- Peru: A new day a new government; BCRP unchanged, as expected

- Mexico: Banxico minutes reinforce cutting bias; Industrial production retreats

PERU: A NEW DAY A NEW GOVERNMENT

Peru woke up to a new President this morning, José Jerí, a 38 year old lawyer and Member of Congress from the Somos Perú party. José Jerí was designated President by Congress after Congress impeached now former President Dina Boluarte overnight. This, a change in government, has become typical fare for Peru, a country where rumors may abound for months regarding a presidential impeachment and nothing happens, and then, from one day to the next, out of the blue there is a midnight impeachment and a sudden new President.

There were two reasons behind the impeachment of former president Dina Boluarte. The first is that her government was weak from the outset and an impeachment had always been a Damocles sword above her. In fact, if anything, her government lasted longer than many expected. However, the issue that precipitated her ouster was a surge in high profile events and a perceived breakdown in domestic security. On October 8th a shooting took place at a concert by local musicians in Lima, presumably for not having paid extortions to criminal groups. This occurred during a week of on-off transportation strikes, also protesting extortions.

Some analysts add a third reason. Members of Congress may have considered that impeaching an unpopular president such as Boluarte could give bonus points with public opinion that could bolster their chances for the upcoming elections.

What does this all mean? José Jerí is the seventh president in seven years. Of these seven presidents, only two were elected as such, Pedro Pablo Kuzcynski in 2016, and Pedro Castillo in 2021. So there is a greater weakness overriding Peru’s day-to-day politics, and that weakness has to do with the country’s political institutions. The current change is a reflection of this institutional weakness.

One can find a silver lining, however, in that these changes have largely occurred within the rule of law. Outside of Castillo’s attempt to close Congress, there has never been an attempt to institute an authoritarian regime. Note that institutions were strong enough to impede Castillo’s intentions. So, yes, political institutions are weak, but the rule of law is faring much better.

One can only hope that the 2026 elections will produce a government with a greater degree of legitimacy and underlying strength that will provide more political order in the country. Until then, it is difficult to conceive that the Jerí government can make significant inroads in this direction.

Two questions arise with the regime change: what does it mean for the economy, and what does it mean for the 2026 elections?

Economic management will depend crucially on the new cabinet, and on who is chosen as finance minister in particular. We are waiting for these designations. In the past, new cabinets have typically been appointed within 72 hours. It’s an open question as to how long it will take to put together a new cabinet, as Jerí was not (we believe?) expecting to become president, and thus was not prepared to be one. Our hope is that he might choose from within the Ministry of Finance for a name, and in general choose institutional names with experience for cabinet positions, as opposed to political appointees. The latter is an important risk however.

The context for the economy is encouraging. The change is taking place at a time when metal prices are surging, exports are at record levels, and the fiscal situation is under control. Furthermore, this will be a relatively short-lived government and, with elections on the horizon, business and consumer confidence may be more focused on those rather than on the current government.

Of course, the elections are all a risk on their own, but it is the same risk that the country has already been facing. Unless, the new government were to choose to influence the elections in some way. There is no reason to believe that this will be the case, other than the fact that the Jerí government emerges from Congress, and that Congress had been tweaking and talking about elections regulations for convenience sake for some time. Our base case is that this will not be an issue, but there is a degree of risk that it will.

There are a few areas of government behaviour concerning the economy that we shall be looking at. One is whether the new government will continue with the policy adopted by the Boluarte government to aggressively promote the tender of infrastructure projects under public-private partnerships. This has been an undertaking by Proinversión, a relatively autonomous entity, so it’s really a question of whether Proinversión will continue to operate as it has been over the last three years.

Furthermore, just a change in cabinet itself frequently means that public sector activities, and especially public investment, suffer for a time. Cabinet changes have their learning curve.

Another issue is policy. José Jerí has come from the ranks of a Congress that has been conspicuous in promoting laws geared to benefit interest groups or which otherwise have a populist bias. So the question emerges regarding just how populist the new government will be. Once again, the formation of the cabinet will give us an idea in this regard.

