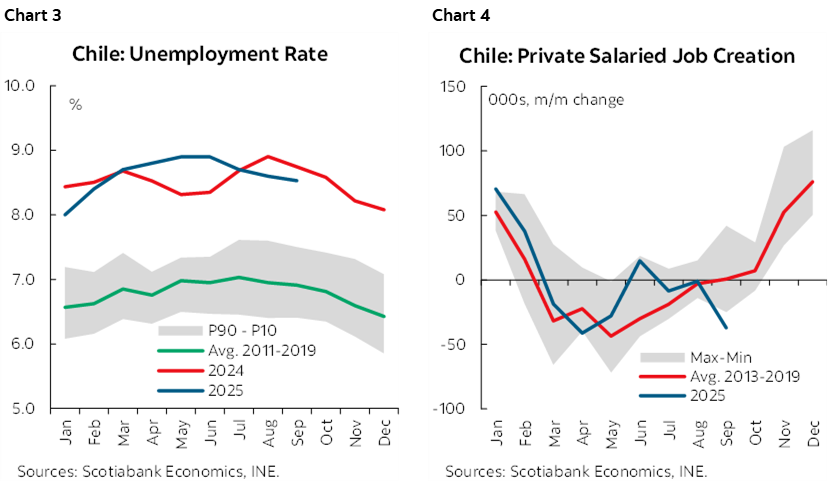

- The labour market is showing early signs of improvement, with marginal job creation. Seasonally adjusted unemployment has returned to levels considered “non-inflationary,” a trend likely to consolidate in the coming months alongside a rebound in investment, particularly in construction.

- Upward pressures on core inflation due to rising labour costs and peso depreciation. Two-year inflation expectations are beginning to rise (FTS: 3.1%), as noted by the Central Bank. Concerns persist over the diffusion of goods (at historical highs) and the consecutive price adjustments, particularly among non-volatile items—most notably goods. We interpret this as an attempt to restore margins in response to rising labour costs and peso depreciation, within a context of stronger private consumption led by lower-income segments.

- A significant peso appreciation before the next meeting could allow for a December rate cut, after the presidential runoff.

PRIVATE SALARIED JOB LOSSES RAISE CONCERNS ABOUT LABOUR MARKET RECOVERY

Chile’s labour market shows modest improvement, with unemployment dropping to 8.5%, in line with seasonal trends and expectations (chart 3). However, job creation slowed to +23,000, below typical September levels (chart 4), mainly due to significant losses in private salaried employment in commerce, manufacturing, and services.

Labour force participation continues to rise, limiting further declines in unemployment and revealing persistent labour market slack. The seasonally adjusted unemployment rate remains at 8.4%, near the upper bound of the BCCh’s non-inflationary range.

Private salaried employment fell by 37,000, a counter-seasonal decline concentrated in commerce, education, real estate, and manufacturing (chart 3 & 4). Gains were seen in administrative services and hospitality. The magnitude and timing of these losses raise concerns about the sustainability of the recovery in the labour market.

—Waldo Riveras

COLOMBIA: MONETARY POLICY PREVIEW—BANREP’S RATE TO STAY ON HOLD AMID UNCERTAINTY AND INCREASING INFLATION EXPECTATIONS

On Friday, October 31st, BanRep will hold its seventh monetary policy meeting of 2025. The economist consensus, including Scotiabank Colpatria, expects the interest rate to remain unchanged at 9.25%, continuing the stability observed for most of the year—likely with the same voting split seen in previous meetings. The discussion may centre around recent upward inflation surprises, a challenging fiscal outlook, and expectations of a significant increase in the minimum wage for 2026.

In September, the board kept the intervention rate unchanged at 9.25%, in line with analyst expectations (see here). Although the international environment appears more favourable due to the Federal Reserve’s interest rate cuts, the board sees even stronger reasons to remain cautious: i) Upward surprises in medium- and long-term inflation; ii) A boost in domestic demand driven by household consumption and higher fiscal deficits; iii) FX performance which is showing some concerning dynamics, making its effectiveness in reducing inflation pressures uncertain. Moreover, the FX has been driven by capital inflows to finance the government, rather than reflecting dynamic FDI; iv) Significant increases in the minimum wage, as publicly announced by the government, which could delay inflation’s convergence to the target; and v) Greater fiscal pressures that could raise risk premiums in the medium term.

