- Chile: A sharp and broad-based disinflationary surprise reopens the door for a December rate cut

- Mexico: CPI meets; mixed auto sector figures

CHILE: OCTOBER CPI SURPRISE—0.0% M/M (3.4% Y/Y)

October’s CPI came in at 0.04% m/m, significantly below both market expectations and our own forecast (0.3% m/m). The surprise was widespread across divisions, with notable downside deviations in several services, particularly within the transport category. Core inflation (ex-volatile items) fell by 0.1% m/m, driven by a 0.3% m/m decline in goods prices and a marginal 0.1% m/m increase in services—the smallest October rise in recent years. Annual inflation stood at 3.4% y/y for both headline and core measures, well below the 4.0% y/y projected in the September Monetary Policy Report (IPoM).

Transport app services and streaming subscriptions led the negative contributions in October’s CPI. At the division level, the largest surprises were concentrated in transport and communications. Within transport, private passenger transport services (e.g., Uber, Cabify, Didi) fell by 6.8% m/m (contribution: -0.03 ppts), likely reversing the sharp increase seen in September. Similarly, audiovisual content subscriptions (e.g., Netflix, Spotify) posted another decline, contributing -0.024 ppts to headline inflation. Together, app-based services accounted for two of the four largest negative product-level contributions in October.

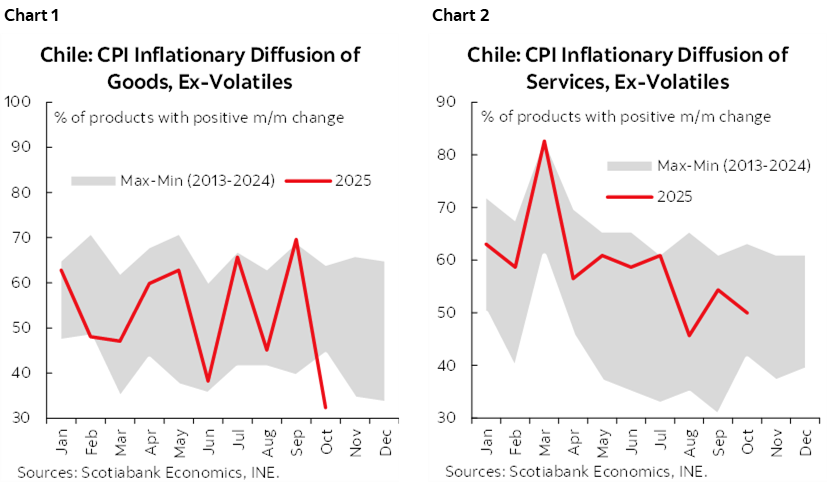

Inflation diffusion hit new historical lows, reflecting broad-based disinflation across the basket. Headline CPI diffusion dropped to 38.9%—a record low for October. The same trend was observed in the core basket, mainly due to historically low diffusion in goods (chart 1), and to a lesser extent, reduced services diffusion (chart 2) compared to the previous month. Consecutive monthly adjustments over the past three months have returned to historical lows, easing concerns raised by September’s inflation print. Part of the decline may be attributed to the early-October Cyber event, which contributed to lower prices in goods and some services. Additionally, key services posted very modest increases such as rent (0.1% m/m), its smallest October monthly rise since at least 2013.

The surprise is evident for markets and the Central Bank, likely increasing the probability of a December rate cut. However, since October’s CPI may not signal a sustained trend, we await confirmation from November’s print before revising our current 50% probability of a cut at the final monetary policy meeting of 2025. We expect nominal swap rates up to 6 months to decline following this unexpected reading.