Will the Jerí government last? There is some noise about impending protests against the new Presidency. Members of Congress in general are not popular, and José Jerí in particular is viewed as someone with baggage. It is not clear how strong, or even lasting, a government like his will be. The one mark that President Jerí would need to make quickly to win over public opinion would be to announce and implement a strong and credible strategy to confront crime and domestic insecurity in general.

It’s early days still. For now we need to see the make-up of the new cabinet, we need to see the reaction of the markets, and we need to see how public opinion reacts. It’s true that the Jerí regime risks being a source of uncertainty until July next year, but that may simply be par for the course for Peru. For the time being, we are not changing our forecasts for 2025 or for 2026. We need more information before we can do so. Given that our forecasts were made already considering underlying political uncertainty, there is a good chance (one can hope?) that we may not need to make material changes.

—Guillermo Arbe

BCRP UNCHANGED, AS EXPECTED

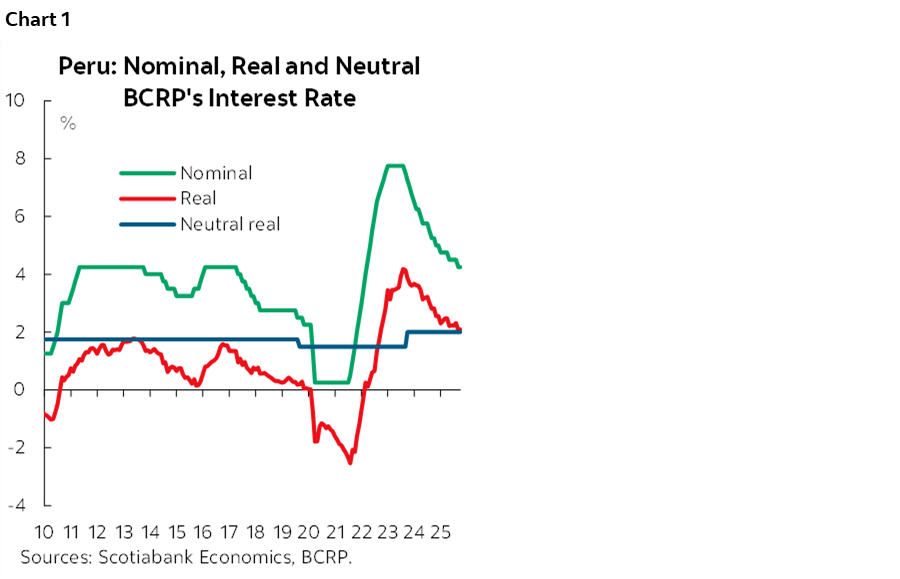

The Board of the Central Reserve Bank of Peru (BCRP) decided to keep its benchmark interest rate unchanged at 4.25% in October, following a 25 bps cut in September. This decision was in line with the market consensus (as reflected in the Bloomberg median). The interest rate differential between the BCRP and the U.S. Federal Reserve remains at zero (chart 1).

The October statement closely mirrors the one issued the previous month and underscores the following key points:

- Headline inflation is expected to approach the midpoint of the target range (1%– 3%) by year-end, while core inflation is projected to remain around 2.0% in the coming months.

- Inflation expectations have remained stable at 2.2%.

- Economic activity expectations and the current situation remain in the optimistic range, in a context where economic activity is hovering around its potential level.

- Global economic outlook continues to be affected by restrictive measures on international trade.

As a result of the decision, the real interest rate rose from 2.07% to 2.09%, very close to the neutral rate (2.0%). Given the narrow differential—just 9 basis points—there appears to be limited room for further rate cuts. Any further adjustment will depend on the trajectory of 12-month inflation expectations. In the past, these expectations have shown resistance to remaining at or below 2.0%, even when headline inflation approached zero.