Ahead of the October 31st meeting, we continue to favour rate stability given the following context: Inflation in August and September showed a rebound, rising from 5.10% y/y to 5.18% y/y, and inflation expectations have increased in both the short and long term. In fact, surveys show that the possibility of inflation falling within the target range in 2026 has vanished.

On the other hand, although the USDCOP remains at low levels, we attribute this to exogenous factors. The strong remittance inflows (+14% y/y through August), which are offsetting the widening trade deficit, would explain the FX performance. Additionally, intensive government monetizations are also influencing exchange rate behavior. However, despite these factors, tradable goods prices have not responded to the improved FX conditions—likely due to strong domestic demand.

On the fiscal front, concerns remain unchanged. Between January and August 2025, the fiscal deficit reached 5.1% of GDP, the highest level on record. Significant adjustments to revenues and expenditures are unlikely, especially ahead of an election period, which increases risk premiums in the medium term.

It is worth noting that in this meeting, the board will have the updated Monetary Policy Report from the central bank staff as an input. Details of this publication will be released next week; however, we expect the staff’s tone to lean hawkish.

Our current monetary policy forecast assumes rate stability for the remainder of the year. We expect the rate to end 2025 at 9.25%, with cuts potentially resuming—not in Q1 2026 as initially expected, but rather in Q2 2026—targeting a rate of 8.25% by year-end 2026. Last but no least, although Director Villamizar was vocal during the IMF meeting about the possibility of rate hikes, we do not expect this discussion to take centre stage just yet.

Key points to consider ahead of October’s BanRep meeting:

- Inflation has increased more than expected in the last two readings (August and September). Annual inflation rose to 5.18% y/y in September, and inflation excluding food increased to 4.94% y/y. The board has highlighted the nature of recent inflation movements, which are believed to be driven by base effects from 2024, but they also emphasize that the future disinflation process is uncertain, as it depends on factors such as food shocks or a continued negative trend in regulated prices—both of which are beyond BanRep’s control. These conditions further reinforce the case for maintaining a cautious stance. In addition, the BanRep survey shows expectations of further rebounds in inflation, which is projected to end 2025 around 5% again and remain above 4% in 2026. This would imply more than five consecutive years with inflation readings above BanRep’s target range.

- Economic activity continues to show positive signs of recovery. In August, economic activity posted a 2.0% y/y increase—below analysts’ expectations—but this was due to base effects from the significant growth in the previous month (4.4% y/y in July) and some calendar effects that impacted the industrial sector. Domestic demand has continued its growth path, supported by household consumption amid historically low unemployment (8.6% in August vs. an 11.5% average for Augusts since 2001) and a record inflow of remittances into the country (+14% y/y between January and August), while public spending has also contributed to this outlook. Additionally, the Colombian economy is projected to grow near its potential in 2026, which allows the board to focus on guiding inflation toward the target without the need for major economic sacrifices.

- The uncertainty associated with the minimum wage increase for 2026 poses a risk to inflation’s convergence to the 3% target. Although the discussion is still several months away, the Board highlighted in its previous meeting the risk associated with salary increases significantly above year-end inflation, as has been evident in previous years. In fact, during September, president Petro talked about a significant increase in the minimum wage (close to +11% in nominal terms) as his legacy in the last year of his government.

- The absence of proposals to achieve fiscal consolidation reveals a challenging outlook. Recently, the Colombian Congress approved the 2026 national budget for COP 547 tn, which, although it reflects a COP 10 tn cut, would still require a tax reform of COP 16 tn to finance it. For now, the Board has warned that higher fiscal deficits (5.1% of GDP between January and August 2025), and the absence of structural adjustments, mean that increased financing needs may be crowding out private investment and delaying the recovery of the credit portfolio. This implies a risk balance tilted by the growing involvement of the national government in the private sector.

—Jackeline Piraján & Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.