—Aníbal Alarcón

MEXICO: CPI MEETS; MIXED AUTO SECTOR FIGURES

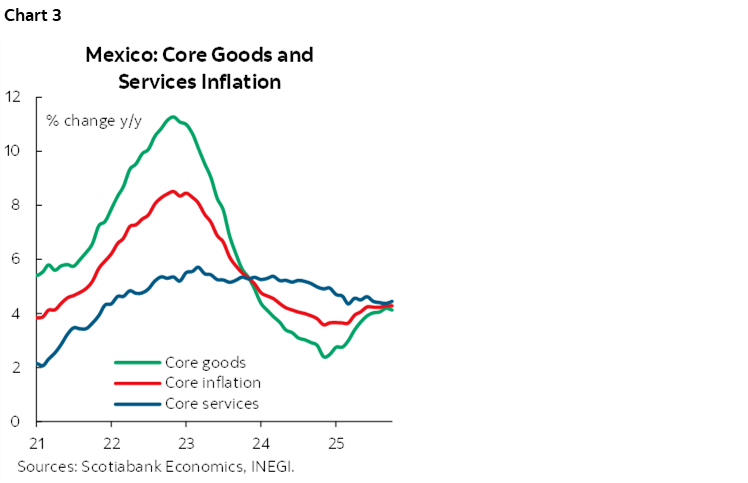

In October 2025, inflation recorded a monthly increase of 0.36%, in line with analysts’ expectations but higher than the 0.23% observed in the previous month. As a result, annual inflation stood at 3.57%, virtually matching the estimated 3.56% and below the 3.76% seen in September. Core inflation rose 0.29% month-over-month and 4.28% year-over-year (chart 3), in line with forecasts of 4.27%, with widespread increases across its components. Goods were notable, especially food, beverages, and tobacco (5.26% y/y), as well as services, where education stood out (5.82% y/y). Meanwhile, the non-core component increased 0.63% monthly and reached 1.18% annually, driven by adjustments in electricity tariffs, while agricultural products declined by -0.90%. Among the items with the greatest upward impact were electricity, air transportation, tourism services, and professional services; in contrast, green tomatoes, avocados, oranges, and lemons contributed to the downside.

Producer Price Index Trends

In the same month, producer prices eased to 2.96% y/y from 3.06% previously. By sector, prices for primary activities rose from 0.48% to 0.65%. Industrial activity prices moderated from 2.54% to 2.28%, with the largest increase in construction. Meanwhile, services accelerated from 4.22% to 4.32%.

Automotive Industry Performance: Production and Exports

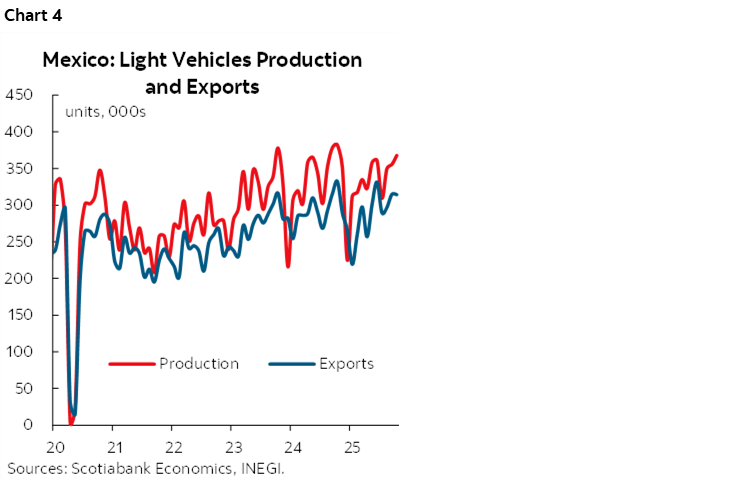

According to INEGI, 367,870 light vehicles were produced in October (chart 4), representing a -3.72% decline compared to the previous year, marking three consecutive months of contractions. Year-to-date production has fallen -0.69% versus the same period last year. In contrast, light vehicle sales rose 5.99% y/y to 129,736 units, although cumulative sales through October showed only a marginal increase of 0.11%. Finally, exports contracted -5.45% y/y in October, totaling 314,217 units. Year-to-date, 2.88 million units have been shipped abroad, a -1.5% annual decline, with the United States as the main destination, accounting for 78.7% of total exports.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.