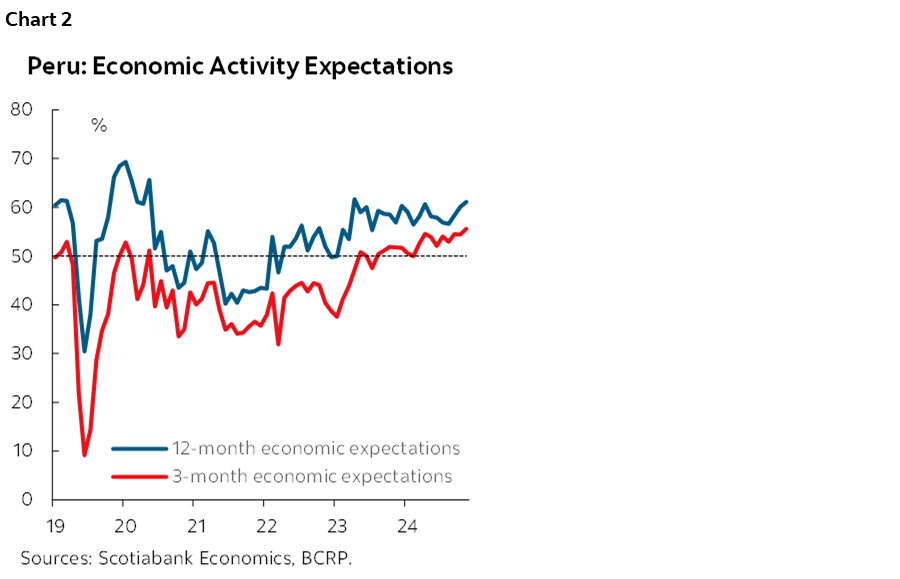

Price stability, strong domestic demand growing above 6.0% during the first half of 2025 and robust economic activity expectations, despite the upcoming presidential elections and political risks, reinforce the perception that the BCRP is unlikely to adjust its policy stance in the near term. Notably, twelve-month economic expectations have trended upward over the past four months, while three-month expectations have reached a six-and-a-half-year high (chart 2).

Accordingly, we anticipate the benchmark rate will remain unchanged through year-end.

We preliminarily estimate that headline monthly inflation for October will be positive, reaching approximately +0.15%, driven by an increase in the food category. Additionally, a base effect will be present, as the October 2024 figure was negative (-0.09%), contrasting with the 20-year average of 0.1%. As a result, twelve-month inflation is likely to rise from 1.36% in September to 1.65% in October.

Twelve-month inflation expectations have edged down slightly, from an average of 2.18% in August to 2.16% in September. By year-end, economic agents anticipate a range between 2.00% and 2.10%, and for 2026, between 2.20% and 2.30%, according to the most recent macroeconomic expectations survey published on October 3rd. On our part, we expect inflation to close at approximately 1.9% in 2025 and around 2.2% in 2026.

—Ricardo Avila

MEXICO: BANXICO MINUTES REINFORCE CUTTING BIAS

Banxico released the minutes of the September 25th meeting, providing details on the discussion surrounding inflation and monetary policy, with a majority decision to adjust the pace of rate cuts to 25 basis points, bringing the target interest rate to 7.5%. Overall, we highlight that the arguments of the Governing Board members revolved around the current level of inflation, emphasizing the increase in the core component, as well as the relative stance of interest rates. In this regard, despite the recent rebound in goods prices, comments suggest that several members consider it appropriate to continue with adjustments in upcoming meetings.

Moreover, the dissenting opinion of Deputy Governor Heath is worth considering. Mr. Heath argued that upward revisions to the core inflation forecast suggest its persistence has been underestimated, and that the non-core component could rebound at some point within the forecast horizon. He also concluded that there are difficulties in consolidating a downward inflation trajectory and included the impact of tax and tariff increases among the inflationary risks in the outlook. Therefore, he suggested being more cautious until there is greater evidence towards the 3.0% target.

Regarding the international economy, some members mentioned that during the third quarter of 2025, global economic activity likely showed a slowdown compared to the previous quarter, with persistent weakness in the manufacturing sector and stronger performance in services. In the United States, growth remained stable, driven by investment in high technology, although there were cooling signs in household spending and the labour market. Headline inflation remained slightly above targets in most economies, while core inflation showed persistence, especially in goods and services. In this context, easing cycles have been started by several central banks, notably the Federal Reserve, which reduced its rate by 25 basis points and anticipates further cuts for the remainder of the year.

Regarding Mexico’s economy, in the second quarter of 2025, GDP grew by 0.64% q/q, surpassing the performance of the first quarter and previous expectations, leading to an upward revision of annual projections. However, a weak economic environment persists, with downside risks stemming from global uncertainty and trade tensions. At the beginning of the third quarter, activity showed signs of contraction, especially in industry and manufacturing, while the tertiary and primary sectors also weakened. Private consumption showed resilience, supported by a rebound in imported goods and wage mass, although investment continued to decline. As for non-automotive manufacturing exports to the U.S., these boosted the external sector, favoured by the USMCA and lower tariffs. Despite this, slack conditions prevail in the economy, with a negative output gap and a labour market showing mixed signals, where the decline in formal employment and wage moderation could limit consumption in the coming months.

Headline inflation in the first half of September 2025 stood at 3.74%, reflecting a decrease compared to the second quarter, driven by lower non-core inflation, especially in energy, fruits, and vegetables. Additionally, some members mentioned that during the same period, core inflation remained stable at 4.26%, having stayed within the 4.20–4.30% range since mid-June, with persistent sectoral pressures, mainly in services and livestock products. Inflation expectations for the end of 2025 were slightly revised downward, while medium- and long-term expectations remain anchored around 3.5%. However, the short-term forecast for the core component was revised upward again. Although headline inflation is expected to converge to the target in the third quarter of 2026, core inflation may take longer to decelerate. Thus, the balance of risks remains tilted to the upside, with factors such as wage pressures, fiscal adjustments, volatility in non-core inflation, and trade tensions potentially affecting the inflation trajectory.

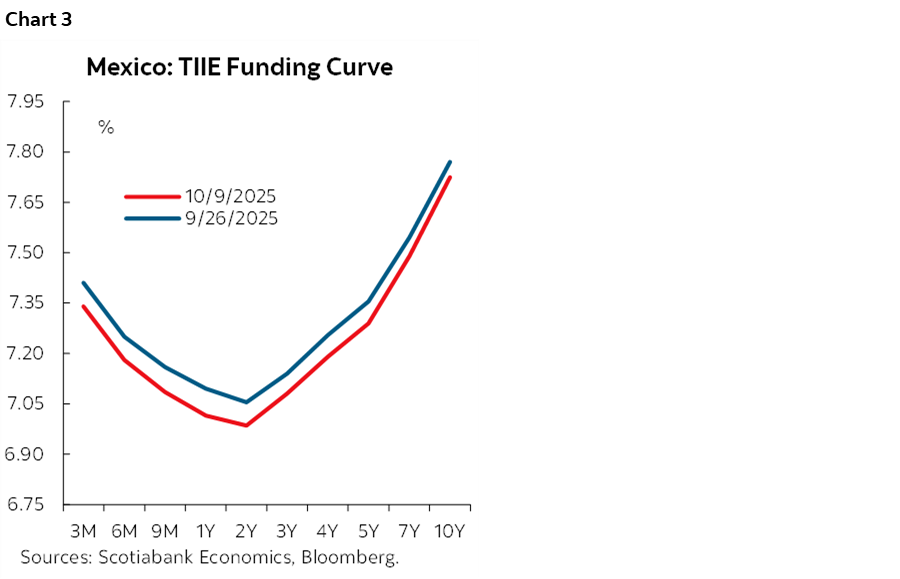

In the monetary policy discussion, most members agree that inflation has shown signs of moderation, especially in its headline component, and that the external environment—including the more accommodative stance of the Federal Reserve and the appreciation of the exchange rate—provides room to continue the monetary easing cycle. They also share the view that monetary policy should remain prudent and based on a careful assessment of inflation determinants, with an emphasis on gradualism. However, there are important contrasts. Three members believe that monetary policy can continue to ease without compromising stability, given that inflation responds more to relative price adjustments, the ex-ante real rate remains restrictive, and slack conditions are observed in the economy. On the other hand, two members express greater caution: one warns that core inflation remains outside the variability range and lacks a clear downtrend, while another emphasizes that inflation convergence has not yet been consolidated and that monetary policy should remain restrictive until a firm downward trajectory is observed. The latter also questions the effectiveness of monetary transmission amid credit expansion and high liquidity (chart 3).

Looking ahead, based on members’ comments, we anticipate an additional 25 basis point cut at the November 6th meeting, bringing the rate to 7.25%, with a split vote. However, we believe that further adjustments will depend on whether core inflation shows stronger signs of a downtrend and on the Federal Reserve’s stance in its remaining meetings this year. In this regard, the monthly inflation reading for September rebounded, less than expected, to 3.76% versus the 3.78% consensus and 3.57% previously; however, core inflation rose again to 4.28%, its highest level since April 2024, from 4.23% previously. Despite this, we maintain for now the expectation of a year-end rate of 7.00%, anticipating that the relative stance against the Federal Reserve will be preserved.

INDUSTRIAL PRODUCTION RETREATS

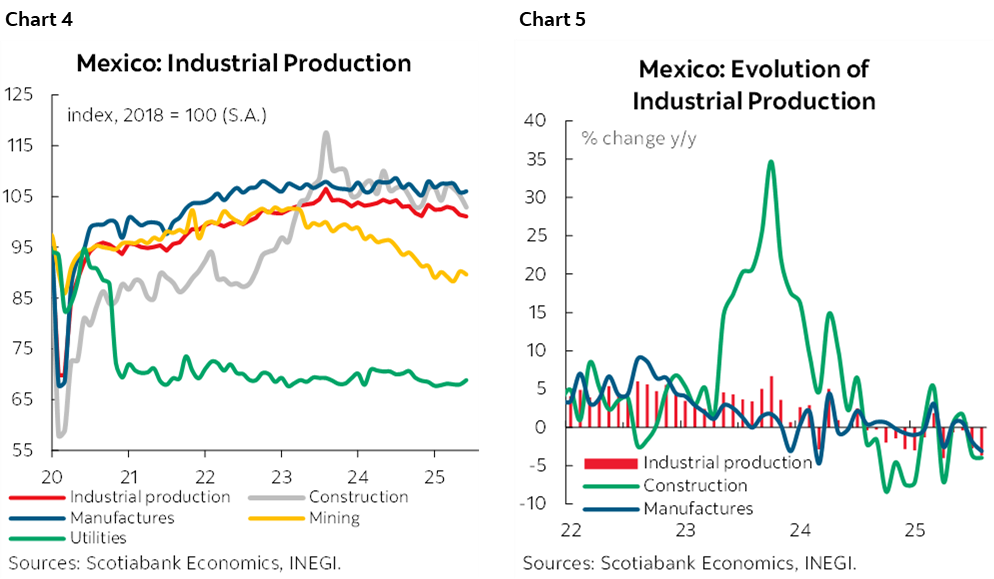

In August, industrial production fell by -0.3% m/m and -2.7% y/y. By component and compared to the previous month using seasonally adjusted figures, construction and mining recorded declines of -2.2% (compared to -1.3% in July) and -0.7% (compared to 2.2%), respectively. The non-metallic mineral industry also retreated, with a decrease of -4.7%, marking its first negative result in three months (charts 4 and 5).

Manufacturing industries recovered slightly, showing growth of 0.2%, up from -1.6%, as was the generation of electricity, water supply, and gas distribution via pipelines, which increased by 1.3%. Thus, in the first eight months of the year, industrial production showed a cumulative real variation of -1.7%.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.